Advertisement

- United States

- /

- Software

- /

- NasdaqGS:DBX

Does Dropbox’s AI Push Signal a Long Term Value Opportunity in 2025?

Reviewed by Bailey Pemberton

- If you are wondering whether Dropbox is quietly turning into a value opportunity while many investors focus on flashier tech names, this breakdown is for you.

- The stock is down 2.8% over the last week, 5.8% over the last month, and 3.3% year to date, but it is still up 27.7% over three years and 15.0% over five years, which tells a very different longer term story.

- Recent headlines have focused on Dropbox sharpening its product focus and pushing harder into AI driven features and workflow automation. This strategic shift has caught the eye of both investors and competitors. At the same time, ongoing discussions around cost discipline and capital allocation have added more nuance to how the market is pricing the stock's future growth.

- In our framework, Dropbox scores 5 out of 6 on valuation checks, which you can see in detail in its valuation score. Next, we will walk through those methods one by one, before finishing with a more holistic way to think about what the market might be missing.

Find out why Dropbox's -7.2% return over the last year is lagging behind its peers.

Approach 1: Dropbox Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting its future cash flows and discounting them back to today, to reflect risk and the time value of money.

For Dropbox, the model starts with last twelve month free cash flow of about $906 million, a strong base for a mid cap software business. Analysts provide detailed estimates for the next few years, and Simply Wall St then extrapolates those trends over a 10 year period. On this view, Dropbox is expected to be generating around $1.3 billion in free cash flow by 2035, with growth gradually slowing as the business matures.

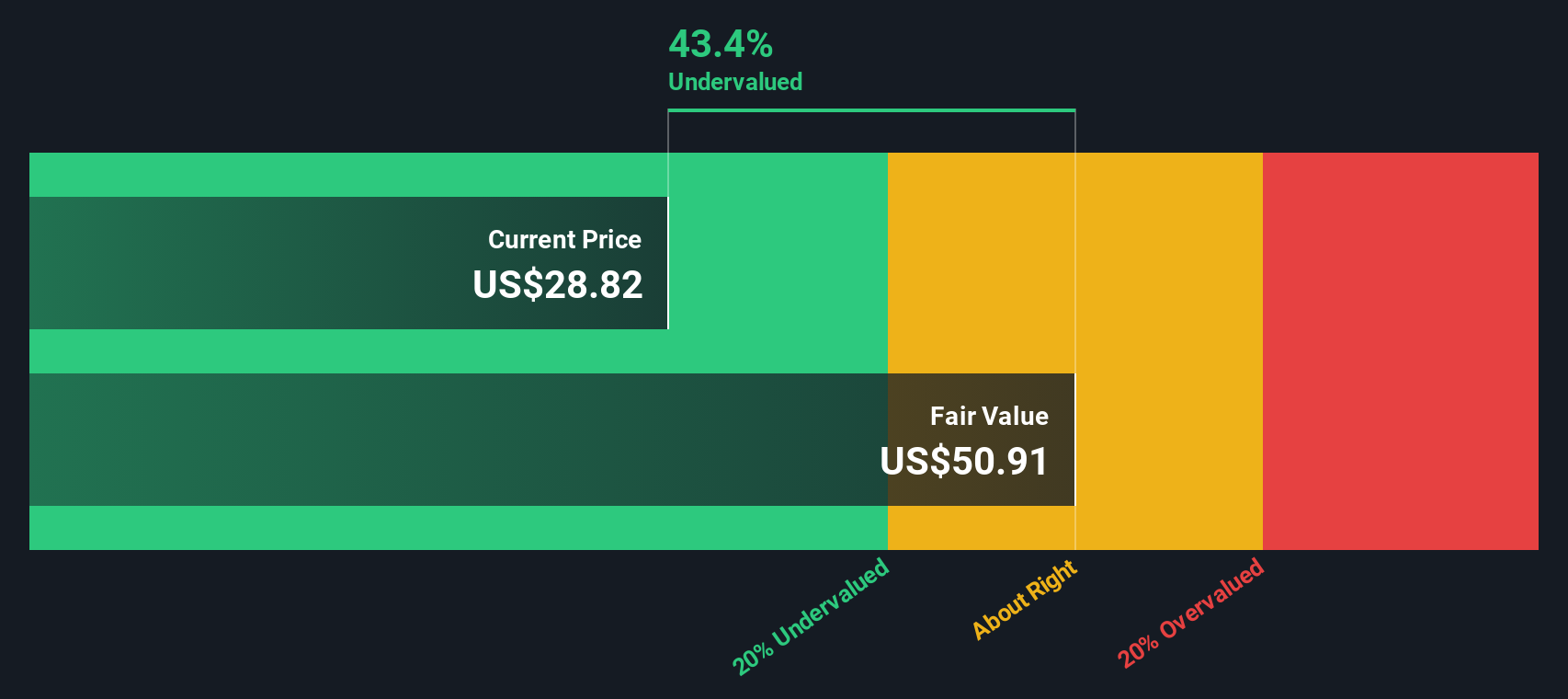

When all of those projected cash flows are discounted back and combined with a reasonable long term growth assumption, the DCF model arrives at an intrinsic value of about $58.04 per share. Compared with the current market price, this implies the stock is trading at roughly a 50.7% discount.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Dropbox is undervalued by 50.7%. Track this in your watchlist or portfolio, or discover 909 more undervalued stocks based on cash flows.

Approach 2: Dropbox Price vs Earnings

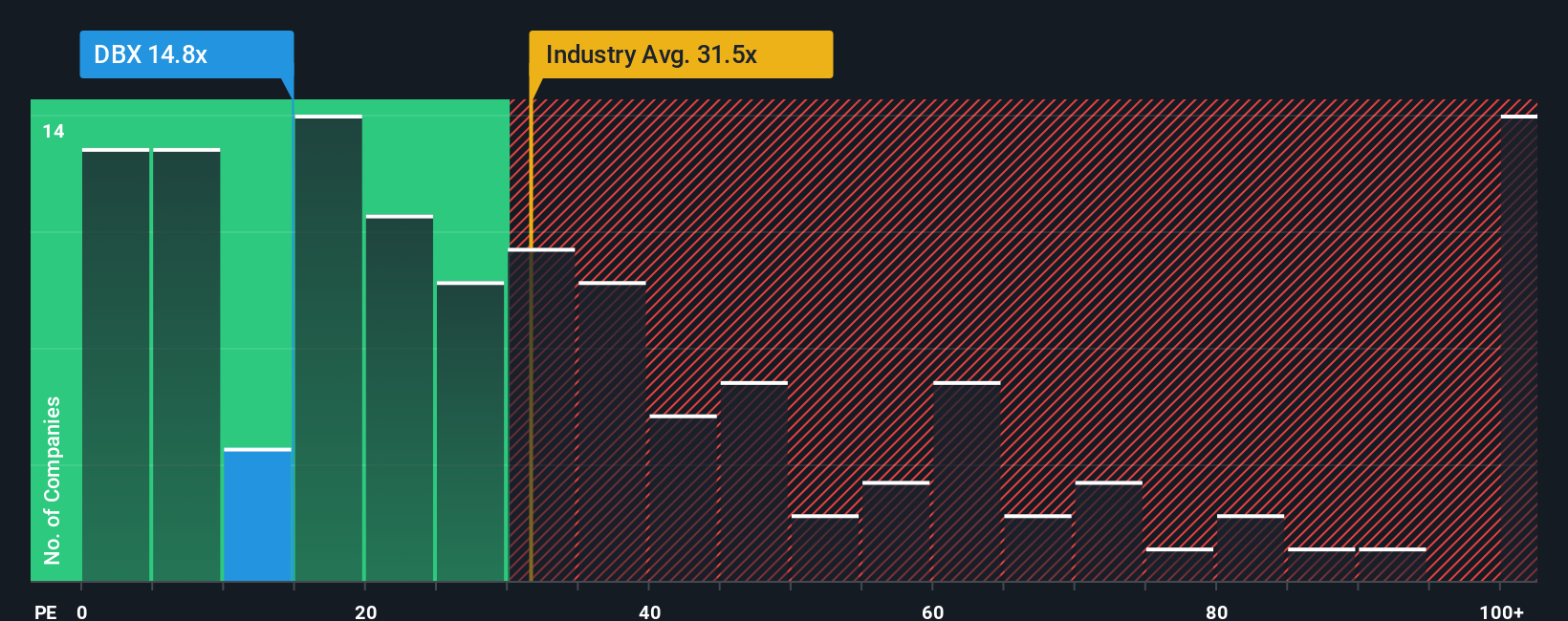

For a consistently profitable business like Dropbox, the price to earnings, or PE, ratio is a useful way to judge whether investors are paying a reasonable price for each dollar of earnings. In general, faster growth and lower perceived risk justify a higher PE, while slower growth, more cyclicality, or higher uncertainty tend to pull a fair PE lower.

Dropbox currently trades on a PE of about 14.7x, which is well below both the wider Software industry average of roughly 32.7x and the 23.5x average of closer peers. Simply Wall St also calculates a proprietary Fair Ratio of 24.4x, which is the PE you might expect for Dropbox given its specific earnings growth profile, margins, industry, market cap, and risk factors.

This Fair Ratio is more informative than a simple comparison with industry or peer averages, because it adjusts for Dropbox’s own strengths and weaknesses rather than assuming it should trade like a typical software stock. Setting the Fair Ratio of 24.4x against the current 14.7x multiple suggests the market is applying a sizable discount to what looks like a reasonable valuation baseline.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1463 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Dropbox Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, an easy tool on Simply Wall St's Community page that lets you turn your view of Dropbox into a coherent story that links its business drivers, a financial forecast, and a resulting fair value. Narratives then continuously update that story when new information arrives, so you can compare your Narrative fair value to the current share price and decide whether to buy, hold, or sell. You can also see how other investors may, for example, build a bullish Narrative that leans on deeper AI integration, margin expansion, and a fair value closer to $35, or a more cautious Narrative that stresses revenue decline, competition, and a fair value nearer $20.

Do you think there's more to the story for Dropbox? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DBX

Dropbox

Provides a content collaboration platform in the United States and internationally.

Undervalued with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.563.6% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$4811.0% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5446.8% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8212.9% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

TR

TripleS on AnaptysBio ·

ANAB has a scaling and rising royalty stream, one up and coming new royalty, a loan that dies in 2027 which will result in a doubling

Fair Value:US$9025.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GE

Germaine on MM Computer Systems Berhad ·

MM Computer Systems' Latest Contract Wins Reinforce Growth Momentum After Listing

Fair Value:RM 0.3313.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

TripleS on Energy World ·

EWC trades at A$0.052. It carries no debt, just agreed to sell its turbines for US$350m (~A$500m), and once that cash lands the compan

Fair Value:AU$0.1151.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75031.5% undervalued

79 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.9% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7441.2% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative