Advertisement

- United States

- /

- Software

- /

- NasdaqGS:APP

Assessing AppLovin (APP) After Recent Pullback And Rich Earnings Multiple

Reviewed by Bailey Pemberton

- If you are wondering whether AppLovin shares still offer value after a strong run, this article will walk through what the current price might be implying about the business.

- The stock has seen an 8.5% decline over the last 7 days and a 14.9% decline over the last 30 days, although it is still up 87.3% over the last year and has a very large 3 year return.

- Recent coverage has focused on AppLovin's role as a software platform in the mobile app and advertising space, as investors weigh how its position in that market fits into longer term expectations. This mix of enthusiasm and caution helps explain why the share price has been strong over a year but more volatile in the short term.

- Right now AppLovin scores 1 out of 6 on our valuation checks. Next we will look at what different valuation methods suggest about the stock and then finish with a way to think about value that goes beyond just the usual ratios.

AppLovin scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: AppLovin Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business might be worth today by projecting its future cash flows and discounting them back to the present.

For AppLovin, the model uses a 2 Stage Free Cash Flow to Equity approach based on cash flow projections. The latest twelve month free cash flow is about $3.40b. Analysts provide explicit forecasts for several years, and then Simply Wall St extrapolates further, with projected free cash flow reaching $8.82b in 2030. Discounted values for the 2026 to 2035 period range from about $4.42b to $5.87b per year. These values collectively feed into the model’s estimate.

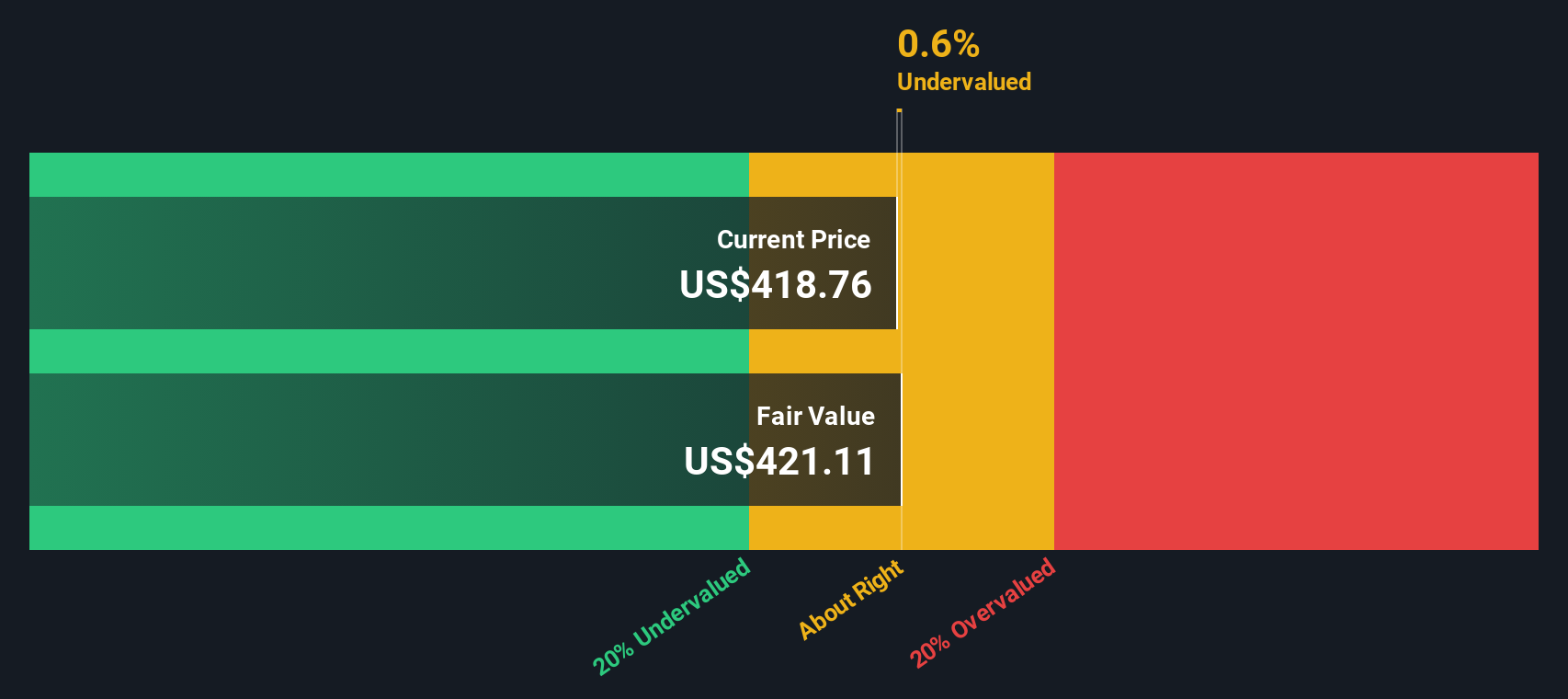

Putting all of this together, the DCF output suggests an estimated intrinsic value of $465.22 per share. Compared with the current share price, the model indicates the stock is about 32.5% overvalued based on these cash flow assumptions and discount rate choices.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests AppLovin may be overvalued by 32.5%. Discover 879 undervalued stocks or create your own screener to find better value opportunities.

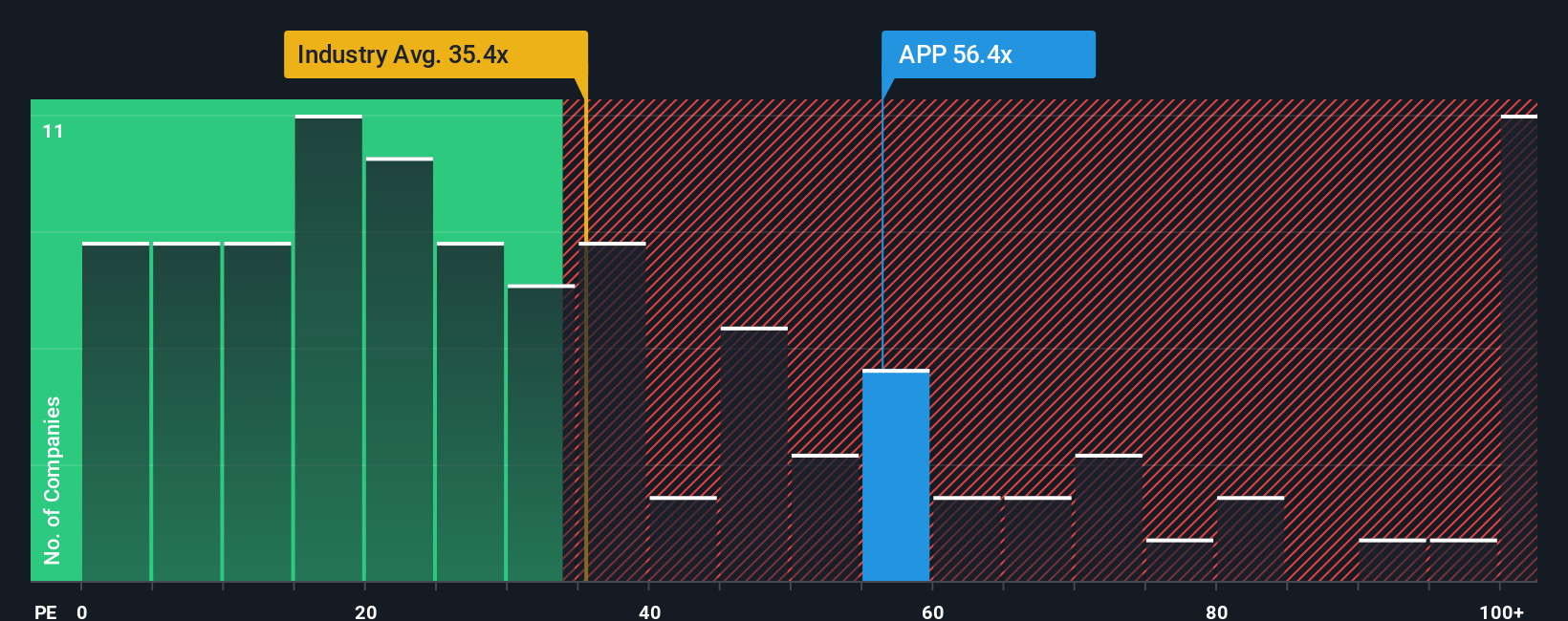

Approach 2: AppLovin Price vs Earnings

For profitable companies, the P/E ratio is a useful way to relate what you pay for a share to the earnings that each share generates. It quickly shows how many years of current earnings the market is effectively paying for.

What counts as a “normal” P/E depends a lot on how fast earnings are expected to grow and how risky those earnings are. Higher growth and lower perceived risk can support a higher P/E, while slower growth or higher uncertainty usually point to a lower P/E being reasonable.

AppLovin currently trades on a P/E of 71.45x. That sits above both the Software industry average P/E of 32.17x and the peer average of 42.87x. Simply Wall St’s Fair Ratio for AppLovin is 54.72x, which is a proprietary estimate of what the P/E might be given factors such as the company’s earnings growth profile, profit margins, industry, market cap and risk characteristics.

Compared with a simple peer or industry comparison, the Fair Ratio aims to be more tailored because it incorporates these company specific drivers rather than treating all software stocks as similar. Since AppLovin’s actual P/E of 71.45x is higher than the Fair Ratio of 54.72x, this approach points to the shares looking expensive on earnings.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your AppLovin Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which let you attach a clear story about AppLovin, including your assumptions for future revenue, earnings and margins, to a financial forecast. You can then link that forecast to a fair value and compare that fair value with today’s price using an easy tool on Simply Wall St’s Community page. This tool updates as new news or earnings arrive. One investor might build a Narrative that lines up with a fair value near the higher end of current community estimates, while another could lean toward the lower end. Both can quickly see whether their own fair value suggests the current price is closer to a buy, hold, or sell decision for them.

Do you think there's more to the story for AppLovin? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:APP

AppLovin

Provides end-to-end artificial intelligence-powered advertising solutions for businesses in the United States and internationally.

Exceptional growth potential with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4342.5% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

ZA

ZayaanS on Pro Medicus ·

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

Fair Value:AU$196.7833.2% undervalued

31 followersusers have followed this narrative

5 commentsusers have commented on this narrative

18 likesusers have liked this narrative

ST

SteveGruber on Warner Bros. Discovery ·

The Rising Deal Risk That Helped Sink Netflix’s $72 Billion Bid for Warner Bros. Discovery

Fair Value:US$18.1752.7% overvalued

5 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6435.3% undervalued

35 followersusers have followed this narrative

3 commentsusers have commented on this narrative

17 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on Toronto-Dominion Bank ·

Toronto-Dominion Bank (TD): Record Earnings Confronting a Multi-Year U.S. Compliance Overhaul.

Fair Value:CA$137.716.0% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Parker-Hannifin ·

Parker-Hannifin Corp (PH): The "Industrial Compounder" Navigating Geopolitical Headwinds and Aerospace Records.

Fair Value:US$1.04k10.4% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Samsung Electronics ·

Samsung Electronics (005930): The HBM4 Counter-Offensive – Reclaiming AI Relevance Amidst Global Macro Chaos.

Fair Value:₩210.61k17.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.2% undervalued

51 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.8% undervalued

1102 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59631.3% undervalued

1302 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative