InterDigital (IDCC) shares have climbed over the past month, gaining 28%. Investors are taking notice as the company maintains momentum and draws attention to how its performance might shape up in the coming period.

InterDigital’s share price is on a roll lately, benefiting from building momentum and renewed optimism among investors. While the 1-year total shareholder return stands at a modest 1.5%, it is the sustained gains over the past several months that have people taking a second look. This suggests sentiment around long-term prospects is improving alongside a string of positive results and developments.

Yet with shares reaching new highs, investors may be wondering whether InterDigital is trading at an attractive valuation, or if the current price already reflects all future growth potential. Could this be a compelling entry point, or has the market priced it in?

Advertisement

Most Popular Narrative: 10% Overvalued

InterDigital's most closely followed valuation narrative signals that the latest fair value estimate of $323.75 sits meaningfully below the last close at $356.10. This creates a contrast between significant recent gains and the rigorous financial assumptions behind the fair value calculation.

The recent 67% uplift in the Samsung license and an all-time high annualized recurring revenue, driven by multi-year agreements with major OEMs, have set highly optimistic expectations for continued outsized growth in future contract renewals. This could potentially inflate valuation multiples and overstate the sustainable revenue trajectory.

Surprised the stock looks expensive even after blockbuster deals? There are bold assumptions about multi-year earnings, revenue declines, and where future profit margins land. Want to see which of these big moving parts really tilt that fair value balance? The full narrative reveals what's propelling and challenging the current valuation.

However, unexpected success in non-smartphone licensing and sustained high-margin agreements could quickly shift perceptions regarding InterDigital’s long-term growth potential.

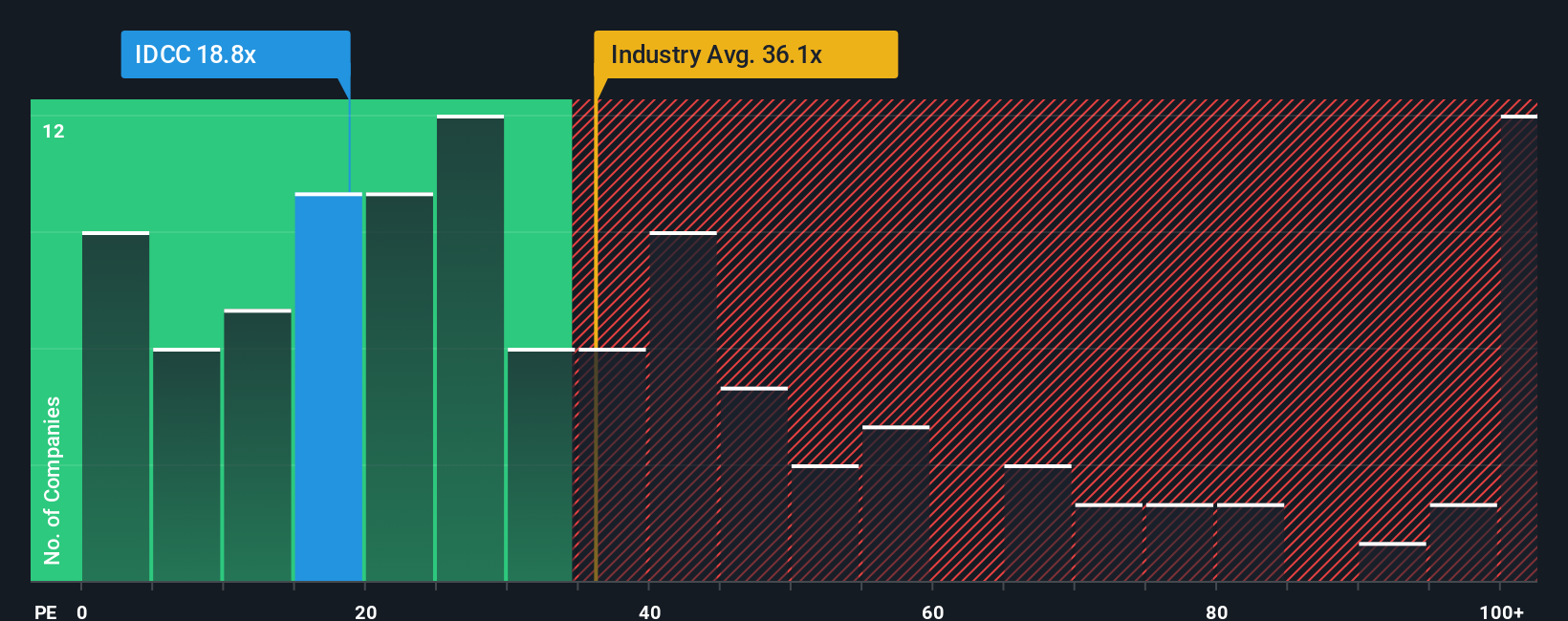

Another View: Multiples Suggest Value Compared to Peers

Looking beyond fair value estimates, InterDigital’s price-to-earnings ratio is currently 19.8x. That is considerably lower than both the US Software sector average of 35.5x and its closest peer average of 31.9x, yet it is notably above the fair ratio of 14.9x. This gap highlights room for risk if the market pivots, or potential reward if optimism holds. Do these lower multiples mean the market is underappreciating InterDigital, or is its premium justified?

Why settle for watching from the sidelines when there are standout opportunities waiting for you? Sharpen your edge with fresh picks across different sectors:

Tap into cutting-edge innovation in medicine and technology with these 31 healthcare AI stocks, and see which businesses are revolutionizing the healthcare landscape.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies