Advertisement

- United States

- /

- Software

- /

- NasdaqGS:CRWD

Is CrowdStrike (CRWD) Pricing Reflect Recent Pullback And Cybersecurity Momentum Accurately

Reviewed by Bailey Pemberton

- If you are looking at CrowdStrike Holdings and wondering whether the current share price lines up with the underlying business, this article will walk through what the numbers are actually saying about value.

- The stock last closed at US$415.36, with returns of 11.5% decline over 7 days, 9.0% decline over 30 days, 8.4% decline year to date, 0.4% decline over 1 year, 262.8% over 3 years and 79.5% over 5 years. These figures give important context before comparing that price to any estimate of fair value.

- Recent news around CrowdStrike has focused on the company's role in cybersecurity and its position within the broader software sector. This helps frame how investors think about both growth potential and risk. This backdrop is important when you weigh up whether recent price moves reflect changing expectations about the business or simply shorter term sentiment shifts.

- Our valuation framework gives CrowdStrike a 3 out of 6 valuation score, showing it screens as undervalued on half of our checks. Next we will walk through those methods, before finishing with a different way of thinking about valuation that many investors may find even more useful.

Approach 1: CrowdStrike Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes estimates of the cash a business could generate in the future, then discounts those projected cash flows back to today to arrive at an estimate of what the entire company might be worth in the present.

For CrowdStrike Holdings, the model used is a 2 Stage Free Cash Flow to Equity approach. The latest twelve months Free Cash Flow is about $1.11b. Analysts provide detailed forecasts for the next few years, and Simply Wall St extends those projections further out, with Free Cash Flow for 2031 estimated at $6.48b, alongside a full set of discounted cash flow figures running through 2035.

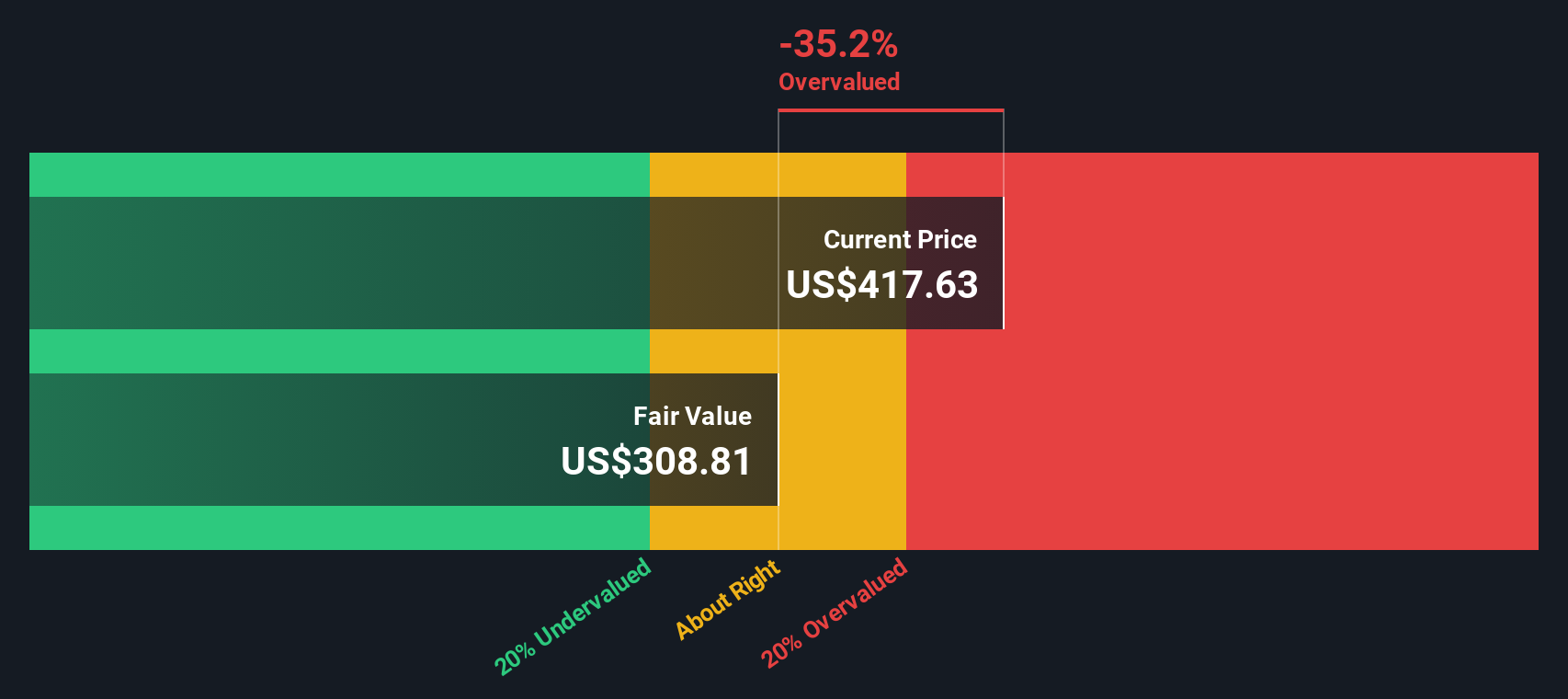

Pulling all those discounted cash flows together, the model arrives at an estimated intrinsic value of US$522.22 per share, compared to the recent share price of US$415.36. The implied intrinsic discount is 20.5%, which indicates that the shares screen as undervalued on this measure.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests CrowdStrike Holdings is undervalued by 20.5%. Track this in your watchlist or portfolio, or discover 867 more undervalued stocks based on cash flows.

Approach 2: CrowdStrike Holdings Price vs Sales

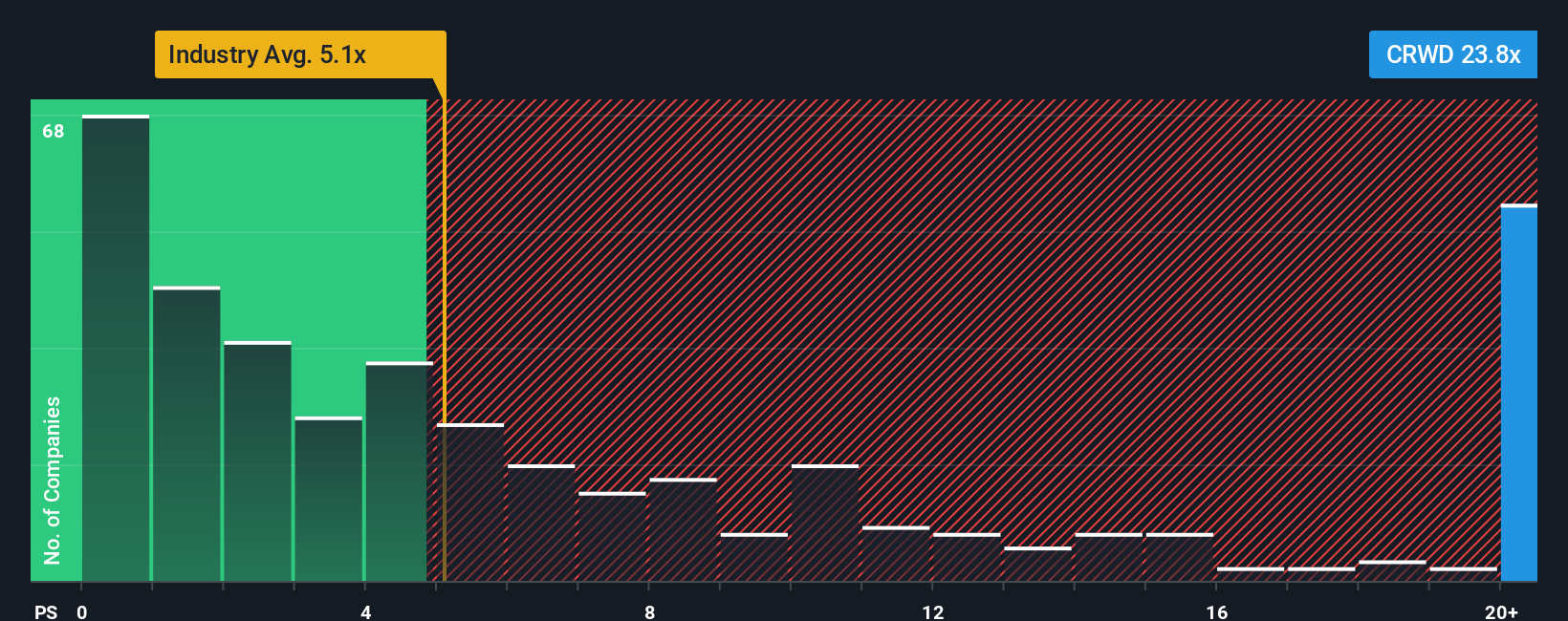

For companies where investors focus heavily on revenue growth and scale, the Price to Sales, or P/S, ratio is a useful cross check on value, because it compares what the market is paying to each dollar of current sales.

Higher growth expectations and lower perceived risk tend to justify a higher “normal” P/S ratio, while slower expected growth or higher risk usually line up with a lower multiple. That context matters when you compare CrowdStrike Holdings to other software names.

CrowdStrike currently trades on a P/S ratio of 22.94x. This sits well above the Software industry average of 3.89x and also above the selected peer group average of 10.14x, which on simple comparison might suggest a rich valuation.

Simply Wall St’s Fair Ratio framework estimates what a more tailored P/S multiple could look like by blending factors such as CrowdStrike’s revenue growth profile, margins, size, sector and risk indicators. Because it adjusts for these company specific drivers, it can be more informative than a straight comparison with industry or peer averages.

The Fair Ratio for CrowdStrike is 13.54x, which is below the current 22.94x, indicating that on this metric the shares screen as overvalued.

Result: OVERVALUED

P/S ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1433 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your CrowdStrike Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way for you to attach your own story about CrowdStrike to the numbers behind its fair value, revenue, earnings and margins.

A Narrative links what you believe about the business to a clear forecast, then connects that forecast to a fair value estimate that you can compare directly with the current share price to help decide whether you want to buy, hold or sell.

On Simply Wall St, Narratives sit inside the Community page and are designed to be easy to use. They automatically refresh when new information such as earnings releases or major news is added, so your story and numbers stay aligned with the latest data.

For example, one CrowdStrike Narrative might assume a very high fair value because the creator expects strong revenue growth and robust margins. Another might set a much lower fair value based on more modest growth and profitability assumptions, giving you a clear view of how different views on the same company translate into different price expectations.

Do you think there's more to the story for CrowdStrike Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CRWD

CrowdStrike Holdings

Provides cybersecurity solutions in the United States and internationally.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7063.1% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.5% undervalued

47 followersusers have followed this narrative

8 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0539.5% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15121.8% undervalued

91 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Investigator Silver ·

Investigator Silver, Leverage Exposed: $1/oz Move = $42M Cash for This ASX Developer

Fair Value:AU$2.3997.7% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

TA

Talos on Voyager Technologies ·

The "Landlord of Orbit" – A Deep Value Play Ahead of the Starlab Era

Fair Value:US$385.289.5% undervalued

18 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Advanced Micro Devices ·

The "David vs. Goliath" AI Trade – Why Second Place is Worth Billions

Fair Value:US$907.3239.7% undervalued

38 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.3% undervalued

66 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1929.0% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9721.9% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative