Advertisement

- United States

- /

- Software

- /

- NasdaqGS:IDCC

Assessing InterDigital (IDCC) Valuation As New IoT Payments Licensing Deal Expands Beyond Smartphones

InterDigital’s new IoT licensing deal and why it matters for the stock

InterDigital (IDCC) has signed an IoT patent license agreement with a well known fintech company in the payments space, covering point of sale devices that use its 3G, 4G, Wi Fi 5 and Wi Fi 6 technologies.

For you as an investor, this agreement highlights how InterDigital is putting its wireless intellectual property to work in connected payment infrastructure. This is a segment that sits outside the company’s more traditional smartphone and telecom hardware licensing activity.

See our latest analysis for InterDigital.

Despite the new IoT agreement, InterDigital’s share price is down 27.9% over the past 30 days and 23.6% over 90 days. However, the 1 year total shareholder return of 25.2% and very large 5 year total shareholder return suggest longer term holders have still seen strong gains.

If this IoT licensing story has you thinking about other ways to tap into connected technology and infrastructure, it could be worth scanning 34 power grid technology and infrastructure stocks.

With InterDigital’s stock falling sharply in recent months even as it signs new IoT deals, you need to ask whether sentiment has swung too far or if the current price already reflects the company’s future growth potential.

Most Popular Narrative: 42.5% Undervalued

The most followed valuation narrative puts InterDigital’s fair value at $462.67 per share versus a last close of $266.12, framing a wide gap that hinges on long term licensing assumptions.

The recent 67% uplift in the Samsung license and an all time high annualized recurring revenue, driven by multi year agreements with major OEMs, have set highly optimistic expectations for continued outsized growth in future contract renewals, potentially inflating valuation multiples and overstating sustainable revenue trajectory.

Analysts behind this narrative are leaning on detailed forecasts for earnings, revenue and margins, plus a premium future P/E multiple supported by a specific discount rate and buyback assumptions. The full story shows exactly how those ingredients combine to reach the projected fair value and what would need to happen in the business for that gap to close over time.

Result: Fair Value of $462.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the narrative could be stretched if regulatory pressure on patent licensing deepens, or if expected revenue from non smartphone verticals, such as IoT and automotive, proves slower to materialize.

Find out about the key risks to this InterDigital narrative.

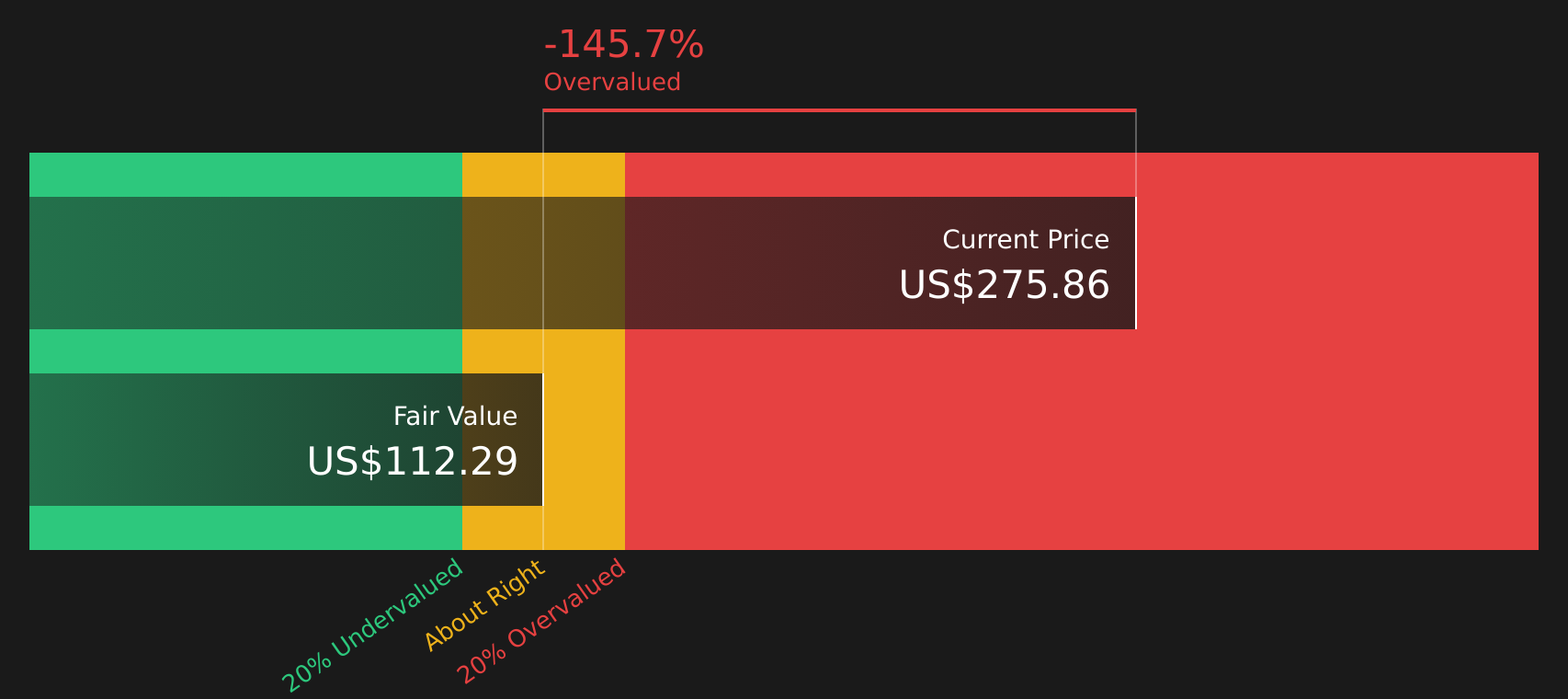

Another View: What the DCF Model Says

While the popular narrative points to a $462.67 fair value, our DCF model paints a very different picture. On that approach, InterDigital’s estimated future cash flow value comes in at $113.19 per share, which would frame the stock as expensive at the current $266.12. For you, the real question is which set of assumptions feels more realistic over the long run.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out InterDigital for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals across the narratives, do you think the market is too cautious or not cautious enough? Act while the information is fresh and review the 3 key rewards.

Looking for more investment ideas?

If you stop here, you could miss stocks that fit your style far better, so take a few minutes and let the data point you to fresh opportunities.

- Target potential mispricings by scanning 51 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect their underlying strength.

- Lock in income focused ideas by reviewing 10 dividend fortresses that offer higher yields alongside an emphasis on resilience.

- Prioritise capital preservation by checking 67 resilient stocks with low risk scores built around companies with more resilient risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:IDCC

InterDigital

Operates as a global research and development company focuses on wireless, visual, artificial intelligence (AI), and related technologies.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4353.2% undervalued

73 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22043.1% undervalued

23 followersusers have followed this narrative

6 commentsusers have commented on this narrative

26 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.8% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8168.5% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

RE

RetiredbutWorking on USA Rare Earth ·

USAR Secures $19.3M Boost to Develop an Independent Rare Earth Supply Chain

Fair Value:US$0.336.7k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1932.1% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NE

newsfinder11221 on Tanco Holdings Berhad ·

Tanco Holdings Expands Growth Pipeline With Smart Port, ECRL And Property Projects

Fair Value:RM 8.1279.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.0% undervalued

114 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74018.2% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6116.8% undervalued

1191 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative