Advertisement

- United States

- /

- Software

- /

- NasdaqGS:CRNC

Cerence (NASDAQ:CRNC) Is Looking To Continue Growing Its Returns On Capital

There are a few key trends to look for if we want to identify the next multi-bagger. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. With that in mind, we've noticed some promising trends at Cerence (NASDAQ:CRNC) so let's look a bit deeper.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for Cerence, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

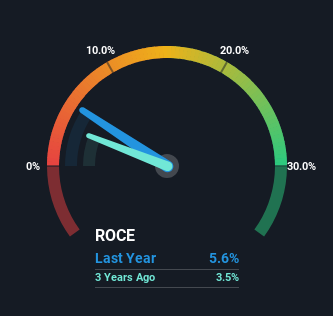

0.056 = US$49m ÷ (US$987m - US$107m) (Based on the trailing twelve months to March 2024).

So, Cerence has an ROCE of 5.6%. In absolute terms, that's a low return and it also under-performs the Software industry average of 7.5%.

View our latest analysis for Cerence

In the above chart we have measured Cerence's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free analyst report for Cerence .

The Trend Of ROCE

You'd find it hard not to be impressed with the ROCE trend at Cerence. The figures show that over the last five years, returns on capital have grown by 88%. That's not bad because this tells for every dollar invested (capital employed), the company is increasing the amount earned from that dollar. Interestingly, the business may be becoming more efficient because it's applying 31% less capital than it was five years ago. If this trend continues, the business might be getting more efficient but it's shrinking in terms of total assets.

What We Can Learn From Cerence's ROCE

In summary, it's great to see that Cerence has been able to turn things around and earn higher returns on lower amounts of capital. Although the company may be facing some issues elsewhere since the stock has plunged 97% in the last three years. Regardless, we think the underlying fundamentals warrant this stock for further investigation.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 3 warning signs for Cerence (of which 1 can't be ignored!) that you should know about.

While Cerence isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CRNC

Cerence

Provides AI-powered assistants for the mobility/transportation market in the United States, the rest of the Americas, Germany, the rest of Europe, the Middle East, Africa, Japan, and the rest of the Asia-Pacific.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4346.7% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

ZA

ZayaanS on Pro Medicus ·

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

Fair Value:AU$196.7838.3% undervalued

26 followersusers have followed this narrative

4 commentsusers have commented on this narrative

18 likesusers have liked this narrative

ST

SteveGruber on Warner Bros. Discovery ·

The Rising Deal Risk That Helped Sink Netflix’s $72 Billion Bid for Warner Bros. Discovery

Fair Value:US$18.1753.8% overvalued

5 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6438.5% undervalued

31 followersusers have followed this narrative

3 commentsusers have commented on this narrative

13 likesusers have liked this narrative

Recently Updated Narratives

AN

andre_santos on Realty Income ·

Realty Income - A Fundamental and Historical Valuation

Fair Value:US$73.4610.2% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HP

HpN on Microsoft ·

A Structured Counter‑Analysis of "The Leaking Dreadnought"

Fair Value:US$509.8220.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Alphabet ·

Alphabet Inc. (GOOG): The Gemini Era – Consolidating AI Dominance in 2026.

Fair Value:US$35514.6% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.888.0% undervalued

65 followersusers have followed this narrative

5 commentsusers have commented on this narrative

28 likesusers have liked this narrative

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.376.7% undervalued

48 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59632.0% undervalued

1299 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative