Advertisement

- United States

- /

- Software

- /

- NasdaqGS:IDCC

Assessing InterDigital (IDCC) Valuation After A Q1 Beat And Key Licensing And Patent Injunction Wins

InterDigital (IDCC) is back in focus after first quarter results came in ahead of guidance, helped by new and renewed licensing agreements with major electronics manufacturers and several patent injunction wins.

See our latest analysis for InterDigital.

The latest Q1 beat and InterDigital’s visibility at 6G conferences come after a sharp reset in the stock, with the share price down 9.1% over the past month and 26.9% over 90 days, even though the 1 year total shareholder return is 16.3% and the 5 year total shareholder return is 252.2%. This points to long term momentum that contrasts with recent weakness.

If events around InterDigital have you thinking about where else growth in wireless, AI and next gen infrastructure could show up, consider widening your search with our screener of 48 AI infrastructure stocks

With InterDigital shares down sharply in recent months despite a 1 year total return of 16.3% and a 5 year total return above 250%, the key question is whether current pricing offers upside or whether the market already reflects future growth.

Most Popular Narrative: 43.6% Undervalued

InterDigital's most followed narrative pegs fair value at $462.67 per share, well above the recent close around $261.07, setting up a clear valuation gap for investors to weigh.

The recent 67% uplift in the Samsung license and an all-time high annualized recurring revenue, driven by multi-year agreements with major OEMs, have set highly optimistic expectations for continued outsized growth in future contract renewals, potentially inflating valuation multiples and overstating sustainable revenue trajectory. Investors may be projecting accelerated licensing expansion into non-smartphone verticals (such as automotive, industrial IoT, smart cities, and healthcare) due to the widely anticipated proliferation of connected devices; however, actual monetization and revenue ramp from these adjacent markets remain unproven and could fall short of aggressive assumptions.

Want to see how a flat revenue outlook, slightly lower margins, and a much higher future earnings multiple can still support that kind of fair value gap? The narrative leans on detailed profit assumptions, a long runway for contracts, and a punchy valuation multiple that goes well beyond current market pricing.

Result: Fair Value of $462.67 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upbeat narrative could unravel if regulators tighten rules around patent licensing, or if newer IoT and 6G markets deliver slower than expected monetization.

Find out about the key risks to this InterDigital narrative.

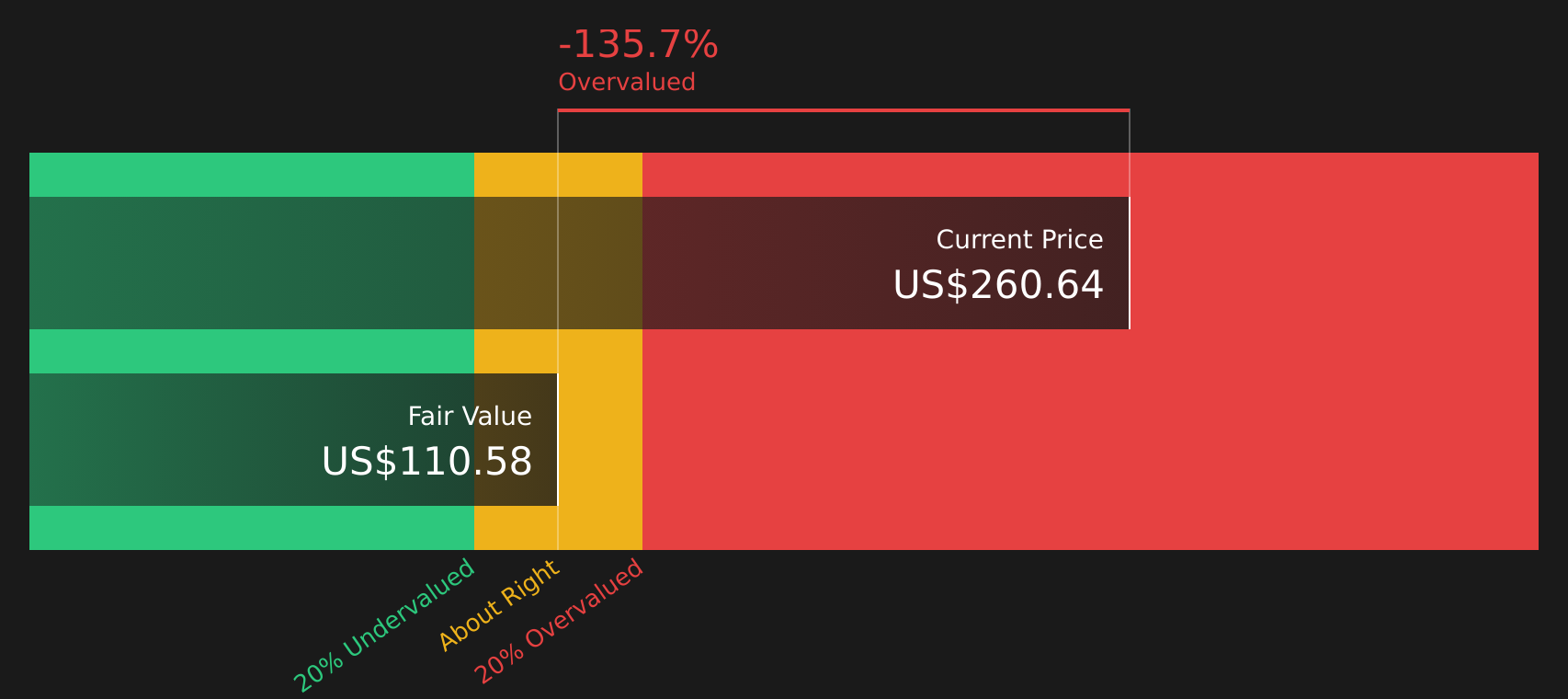

Another Angle On Valuation

That analyst-driven fair value of $462.67 contrasts sharply with Simply Wall St’s own discounted cash flow work. The SWS DCF model puts InterDigital’s future cash flow value at $112.38 per share versus a recent price around $256.64, pointing to an overvalued outcome instead.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out InterDigital for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mix of optimism and doubt here feels familiar, treat it as your cue to move quickly and review the underlying data for yourself, especially the 3 key rewards.

Looking for more investment ideas?

If InterDigital sits on your watchlist already, do not stop there, keep building your opportunity set so you are not relying on a single stock story.

- Chase potential mispricings by scanning 46 high quality undervalued stocks that pair solid fundamentals with prices that differ from underlying business quality.

- Strengthen your income stream by reviewing 10 dividend fortresses that focus on higher yields backed by resilient business models.

- Protect your downside by filtering for 64 resilient stocks with low risk scores designed to highlight companies with more stable risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:IDCC

InterDigital

Operates as a global research and development company focuses on wireless, visual, artificial intelligence (AI), and related technologies.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7057.7% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17036.9% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38027.7% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7446.7% undervalued

55 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

Recently Updated Narratives

IM

Imthetxarbi on Sylvania Platinum ·

A Debt-Free PGM Producer Trading at 2x EBITDA With a 10% Dividend Yield Nobody Is Talking About

Fair Value:UK£1.7948.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MI

Miracleworker on Diversified Energy ·

DEC.L: Dip-Buying Opp, 8%+ Div & 57-100% Potential Gain Over 12 Months

Fair Value:UK£10.460% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IM

Imthetxarbi on Watches of Switzerland Group ·

A Compelling Compounder at a Retailer's Multiple

Fair Value:UK£1134.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.3% undervalued

124 followersusers have followed this narrative

3 commentsusers have commented on this narrative

36 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9721.8% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1932.0% undervalued

46 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

FR

FrontierTom on United States Antimony ·

Great Long term play that needs great tolerance for price swings along the way.

0

|0