Advertisement

- United States

- /

- Software

- /

- NasdaqGS:IDCC

InterDigital’s Fintech IoT Licensing Push Might Change The Case For Investing In InterDigital (IDCC)

Reviewed by Sasha Jovanovic

- Earlier this week, InterDigital announced an IoT patent licensing agreement that allows a leading fintech payments company to use its 3G, 4G, Wi‑Fi 5 and Wi‑Fi 6 technologies in point‑of‑sale devices, deepening the reach of its global patent portfolio into connected payment infrastructure.

- This agreement highlights how InterDigital is extending its licensing model beyond smartphones into embedded IoT and payments hardware, creating a broader base of potential long‑term recurring licensing opportunities across everyday transaction devices.

- We will now examine how this expansion into fintech point-of-sale IoT licensing could influence InterDigital's existing investment narrative and growth assumptions.

AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

InterDigital Investment Narrative Recap

To own InterDigital, you need to believe its patent portfolio can keep generating high quality, recurring licensing income across smartphones, consumer electronics, and an expanding IoT and streaming footprint. The new fintech point of sale IoT deal broadens that thesis into payments, but it does not obviously change the near term focus on sustaining recent licensing momentum or the key risk that expectations for non smartphone monetization and catch up revenues prove too optimistic.

The most relevant recent announcement here is InterDigital’s first quarter 2026 update, where management reported results ahead of guidance and reaffirmed the full year outlook. That backdrop of already strong licensing execution in smartphones, PCs, and consumer electronics frames this fintech IoT agreement as another incremental proof point in the diversification story, but investors still need to weigh it against the risk that newer verticals such as payments, streaming, and broader IoT scale more slowly than consensus currently assumes.

Yet behind this growth story, investors should also be aware of the rising regulatory and legal scrutiny on patent licensing that could...

Read the full narrative on InterDigital (it's free!)

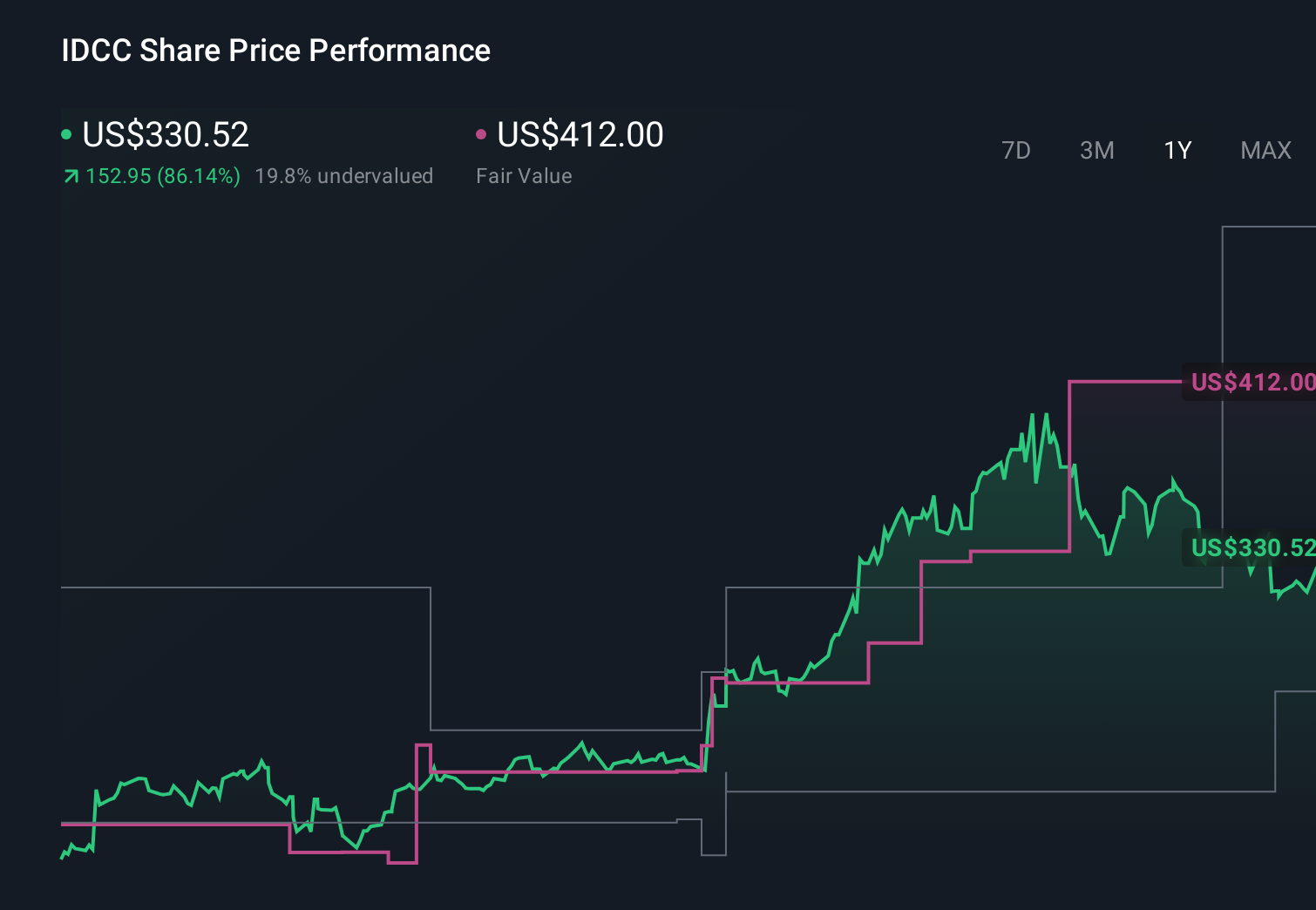

InterDigital's narrative projects $1.0 billion revenue and $490.5 million earnings by 2029.

Uncover how InterDigital's forecasts yield a $462.67 fair value, a 75% upside to its current price.

Exploring Other Perspectives

More optimistic analysts were already penciling in about US$1.0 billion of revenue and roughly US$487.6 million of earnings by 2029, so this IoT payments deal might strengthen that case or highlight how dependent it is on avoiding long term pressure from royalty free standards and similar challenges.

Explore 6 other fair value estimates on InterDigital - why the stock might be worth less than half the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your InterDigital research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free InterDigital research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate InterDigital's overall financial health at a glance.

Seeking Other Investments?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Outshine the giants: these 14 early-stage AI stocks could fund your retirement.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:IDCC

InterDigital

Operates as a global research and development company focuses on wireless, visual, artificial intelligence (AI), and related technologies.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4352.8% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22045.8% undervalued

14 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3533.5% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

TH

TheInternationalInvestor on Hotel101 Global Holdings ·

Hotel101 Global: A Scalable Hospitality Platform Built to Compound

Fair Value:US$17.2365.8% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SI

Simple_Jack on eBay ·

GME and EBay both Valued I. Their Past Instead of Futute

Fair Value:US$104.948.9% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

SI

Simple_Jack on GameStop ·

Expect GameStop's Profit Margin to Rise by 11% with a Future PE of 26x

Fair Value:US$6364.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.4% undervalued

114 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74018.6% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6117.9% undervalued

1186 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative