Advertisement

- United States

- /

- IT

- /

- NasdaqGS:FSLY

Assessing Fastly (FSLY) After Prolonged Share Price Declines

Reviewed by Bailey Pemberton

- If you are wondering whether Fastly's current share price lines up with its underlying value, you are not alone.

- The stock closed at US$9.62 recently, with returns of 2.6% over the last 7 days, a 5.1% decline over 30 days, a 5.6% decline year to date, and a 10.3% decline over the past year. The 3 year and 5 year returns stand at 19.2% and 91.4% declines respectively.

- These mixed returns have kept Fastly on many investors' watchlists. The share price history raises questions about how the market currently views its growth prospects and risks. That context makes it especially important to step back and assess what you are actually paying for today.

- On our checks, Fastly scores a 2 out of 6 valuation score, which suggests some areas may look cheaper than others. Next, we will walk through the main valuation approaches and then finish with a more complete way to think about what the stock might be worth.

Fastly scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Fastly Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company might be worth by projecting its future cash flows and discounting them back to today. It is essentially asking what all those future dollars are worth in present terms.

For Fastly, the model uses a 2 stage Free Cash Flow to Equity approach. The latest twelve month free cash flow is about $31.29 million, and analyst inputs plus extrapolations point to free cash flow of $36.58 million in 2026 and $43.60 million in 2027. Simply Wall St then extends those projections out to 10 years, gradually tapering expected growth in cash flows through 2035.

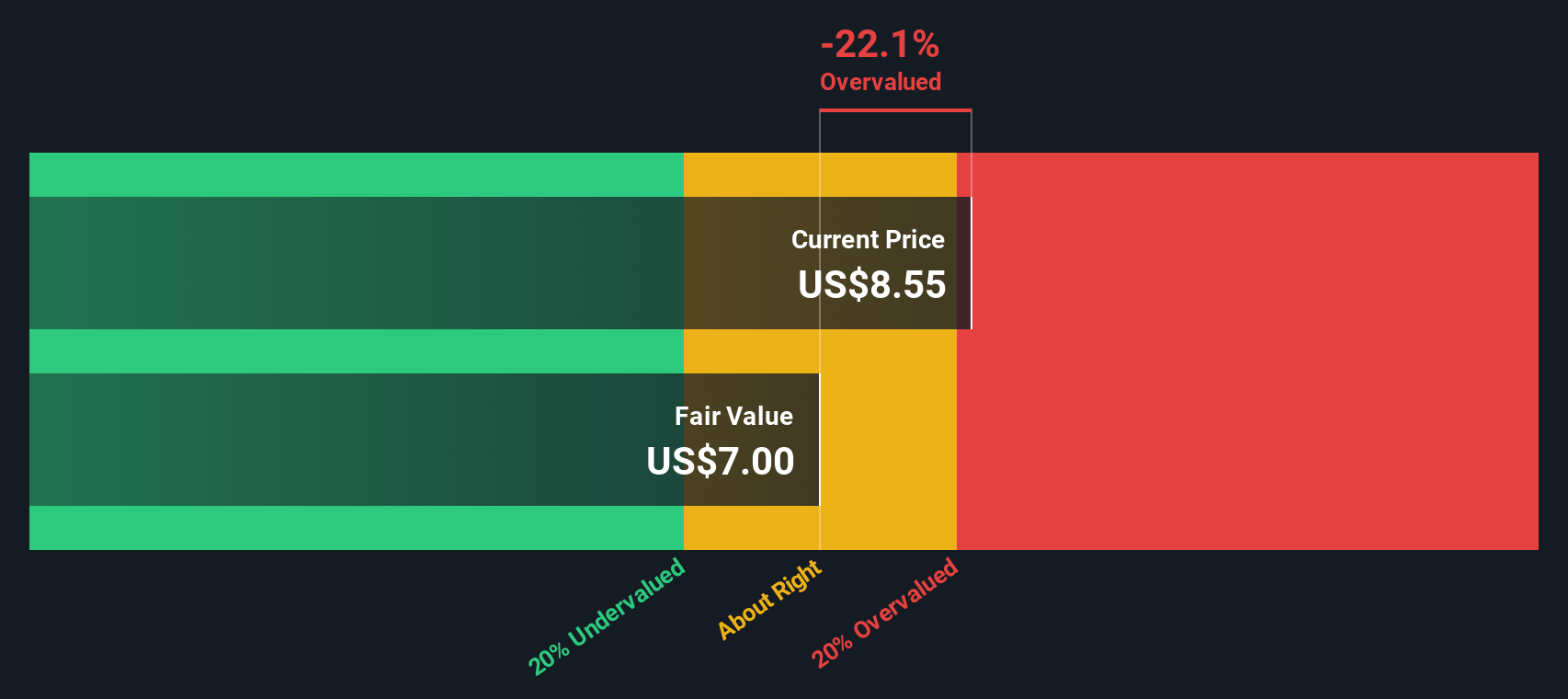

When all of these projected cash flows are discounted back to today, the model arrives at an estimated intrinsic value of about $5.24 per share. Compared with the recent share price of $9.62, the DCF output suggests the stock is 83.8% overvalued on this cash flow view.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Fastly may be overvalued by 83.8%. Discover 869 undervalued stocks or create your own screener to find better value opportunities.

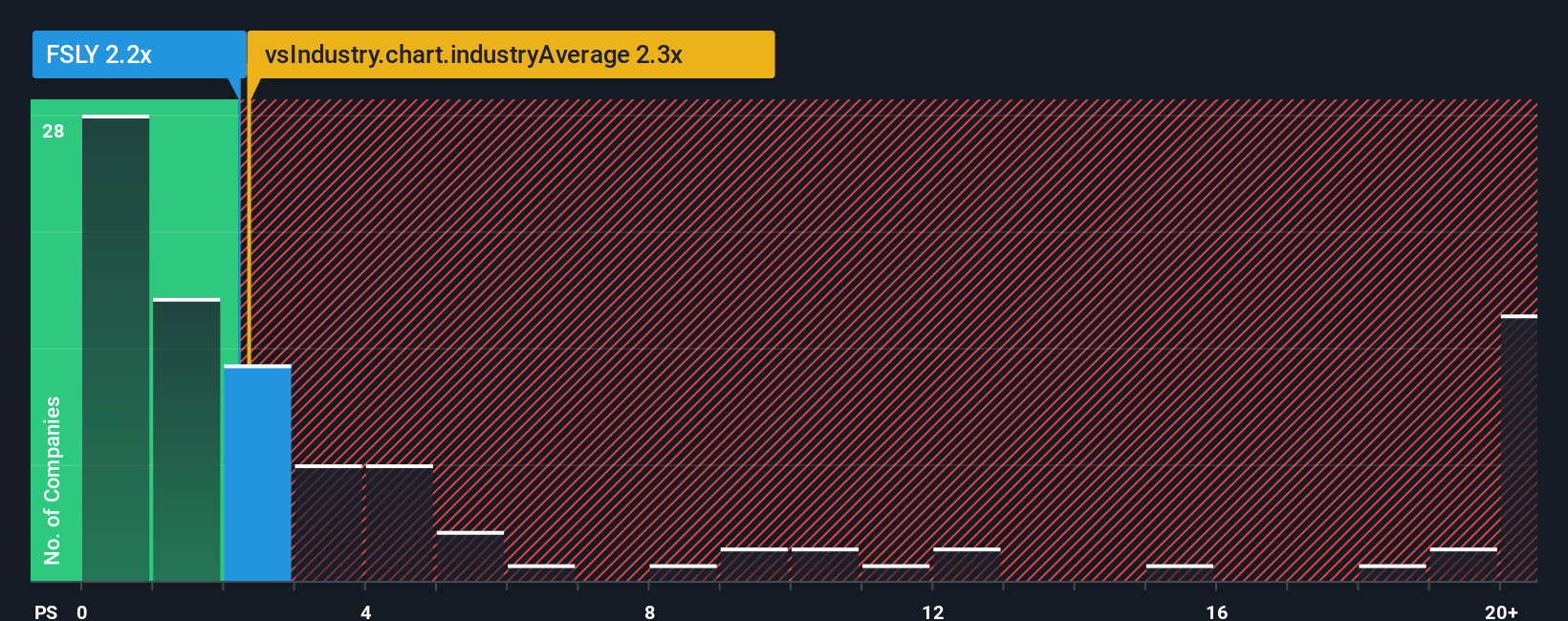

Approach 2: Fastly Price vs Sales

For companies where earnings are limited or volatile, P/S is often more useful than P/E because it focuses on revenue rather than profit, which can swing around with investment cycles and accounting treatments. Investors usually pay a higher or lower P/S depending on how they see a company’s growth potential and risk, so there is no single “right” multiple.

Fastly currently trades on a P/S of 2.43x. That sits close to the broader IT industry average P/S of 2.23x and below the peer group average of 5.00x. Simply Wall St’s Fair Ratio framework goes a step further by estimating what P/S might be reasonable for Fastly, given factors like its growth profile, margins, size and risk, and arrives at a Fair Ratio of 2.60x.

This Fair Ratio is designed to be more tailored than a simple comparison with peers or the industry, because it adjusts for Fastly’s own characteristics rather than assuming it should trade exactly like the average company. With the actual P/S of 2.43x sitting slightly below the Fair Ratio of 2.60x, the multiple based view describes the shares as modestly undervalued on this metric.

Result: UNDERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1417 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Fastly Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce Narratives. These are simply your story about Fastly connected to your own numbers on future revenue, earnings, margins and what you think a fair value might be.

A Narrative links three pieces together: the business story you believe, the financial forecast that story implies and the fair value that follows from those assumptions, so you can clearly see how your view translates into a number.

On Simply Wall St, Narratives sit inside the Community page and are used by millions of investors as an easy tool, because the platform compares each Narrative fair value to the current share price and keeps those views updated automatically when new information like news or earnings is added.

For Fastly, this can mean one investor builds a Narrative that points to a much higher fair value based on stronger revenue and margin assumptions, while another uses more cautious forecasts and arrives at a far lower fair value. This gives you a clear sense of how different perspectives lead to different price expectations.

Do you think there's more to the story for Fastly? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:FSLY

Fastly

Operates an edge cloud platform for processing, serving, and securing its customer’s applications in the United States, the Asia Pacific, Europe, and internationally.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

61 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

AN

AntonioS on CAR Group ·

CAR Group. A wonderful compounding franchise at a fair-not-cheap price.

Fair Value:AU$3219.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GA

GaryB on Palantir Technologies ·

Palantir hits 52 week low.

Fair Value:US$274.861.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NO

North49_ on iShares - iShares MSCI South Korea ETF ·

EWY:US NYSE Arca iShares Msci South Korea ETF, an opportunity to diversify your tech investments.

Fair Value:US$273.4525.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative