Advertisement

- United States

- /

- Software

- /

- NasdaqGS:CHKP

Earnings Update: Here's Why Analysts Just Lifted Their Check Point Software Technologies Ltd. (NASDAQ:CHKP) Price Target To US$186

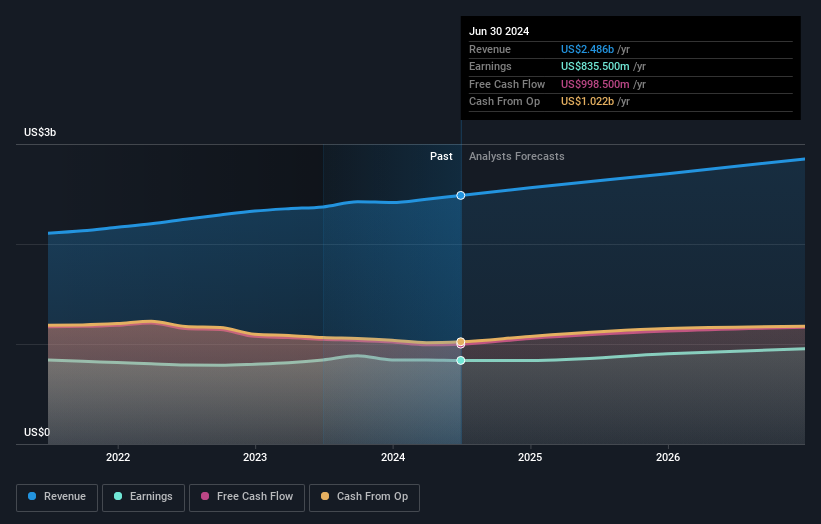

It's been a good week for Check Point Software Technologies Ltd. (NASDAQ:CHKP) shareholders, because the company has just released its latest second-quarter results, and the shares gained 5.3% to US$181. Check Point Software Technologies reported in line with analyst predictions, delivering revenues of US$627m and statutory earnings per share of US$1.74, suggesting the business is executing well and in line with its plan. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

See our latest analysis for Check Point Software Technologies

After the latest results, the 34 analysts covering Check Point Software Technologies are now predicting revenues of US$2.56b in 2024. If met, this would reflect a reasonable 3.1% improvement in revenue compared to the last 12 months. Statutory per-share earnings are expected to be US$7.40, roughly flat on the last 12 months. In the lead-up to this report, the analysts had been modelling revenues of US$2.56b and earnings per share (EPS) of US$7.38 in 2024. So it's pretty clear that, although the analysts have updated their estimates, there's been no major change in expectations for the business following the latest results.

The consensus price target rose 8.2% to US$186despite there being no meaningful change to earnings estimates. It could be that the analystsare reflecting the predictability of Check Point Software Technologies' earnings by assigning a price premium. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Check Point Software Technologies, with the most bullish analyst valuing it at US$215 and the most bearish at US$110 per share. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's clear from the latest estimates that Check Point Software Technologies' rate of growth is expected to accelerate meaningfully, with the forecast 6.3% annualised revenue growth to the end of 2024 noticeably faster than its historical growth of 5.1% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to see revenue growth of 12% annually. It seems obvious that, while the future growth outlook is brighter than the recent past, Check Point Software Technologies is expected to grow slower than the wider industry.

The Bottom Line

The most obvious conclusion is that there's been no major change in the business' prospects in recent times, with the analysts holding their earnings forecasts steady, in line with previous estimates. On the plus side, there were no major changes to revenue estimates; although forecasts imply they will perform worse than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Check Point Software Technologies going out to 2026, and you can see them free on our platform here..

You can also see our analysis of Check Point Software Technologies' Board and CEO remuneration and experience, and whether company insiders have been buying stock.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CHKP

Check Point Software Technologies

Develops, markets, and supports a range of products and services for IT security worldwide.

Outstanding track record and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc Al ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.254.8% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

SO

sorkdhkddlek on Marvell Technology ·

From AI Infrastructure Plumber to Full-Stack AI Factory Architect

Fair Value:US$14017.8% overvalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

MI

MiningStockAnalyst on Aurelia Metals ·

Aurelia Metals Limited — Transitioning Into a Higher-Quality Mid-Tier Producer

Fair Value:AU$0.427.5% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

CO

composite32 on TotalEnergies ·

Is This strategic transformation of TTE? Significant re-rating potential

Fair Value:€88.2910.2% undervalued

16 followersusers have followed this narrative

2 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74017.7% undervalued

30 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

SI

Silvester on Prospect Capital ·

PSEC Contrary investing

Fair Value:US$2.93.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agape on Berkshire Hathaway ·

Thinking on BRKB

Fair Value:US$669.76k99.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.235.0% undervalued

68 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9326.2% undervalued

1395 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74017.7% undervalued

30 followersusers have followed this narrative

3 commentsusers have commented on this narrative

31 likesusers have liked this narrative