Advertisement

- United States

- /

- Software

- /

- NasdaqGS:IDCC

How Stronger Licensing Wins And Patent Enforcement At InterDigital (IDCC) Has Changed Its Investment Story

Reviewed by Sasha Jovanovic

- InterDigital recently reported Q1 2026 results that exceeded its guidance, supported by new and renewed licensing agreements and multiple successful patent injunctions against major media and technology companies.

- By combining stronger-than-expected licensing revenues with active enforcement of its intellectual property and continued involvement in 6G standards, the company is underscoring how its patent portfolio and research activity can reinforce its business model.

- We’ll now examine how these stronger-than-expected licensing results and patent enforcement wins influence InterDigital’s existing investment narrative.

We've uncovered the 11 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

InterDigital Investment Narrative Recap

To own InterDigital, you need to believe its core licensing engine can stay resilient while it broadens into consumer electronics, IoT, and 6G-driven opportunities. In the near term, the main catalyst is how consistently it can renew and expand license deals at attractive economics, while the biggest risk remains any pressure on its ability to enforce and monetize its patents. Recent Q1 outperformance and injunction wins support the existing thesis rather than materially changing it.

The company’s participation at the EuCNC & 6G Summit in Malaga, where it is showcasing Collaborative Sensing for 6G Verticals and joining panels on 6G standardization, directly ties into the longer term catalyst that many investors focus on: turning its 6G and AI networking research into future licensing pools. This complements the stronger Q1 licensing results by reinforcing that today’s cash flows are underpinned by ongoing technical relevance in next generation wireless.

Yet in contrast, investors should also factor in the risk that growing regulatory and legal scrutiny of how patents are enforced could eventually...

Read the full narrative on InterDigital (it's free!)

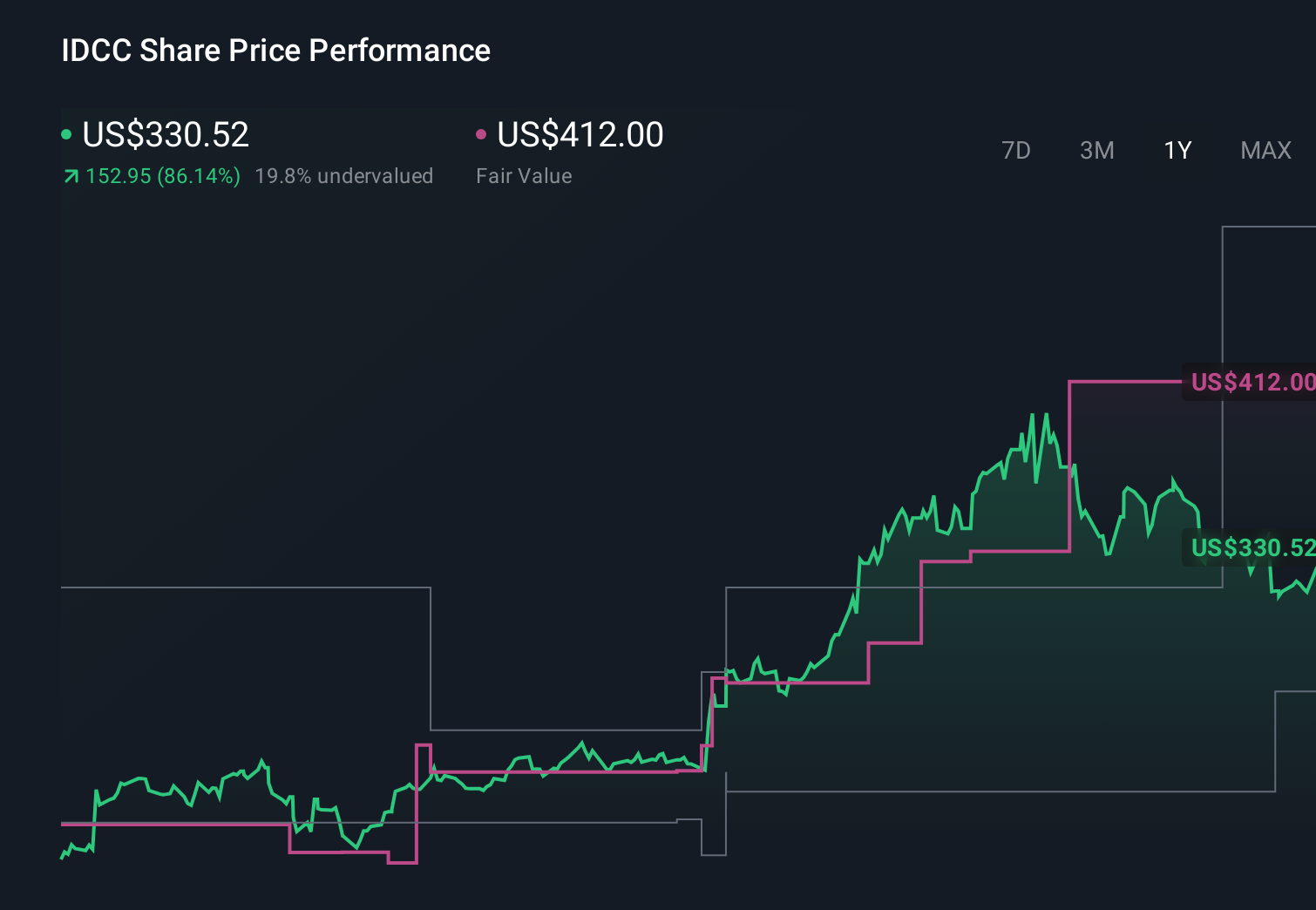

InterDigital's narrative projects $824.6 million revenue and $350.8 million earnings by 2029.

Uncover how InterDigital's forecasts yield a $462.67 fair value, a 79% upside to its current price.

Exploring Other Perspectives

Before this news, the most optimistic analysts were assuming revenues near US$1.0 billion and earnings around US$487.6 million, which is far more upbeat than consensus, and shows how differently you might weigh 6G upside versus the risk that shifting to royalty free or open standards could weaken InterDigital’s licensing power over time.

Explore 5 other fair value estimates on InterDigital - why the stock might be worth as much as 79% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your InterDigital research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free InterDigital research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate InterDigital's overall financial health at a glance.

Ready For A Different Approach?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Rare earth metals are the new gold rush. Find out which 32 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:IDCC

InterDigital

Operates as a global research and development company focuses on wireless, visual, artificial intelligence (AI), and related technologies.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7061.6% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17036.6% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38026.3% undervalued

20 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7448.8% undervalued

50 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

Recently Updated Narratives

AY

Ayomiposi_X on CWG ·

63% Profit Growth, 6.8× Forward P/E: Inside CWG Plc's FY 2025 Numbers and What They Signal

Fair Value:₦3132.9% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WE

Westimnster on EPAM Systems ·

Expect EPAM's fair value to reach 59.38

Fair Value:US$113.3814.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28023.3% undervalued

89 followersusers have followed this narrative

9 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.7% undervalued

124 followersusers have followed this narrative

2 commentsusers have commented on this narrative

36 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9722.1% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1930.3% undervalued

46 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative