Advertisement

- United States

- /

- Software

- /

- NasdaqGS:CHKP

Assessing Check Point After New Cloud Security Launch and Recent Share Price Rebound

Reviewed by Bailey Pemberton

If you have been wrestling with the "hold or sell" question on Check Point Software Technologies, you are definitely not alone. Lately, the stock has given investors a bit of everything: resilience, volatility, and some deep questions on where true value lies. Over the last week, shares picked up 2.8%, which seems to reflect a slight rebound in optimism, even as the 1-year return sits at -5.8%. Stretch your horizon, though, and you see healthy gains of 52.1% over three years and an impressive 67.1% in five, underscoring the company’s longer-term staying power and reminding us that timing, as always, matters.

What’s driving this roller coaster? While the security software industry as a whole has been in the spotlight given increased threats and global chatter about cybersecurity, Check Point has also made quieter moves such as unveiling new cloud security solutions and deepening partnerships with large enterprise clients, actions that boost its value proposition but may not always spark major price leaps on their own. This recent news is building a foundation, reinforcing the company’s reputation as an innovation leader and signaling future growth streams that the market could be starting to recognize more fully.

But is the current valuation fair, generous, or too tight for comfort? According to our framework, Check Point scores a 3 out of 6 on value checks, an intriguing sign there may be areas of undervaluation, but also pockets where the price looks more demanding. To really get a read on where value stands, let’s break things down by key valuation approaches. And just when you think you have seen it all, stick around as we will wrap up with a perspective on valuation that most investors overlook.

Why Check Point Software Technologies is lagging behind its peers

Approach 1: Check Point Software Technologies Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and discounting them to the present. This provides a detailed snapshot of what the business might be worth today based on its ability to generate money going forward.

For Check Point Software Technologies, the latest reported Free Cash Flow stands at $1.15 Billion. Analysts forecast moderate but steady growth, with projections estimating free cash flows will reach $1.42 Billion by 2029. While direct analyst insights typically cover the next five years, subsequent forecasts rely on longer-term extrapolations. Over the next decade, free cash flows are expected to continue this upward trend, though at a gradually decelerating pace.

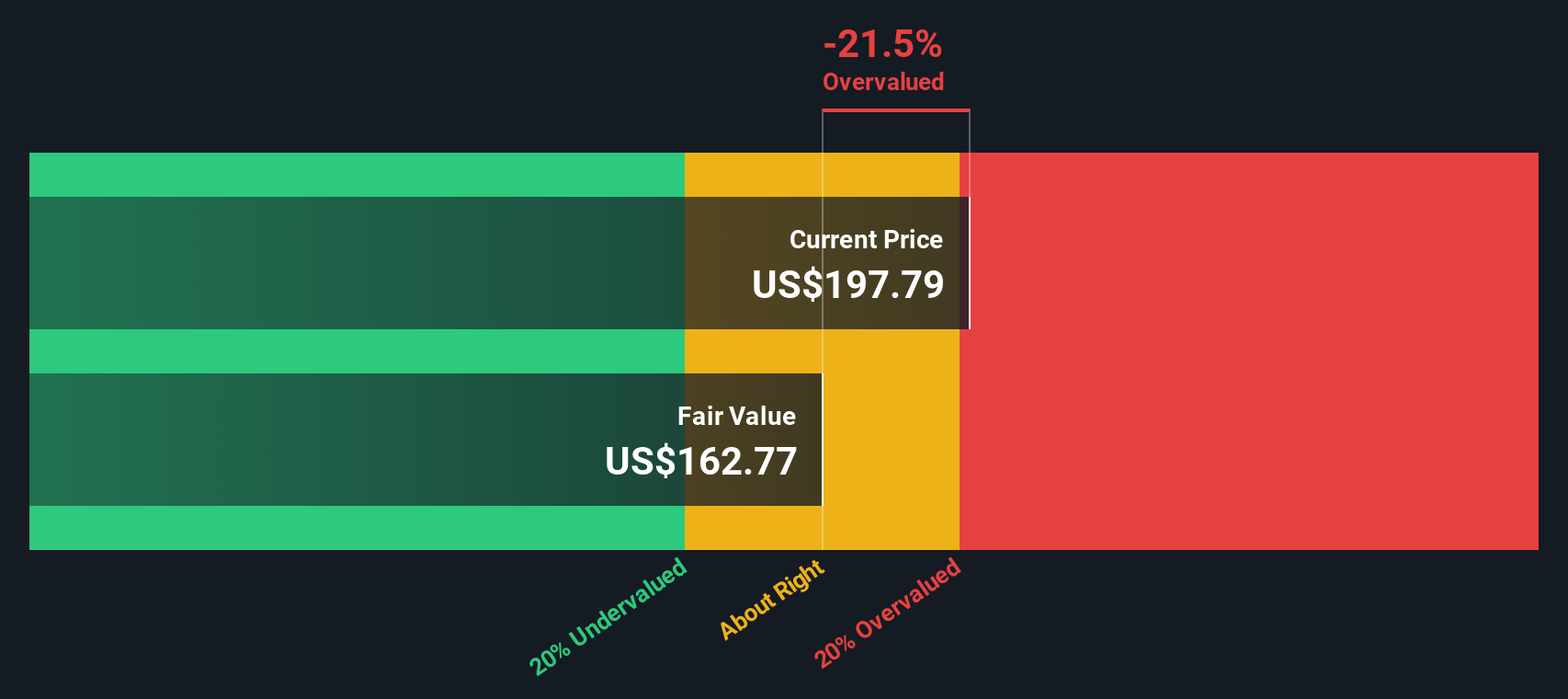

Based on this two-stage Free Cash Flow to Equity model, the DCF valuation suggests an intrinsic value of $164.79 per share. Notably, this is about 17.5% higher than the company's current trading level, meaning the stock is currently priced above what the DCF model deems fair. In other words, investors looking at cash flow fundamentals may find the stock somewhat expensive at present.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Check Point Software Technologies may be overvalued by 17.5%. Find undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Check Point Software Technologies Price vs Earnings

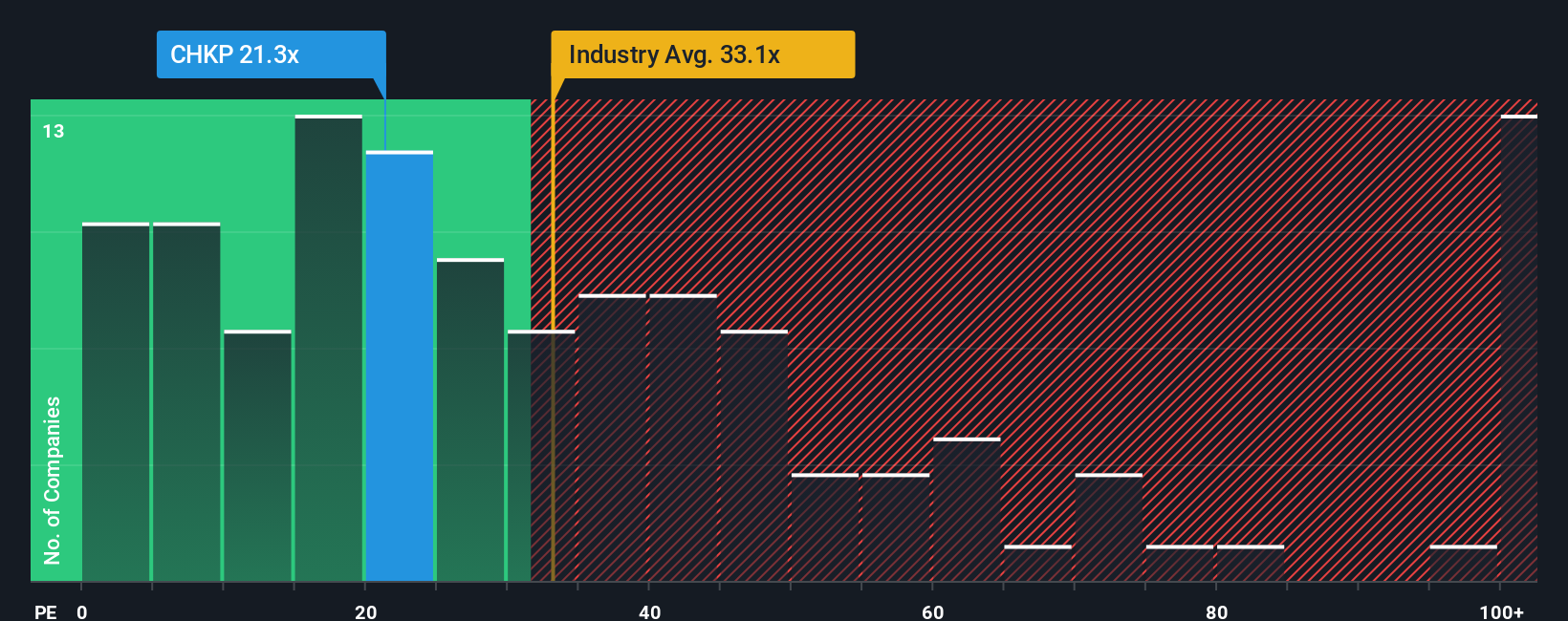

The Price-to-Earnings (PE) ratio is often considered the go-to metric when evaluating profitable, established companies because it connects a company's share price to its actual earnings performance. For businesses that consistently generate healthy profits, like Check Point Software Technologies, the PE ratio provides a direct and transparent snapshot of what investors are willing to pay for each dollar of profit.

However, context matters. Higher growth and lower perceived risk usually justify a steeper PE, while slower-growing or more volatile firms typically warrant lower multiples. That’s why it is best to avoid snap judgments. What is fair in one corner of the market is not always a match elsewhere.

Right now, Check Point trades at a PE of 24.2x. To put that into perspective, it sits well below both the broader software industry average of 34.3x and a peer group average of 44.6x. Yet, numbers on their own can be misleading. This is where Simply Wall St’s ‘Fair Ratio’ comes in: a proprietary benchmark that blends growth prospects, profit margins, risk profile, industry norms, and even company size to arrive at a PE you would expect for a business like Check Point. The Fair Ratio here is 29.5x, which may offer the best apples-to-apples comparison available.

Given Check Point's current PE is about 5.3x below its Fair Ratio, the stock appears undervalued by this measure, suggesting the market may be glossing over some of its strengths or potential.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Check Point Software Technologies Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. Narratives are easy, story-driven forecasts that empower you to tell your own version of a company’s future, connecting your personal expectations for Check Point Software Technologies’ business performance with the numbers, right through to a fair value estimate.

With Narratives on Simply Wall St’s Community page, millions of investors can combine what they believe about the company’s future growth, earnings potential, and risks into a quick, dynamic forecast that provides a fair value updated automatically if new news or results emerge. This approach brings the story and the stats together, making it effortless to compare your Fair Value to the current share price, and decide whether it is time to buy, hold, or sell.

For example, some investors now think Check Point’s transformative AI and SASE initiatives support a fair value as high as $285, while more cautious perspectives focused on margin pressure, competitive threats, and macro risks set it as low as $173. Narratives make these differing outlooks visible, showing you the range of real-world scenarios that could shape your next investment move.

Do you think there's more to the story for Check Point Software Technologies? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CHKP

Check Point Software Technologies

Develops, markets, and supports a range of products and services for IT security worldwide.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

113 followersusers have followed this narrative

1 commentusers have commented on this narrative

20 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9819.4% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

29 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.0% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3650.4% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

AG

Agricola on NeXGold Mining ·

A Case For NeXGold Mining Corp, a 20+ bagger by 2030 (C$40-70) or a 10 bagger by Christmas 2026 (C$16), or both?

Fair Value:CA$5597.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AnimalDoctorKwon on Charles River Laboratories International ·

A Company Preparing for the Future: Charles River Laboratories

Fair Value:US$313.6146.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CR

CrayonDave on New Found Gold ·

The Birth of a High-Grade Canadian Gold Powerhouse

Fair Value:US$5.0850.6% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.5% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59632.1% undervalued

1306 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0226.5% undervalued

1102 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

Trending Discussion

DA

daqui_luis on Corticeira Amorim S.G.P.S ·

Great analysis on a great and solid company with a dominant position in the Cork Market.

0

|0