Dropbox (DBX) shares pulled back slightly today, closing at $29.84 after a recent stretch of gains. Investors may be reassessing Dropbox’s valuation, especially given its steady performance over the past month.

Dropbox’s latest dip comes after a modest run, but zooming out shows the bigger picture: the 1-year total shareholder return stands at 6.6%, and the stock has delivered an impressive 48% total return over the past five years. This momentum has steadied even as some tech peers have stumbled. Recent gains suggest investors are weighing steady fundamentals against valuation, hinting at possible renewed interest if Dropbox continues to deliver consistent results.

If you’re curious about what else could be gathering steam beyond the obvious choices, now’s the perfect moment to see what’s next with our fast growing stocks with high insider ownership.

The question for investors now is whether Dropbox is undervalued based on its fundamentals, or if the recent run means the market has already factored in all the future growth potential.

Advertisement

Most Popular Narrative: 6% Overvalued

Dropbox is trading above the fair value estimate set by the most widely followed narrative, with the latest close at $29.84 versus a calculated fair value of $28.13. This puts the market's expectations somewhat ahead of the narrative's case. The rationale hinges on Dropbox’s revenue, margin, and user base dynamics in coming years.

Persistent emphasis on operational efficiency, via infrastructure optimization, disciplined hiring, and lower marketing spend, has resulted in sustained improvements in non-GAAP operating margins and free cash flow. This has enhanced the company's ability to invest in long-term growth areas while also supporting increasing earnings and cash flow per share.

Curious what keeps Dropbox’s fair value below its current price? There is a key assumption about near-term revenue trends and expense discipline that anchors this outlook. Only those who go further will see the crucial growth and margin forecasts that tip the scales in this narrative’s fair value.

However, persistent revenue declines and intensifying competition from larger cloud providers could challenge Dropbox’s growth trajectory and put this optimistic narrative to the test.

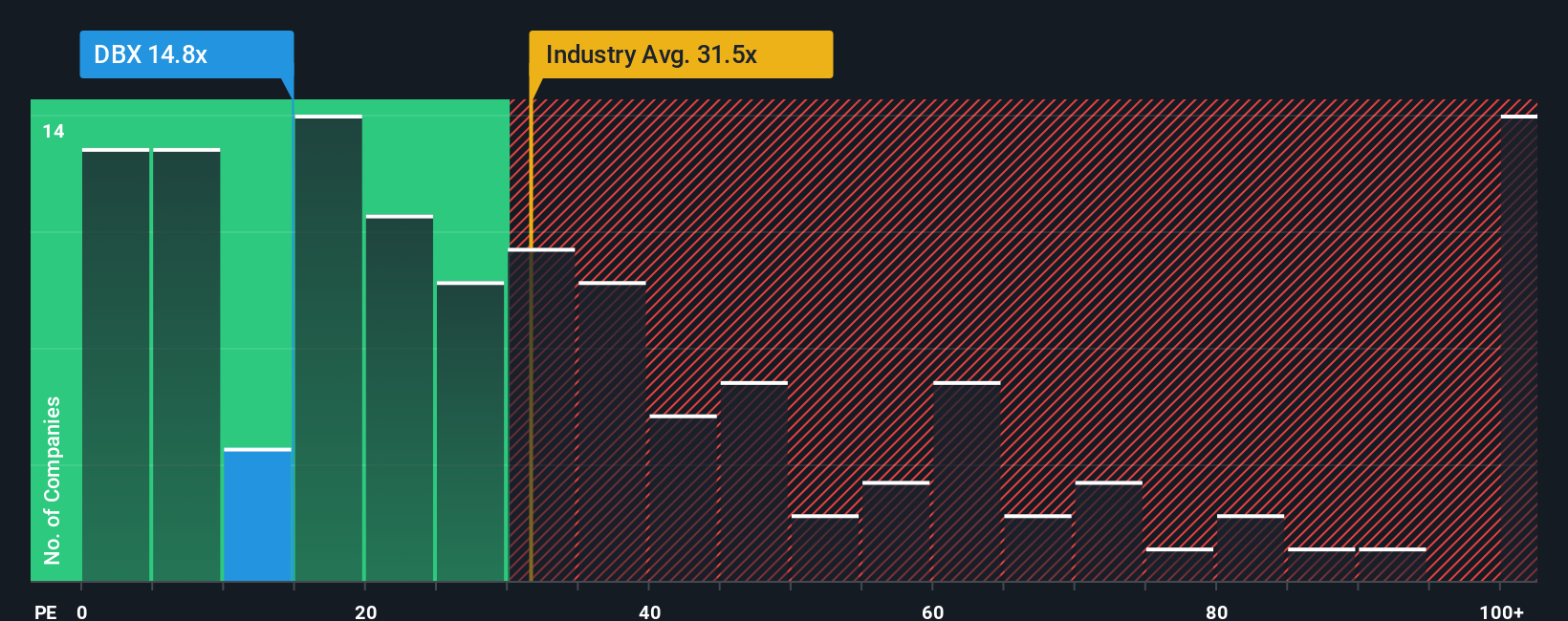

While analysts estimate Dropbox's stock is a bit overvalued against their fair value target, typical valuation ratios paint a different picture. Dropbox trades at 15.4 times earnings, much lower than both its industry average of 30.4 and the peer average of 35. The fair ratio is 24.9, suggesting plenty of room for the market to re-rate upwards if sentiment shifts. Does the market see a bargain others are missing?

Spot technology pioneers early by tracking these 26 AI penny stocks that are positioned to capitalize on breakthroughs in artificial intelligence and machine learning.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks