Advertisement

- United States

- /

- Software

- /

- NasdaqGS:DBX

Is Dropbox (DBX) Still Attractive After Recent Share Price Recovery?

Reviewed by Bailey Pemberton

- If you are wondering whether Dropbox shares still offer value at around US$26.74, you are not alone. This article is here to unpack what that price could mean for long term investors.

- The stock has returned 2.2% over the last 7 days and 7.0% over the last 30 days, while year to date returns sit at a 0.7% decline and the 1 year return is 5.8%, with a 3 year gain of 36.7% and a 5 year return of a 3.6% decline.

- Recent market attention on Dropbox has focused on how the business is positioned within the broader software sector and what that implies for its long term cash generation and competitive standing. This backdrop helps explain why the share price has been moving, as investors reassess how much they are willing to pay for those future cash flows.

- Our assessment currently gives Dropbox a valuation score of 5 out of 6, based on how many of our checks suggest the shares may be undervalued. Next we will walk through the main valuation approaches behind that score before finishing with a broader way to think about what "fair value" really means for this stock.

Approach 1: Dropbox Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a company could be worth by projecting its future cash flows and then discounting them back to today using a required rate of return. In short, it asks what all those future dollars are worth in present day terms.

For Dropbox, the model used is a 2 Stage Free Cash Flow to Equity approach, based on cash flow projections in US$. The latest twelve month free cash flow is about $928.9 million, and analysts provide explicit estimates out to 2027, where free cash flow is projected at $985.2 million. Beyond that, Simply Wall St extrapolates ten year free cash flow projections, which run from $931.0 million in 2026 through to $1,296.6 million in 2035, with each of those future values discounted back to today.

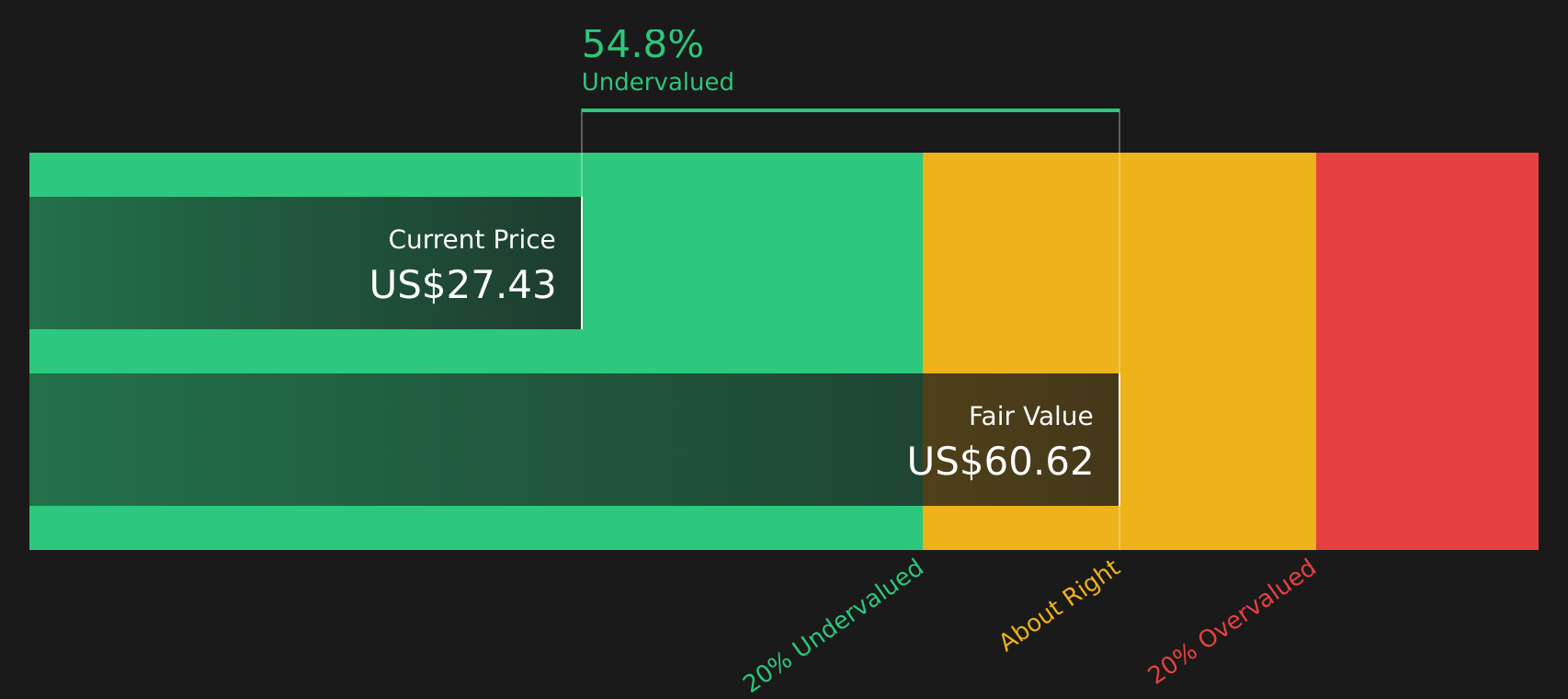

When all projected and discounted cash flows are added up, the model arrives at an estimated intrinsic value of about $59.44 per share. Compared with the current share price of around $26.74, this framework suggests the stock may be trading at a discount of about 55.0% to the model’s estimated value.

Result: Potentially undervalued based on this DCF model

Our Discounted Cash Flow (DCF) analysis suggests Dropbox is undervalued by 55.0%. Track this in your watchlist or portfolio, or discover 46 more high quality undervalued stocks.

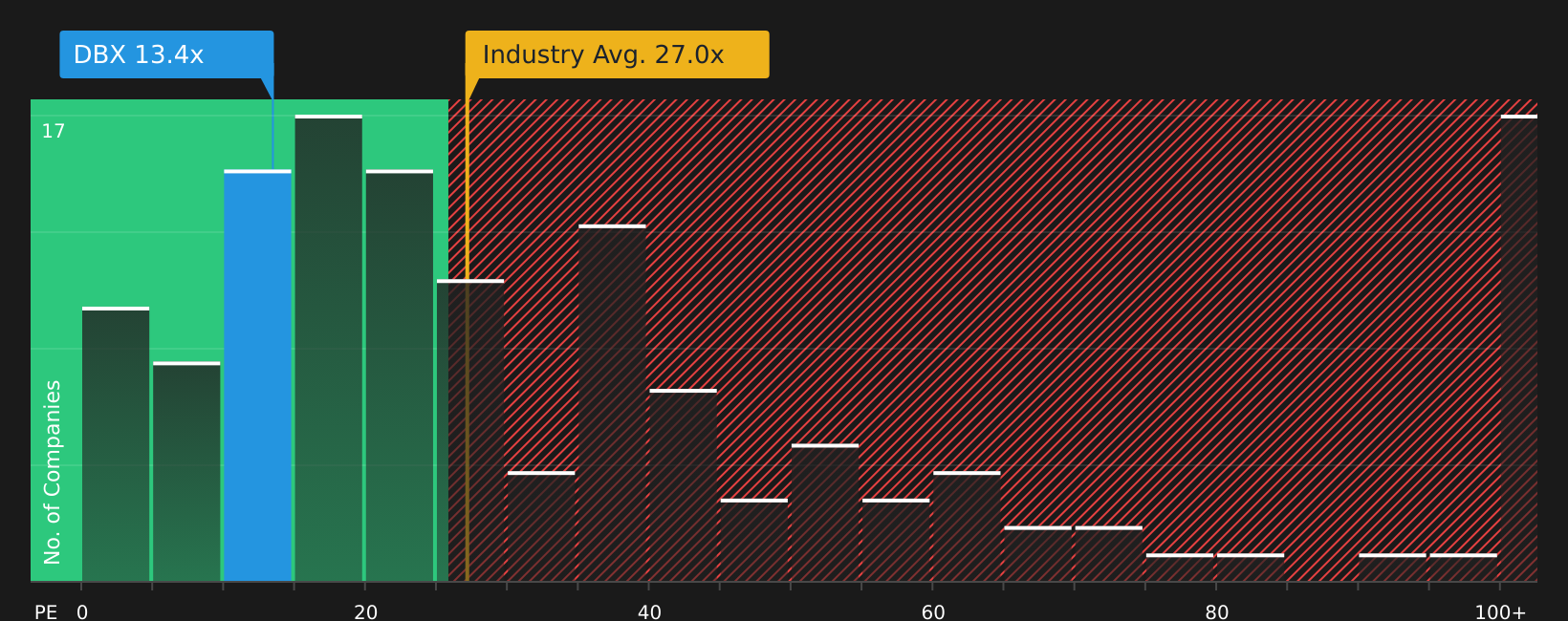

Approach 2: Dropbox Price vs Earnings

For a profitable company like Dropbox, the P/E ratio is a straightforward way to relate what you pay for each share to the earnings that company is generating today. Investors usually accept a higher P/E when they expect stronger growth or see the earnings as relatively predictable, and a lower P/E when growth is more modest or the risks feel higher.

Dropbox currently trades on a P/E of 12.69x. That sits below the broader Software industry average P/E of about 27.27x and also below the peer group average of around 29.34x. Simply Wall St also calculates a proprietary “Fair Ratio” for Dropbox of 19.51x, which is the P/E level that would broadly line up with its earnings growth profile, margins, industry, market cap and risk factors.

This Fair Ratio aims to be more tailored than a simple comparison with industry or peers, because it adjusts for Dropbox’s own characteristics rather than assuming it should trade like an average Software stock. Setting the current P/E of 12.69x against the Fair Ratio of 19.51x suggests the shares are priced below what this framework would consider a more typical valuation.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Dropbox Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce Narratives, a simple tool on Simply Wall St’s Community page that lets you set out your own story for Dropbox; translate that story into assumptions about future revenue, earnings and margins; connect those assumptions to a fair value; then compare that fair value to the current price. The highest Dropbox Narrative on the platform today points to a fair value of about US$30 per share and the lowest to about US$20 per share, showing how two investors can look at the same company data, react differently as new news or earnings automatically update their Narrative, and still use a clear, consistent framework to decide whether the current price around US$26.74 fits their view or not.

For Dropbox however, we will make it really easy for you with previews of two leading Dropbox narratives:

First up is a bullish take that leans into buybacks and AI tools like Dash. This is followed by a more cautious view that focuses on churn, competition and earnings risk. Having both side by side can help you decide which set of assumptions feels closer to your own.

Fair value in this bullish narrative: US$30.00 per share

Implied pricing gap vs last close of US$26.74: about 10.9% undervalued

Revenue trend used in this narrative: 29.8% revenue decline rate

- Assumes AI powered tools like Dropbox Dash, plus enterprise focused products, support higher margins and cash flows over time, even as headline revenue expectations are trimmed.

- Builds in rising profit margins and ongoing share buybacks, which together lift expected earnings per share and justify a higher future price in the model.

- Flags real risks around churn, competition and execution on new products, so the bullish outcome depends on management turning product investment into adoption and monetization.

Fair value in this bearish narrative: US$20.00 per share

Implied pricing gap vs last close of US$26.74: about 33.0% overvalued

Revenue trend used in this narrative: 157.2% revenue decline rate

- Builds around pressure from Teams customer churn, workforce reductions and lower outbound sales capacity, which together weigh on revenue and earnings assumptions.

- Views the shift from mature file storage into AI tools like Dash as introducing timing and execution risk, with slower expected contribution from new products.

- Highlights that if revenue growth sits near the lower end of expectations and margins soften, the earnings multiple that looks reasonable today could be hard to sustain.

If you want to see the full reasoning behind these previews and how other investors are framing Dropbox, Curious how numbers become stories that shape markets? Explore Community Narratives can be a useful next step before you decide how the current price lines up with your own view of the story.

Do you think there's more to the story for Dropbox? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DBX

Dropbox

Provides a content collaboration platform in the United States and internationally.

Undervalued with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3447.6% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.1% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.652.3% undervalued

28 followersusers have followed this narrative

2 commentsusers have commented on this narrative

13 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£161.8% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

YO

youwakeup on Harvest Strategy Enhanced High Income Shares ETF ·

MSTE: Turning Bitcoin Volatility Into Monthly Cash Flow

Fair Value:CA$11.7579.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Ester on Agricore CS Holdings Berhad ·

Agricore CS Holdings Is Riding on Regional Growth Through Defensible Food Ingredient Supply Chains

Fair Value:RM 0.6841.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JU

julio on Masco ·

MASCO VALUATION

Fair Value:US$91.5618.8% undervalued

34 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.0% undervalued

57 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.5% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative