Advertisement

- United States

- /

- Software

- /

- NasdaqGS:CHKP

Returns At Check Point Software Technologies (NASDAQ:CHKP) Appear To Be Weighed Down

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. Having said that, while the ROCE is currently high for Check Point Software Technologies (NASDAQ:CHKP), we aren't jumping out of our chairs because returns are decreasing.

Return On Capital Employed (ROCE): What Is It?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on Check Point Software Technologies is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

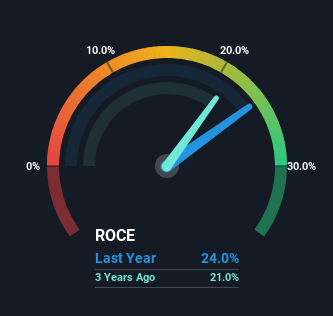

0.24 = US$897m ÷ (US$5.5b - US$1.8b) (Based on the trailing twelve months to June 2023).

Therefore, Check Point Software Technologies has an ROCE of 24%. In absolute terms that's a great return and it's even better than the Software industry average of 9.2%.

View our latest analysis for Check Point Software Technologies

In the above chart we have measured Check Point Software Technologies' prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Check Point Software Technologies here for free.

The Trend Of ROCE

There hasn't been much to report for Check Point Software Technologies' returns and its level of capital employed because both metrics have been steady for the past five years. Businesses with these traits tend to be mature and steady operations because they're past the growth phase. Although current returns are high, we'd need more evidence of underlying growth for it to look like a multi-bagger going forward.

On another note, while the change in ROCE trend might not scream for attention, it's interesting that the current liabilities have actually gone up over the last five years. This is intriguing because if current liabilities hadn't increased to 32% of total assets, this reported ROCE would probably be less than24% because total capital employed would be higher.The 24% ROCE could be even lower if current liabilities weren't 32% of total assets, because the the formula would show a larger base of total capital employed. With that in mind, just be wary if this ratio increases in the future, because if it gets particularly high, this brings with it some new elements of risk.

In Conclusion...

While Check Point Software Technologies has impressive profitability from its capital, it isn't increasing that amount of capital. Unsurprisingly, the stock has only gained 15% over the last five years, which potentially indicates that investors are accounting for this going forward. As a result, if you're hunting for a multi-bagger, we think you'd have more luck elsewhere.

If you're still interested in Check Point Software Technologies it's worth checking out our FREE intrinsic value approximation to see if it's trading at an attractive price in other respects.

Check Point Software Technologies is not the only stock earning high returns. If you'd like to see more, check out our free list of companies earning high returns on equity with solid fundamentals.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:CHKP

Check Point Software Technologies

Develops, markets, and supports a range of products and services for IT security worldwide.

Outstanding track record and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3447.6% undervalued

39 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.1% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.652.3% undervalued

30 followersusers have followed this narrative

2 commentsusers have commented on this narrative

15 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£162.2% undervalued

40 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

DA

davidlsander on Vulcan Minerals ·

Uncovering The Hidden Annuity: Why Vulcan Minerals (TSXV:VUL) Trades At A Massive Discount To Its Sum-Of-The-Parts

Fair Value:CA$2.2378.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Rog on CTT - Correios De Portugal ·

Why CTT benefits in multiple ways right now

Fair Value:€7.6721.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Adecoagro ·

Why a "2026 Super El Nino" is the Ultimate Hedge for Tech-Heavy Portfolios

Fair Value:US$18.2849.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.0% undervalued

60 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.5% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative