Advertisement

- United States

- /

- Software

- /

- NasdaqGS:GTLB

GitLab (GTLB) Q3 2026 Revenue Growth Outpaces Ongoing EPS Loss, Testing Profitability Narrative

GitLab (GTLB) just posted its Q3 2026 numbers, landing revenue at about $244 million with basic EPS of roughly -$0.05 as the company continues to prioritize growth over bottom line profits. The company has seen revenue step up from around $183 million in Q2 2025 to $196 million in Q3 2025, then $211 million in Q4 2025 and $214 million, $236 million and now $244 million across the first three quarters of 2026. At the same time, EPS swung from a positive $0.18 in Q3 2025 to modest losses through 2026, setting the stage for an earnings season where investors will be closely focused on how quickly margins can catch up to the expanding top line.

See our full analysis for GitLab.With the headline numbers on the table, the next step is to weigh them against the big narratives around GitLab, from growth durability to the path toward profitability, and see which stories still hold up under the latest data.

See what the community is saying about GitLab

Losses Narrow as Revenue Scales

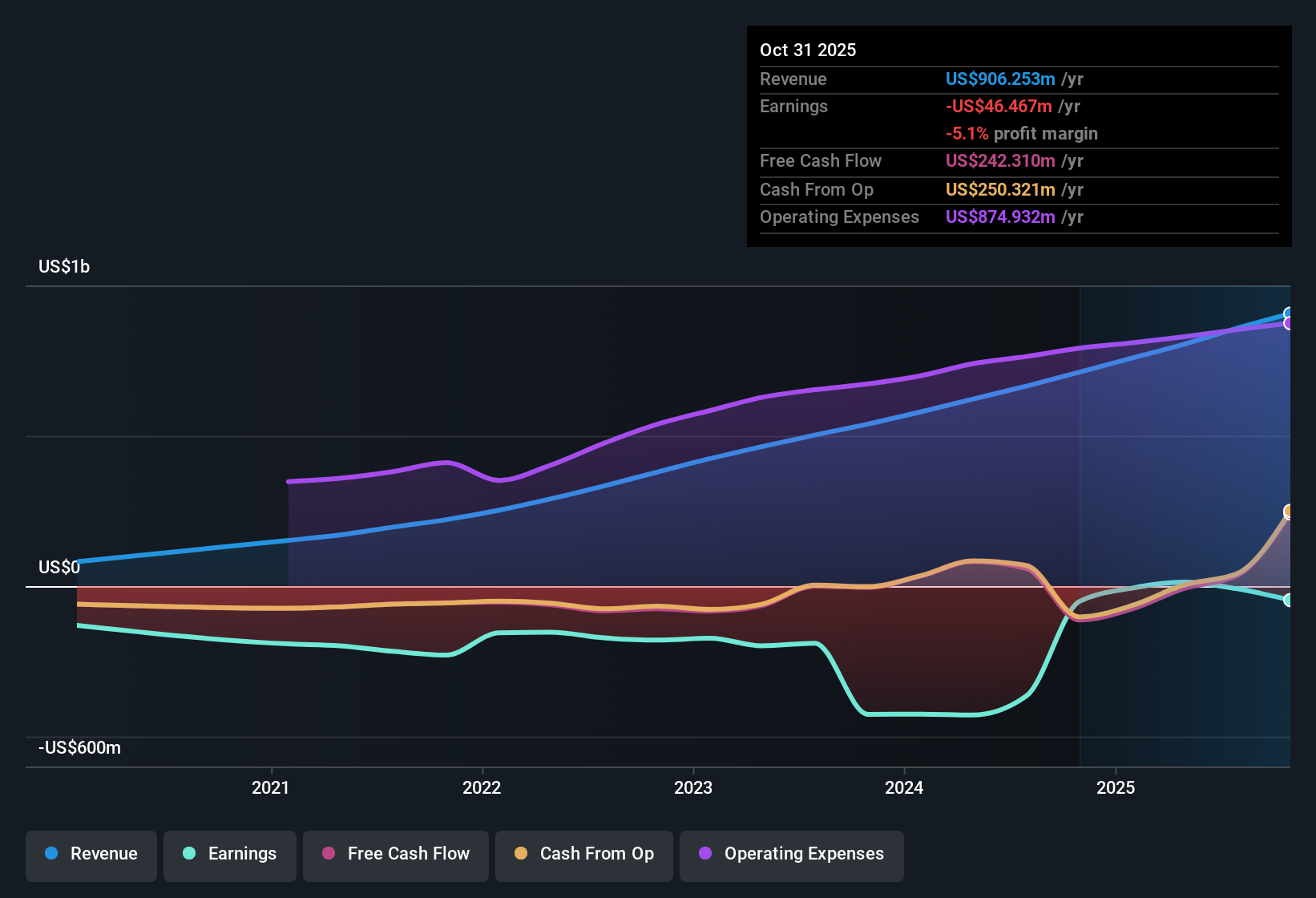

- On a trailing 12 month basis, GitLab generated about $906 million of revenue while posting a net loss of roughly $46 million, showing that losses are small relative to the size of the business.

- Analysts' consensus view that AI driven platform upgrades can support long term growth and better profitability meets mixed evidence in these numbers.

- The platform oriented story is backed by revenue rising from about $666 million to $906 million over the last six trailing 12 month snapshots, aligning with expectations of steady expansion.

- At the same time, the shift from a $13 million trailing profit to a $46 million trailing loss over the last three snapshots reminds investors that the path to monetizing those AI and security features is not yet flowing consistently into the bottom line.

Solid Growth, No Near Term Profits

- Forecast revenue growth of roughly 15.5% per year sits alongside expectations that GitLab will remain unprofitable for at least the next three years, even after shrinking losses by about 12.3% per year over the past five years.

- Bears focus on this disconnect between growth and profits and see several ways it could weigh on future earnings power.

- Concerns about slower net new customer additions and heavier reliance on existing customers tie directly into the need for that 15.5% growth rate to keep holding up if margins are not yet in the black.

- Execution risks from shifting to a hybrid seat plus usage model and recent go to market changes sit uncomfortably next to the fact that trailing 12 month results have swung from a $6 million loss to a $46 million loss over the last five data points.

Valuation Straddles Growth And Risk

- At a current share price of $37.83, GitLab trades on about 7 times trailing 12 month sales, cheaper than the 8.3 times peer average but richer than the 4.9 times broader US software group, while sitting below a DCF fair value of roughly $64.10.

- How investors interpret this in light of the consensus narrative comes down to whether growth and platform depth justify that middle ground multiple.

- Supporters highlight that GitLab has lifted trailing revenue from about $666 million to $906 million while integrating security and compliance into its DevSecOps stack, which aligns with the idea of a premium, unified platform.

- More cautious investors point to the trailing $46 million loss and the expectation of no profits over the next three years as reasons the stock might stay closer to the broader software valuation band than the DCF fair value implies.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for GitLab on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

See the numbers from another angle and want to test that view fast? Shape your own GitLab story in just a few minutes, Do it your way.

A great starting point for your GitLab research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Explore Alternatives

GitLab’s solid revenue growth is overshadowed by persistent losses, execution risk around new pricing models, and uncertainty over when profits will reliably materialize.

If you want growth backed by cleaner financial momentum, use our stable growth stocks screener (2071 results) to quickly zero in on companies already pairing consistent expansion with clearer earnings progress.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:GTLB

GitLab

Develops software for the software development lifecycle in the United States, Europe, and the Asia Pacific.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This OVERLOOKED Gold Stock Could TRIPLE - 3.3M Ounces, Bottom-of-Peer Valuation

Fair Value:CA$470.0% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9721.3% undervalued

50 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1927.2% undervalued

41 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

BJ

Bjergby on PagSeguro Digital ·

PagSeguro: A Cheap Bet on a Bank Hiding Inside a Payments Company, Priced for Failure

Fair Value:US$19.251.4% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

HU

Hunter_Z on A1 A.K. Koh Group Berhad ·

A1AKK’s Festive Season Sales Growth Highlights Strong Core Business Despite IPO-Related Earnings Impact

Fair Value:RM 0.1154.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on ASM Automation Group Berhad ·

ASM Automation Building for the Next Growth Phase Despite Temporary Earnings Slowdown

Fair Value:RM 0.08962.9% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on Geohan Corporation Berhad ·

Geohan Builds Momentum with RM460 Million Order Book

Fair Value:RM 0.042614.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.3% undervalued

119 followersusers have followed this narrative

2 commentsusers have commented on this narrative

34 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9721.3% undervalued

50 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1927.2% undervalued

41 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative