Advertisement

- United States

- /

- Software

- /

- NasdaqGS:CFLT

How Does Confluent Stack Up After a 10% Rally Amid AI Adoption Hopes?

Reviewed by Bailey Pemberton

Thinking about whether to buy, hold, or sell Confluent right now? You are not alone. With so many eyes on the tech sector and ever-shifting market sentiment, Confluent’s story keeps getting more interesting. In just the past week, the stock climbed 5.7%, while over the past month it is up 9.9%. This hints that investors are warming up to its prospects again. That strength stands out even more considering that, year-to-date, Confluent shares are still down nearly 25%. Yet, if you zoom out to the past year, it has managed a positive return of 6.5%, showing some real resilience during a tough period for many high growth names.

Much of this volatility can be traced back to shifting views about the company’s market position and technology adoption. There is a sense among investors that data infrastructure providers like Confluent could benefit as more companies seek to modernize their operations. These bright spots help explain why buyers have stepped in after recent pullbacks.

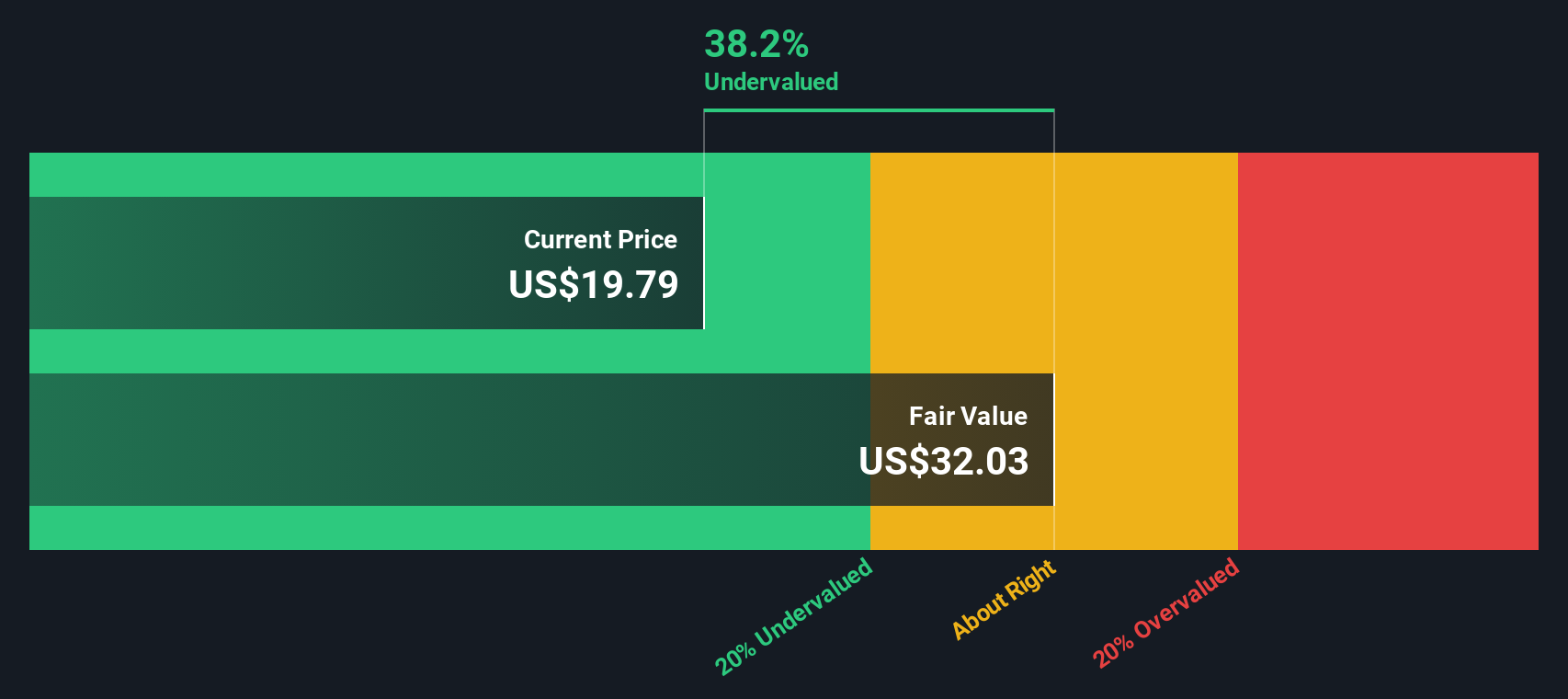

If you are trying to figure out whether the current price delivers value, the numbers offer some clues. Using our six key valuation checks, Confluent scores a 4 out of 6. This signals it is undervalued in most, but not all, areas we track. Of course, each valuation method has its limitations. In the next section, we will break down exactly what those checks are and how Confluent measures up, before exploring an even smarter way to look at its real worth that many investors overlook.

Why Confluent is lagging behind its peers

Approach 1: Confluent Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates the true value of a company by projecting its future cash flows and then discounting those amounts back to today's dollars. This method helps investors understand what Confluent could be worth based on the income it is expected to generate over time.

For Confluent, the most recent Free Cash Flow stands at $15.5 million. Analysts provide free cash flow estimates for the next five years, and based on these projections, as well as longer-term growth rates extrapolated by Simply Wall St, Confluent’s FCF is forecasted to reach $1.02 billion by 2035. This path shows substantial annual growth, with 2029’s free cash flow expected to hit $472.35 million.

Using this two-stage approach, Confluent’s intrinsic value is calculated to be $32.13 per share according to the DCF model. This translates to a roughly 33.8 percent discount from the current market price, indicating the stock is notably undervalued from a cash flow perspective.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Confluent is undervalued by 33.8%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

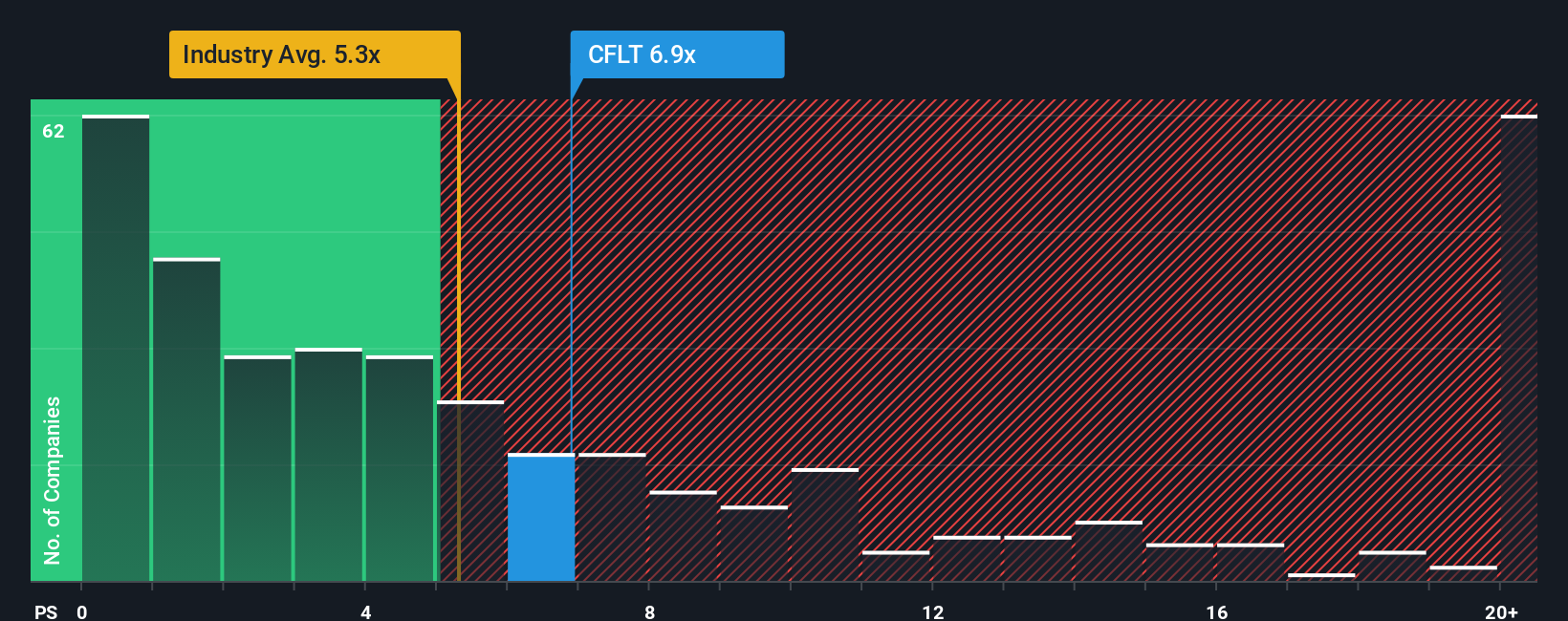

Approach 2: Confluent Price vs Sales

The Price-to-Sales (P/S) ratio is a widely used valuation metric for companies like Confluent that are still scaling up and may not yet be consistently profitable. This multiple enables investors to gauge how much the market values each dollar of revenue, which is especially helpful when profit margins are still evolving or earnings remain negative.

Growth expectations and perceived risk play a big role in shaping what is considered a “normal” or “fair” P/S ratio. Rapidly growing software companies and those with strong competitive positions often command higher ratios, while slower growers or riskier firms typically trade at lower multiples.

Currently, Confluent trades at a P/S ratio of 6.88x. This compares to an average of 5.28x across the Software industry and a peer group average of 9.57x. On the surface, Confluent is more expensive than the industry overall but sits below its closest peers.

To add further nuance, Simply Wall St’s proprietary “Fair Ratio” estimates what a justifiable P/S multiple should be for Confluent, factoring in its growth prospects, profit margins, market cap, and risk. This results in a Fair Ratio of 7.44x. Unlike simple industry or peer comparisons, this metric is tailored specifically to the company’s actual fundamentals and competitive landscape.

Because Confluent’s current P/S ratio is just slightly below its Fair Ratio, shares appear to be valued about right on this measure.

Result: ABOUT RIGHT

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Confluent Narrative

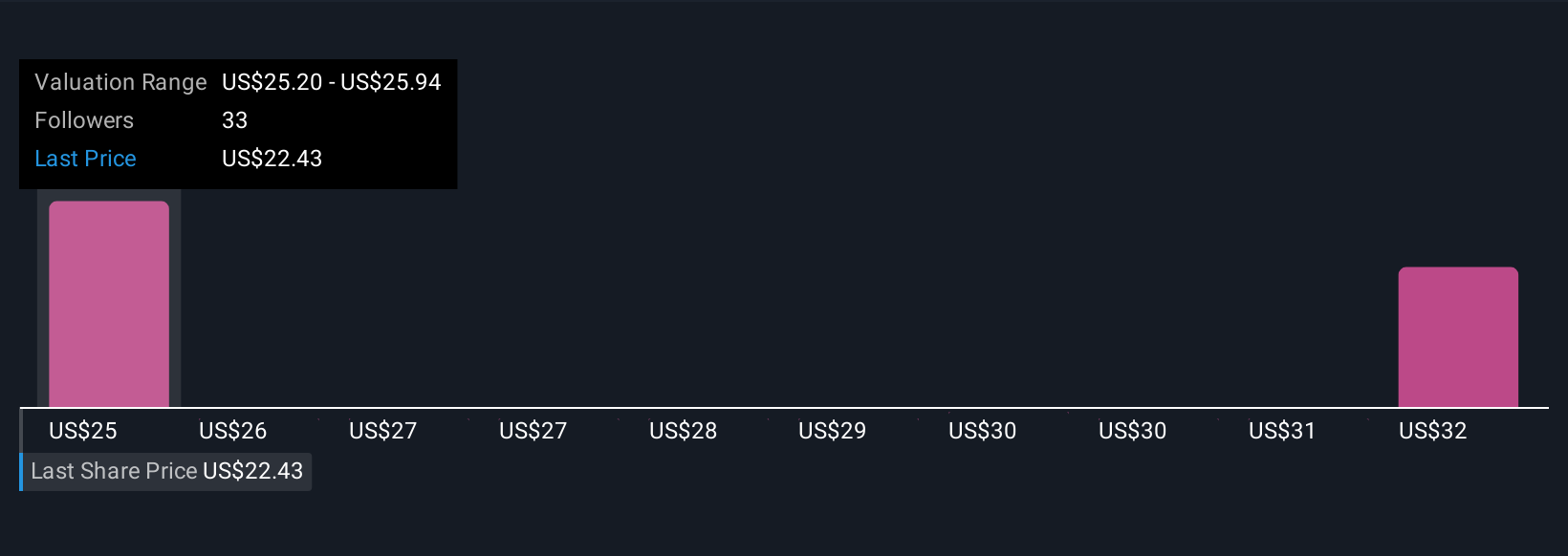

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is your personal investment story that connects what you know about a company, like Confluent’s growth prospects, business risks, and future outcomes, to actual numbers such as estimated future revenue, earnings, and margins. This results in your own view of fair value.

Rather than relying solely on generic ratios or analyst targets, Narratives empower you to combine both the facts and your perspective into a single, actionable view. On Simply Wall St’s Community page, millions of investors use this tool to capture their reasoning, build financial forecasts, and instantly see what price they think a stock is worth. This makes it far easier to spot buy, hold, or sell opportunities by comparing your calculated fair value to the latest market price.

Best of all, Narratives are dynamic, so your assumptions, forecasts, and valuations update as news, earnings, or new data come in, keeping you one step ahead of changes that matter. For example, looking at Confluent right now, some investors forecast rapid AI-driven adoption, supporting a high fair value near $36. Others anticipate slower cloud growth and assign a more conservative value around $20, reflecting different stories and different investment decisions from the same set of information.

Do you think there's more to the story for Confluent? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CFLT

Confluent

Operates a data streaming platform in the United States and internationally.

Excellent balance sheet with very low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1947.9% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7720.4% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19017.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

TH

TheTurntTomato on Opera ·

The Market Is Valuing a Browser While Opera Is Building an AI-Powered Internet Platform

Fair Value:US$26.2925.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TH

TheTurntTomato on Constellium ·

CSTM: A High-Barrier Aerospace and EV Materials Leader Trading at Just 9x Earnings

Fair Value:US$37.1625.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TH

TheTurntTomato on PicS ·

A Fast-Growing Fintech Priced Like a Slow-Growth Bank

Fair Value:US$20.442.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75027.0% undervalued

96 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5457.4% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6512.6% undervalued

65 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

2

|0

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0