Advertisement

- United States

- /

- Software

- /

- NasdaqGS:ADSK

Is Autodesk (ADSK) Pricing Reflect Its DCF Estimate After Recent Share Price Weakness

Reviewed by Bailey Pemberton

- If you are wondering whether Autodesk's current share price actually reflects what the business is worth, you are not alone. This article is built to help you connect the dots between the stock and its underlying value.

- The stock recently closed at US$253.85, with returns of 0.2% over the last 7 days, 5.6% over the last 30 days, an 11.5% decline year to date, and 1.2% over the past year, which gives mixed signals about how the market is currently pricing the company.

- Recent coverage around Autodesk has largely focused on its position in design and engineering software and how that ties into long term demand for digital tools, as investors reassess how much they are willing to pay for recurring software revenue. This context helps explain why even relatively small price moves can attract attention when sentiment towards software names shifts.

- Autodesk's current valuation score is 3 out of 6, which means it screens as undervalued on half of the checks we run. Next we will look at what different valuation approaches suggest about the stock today and how a more complete framework can give you an even clearer view of its true value.

Find out why Autodesk's 1.2% return over the last year is lagging behind its peers.

Approach 1: Autodesk Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes the cash Autodesk is expected to generate in the future and discounts those projections back to today, so you can compare that value to the current share price.

Autodesk’s latest twelve month free cash flow is about US$2.36b. The DCF used here is a 2 Stage Free Cash Flow to Equity model that starts with analyst estimates and then extends them further out. For example, Simply Wall St projects free cash flow of roughly US$3.45b by the financial year ending 2029, with additional extrapolated estimates running out to 2035.

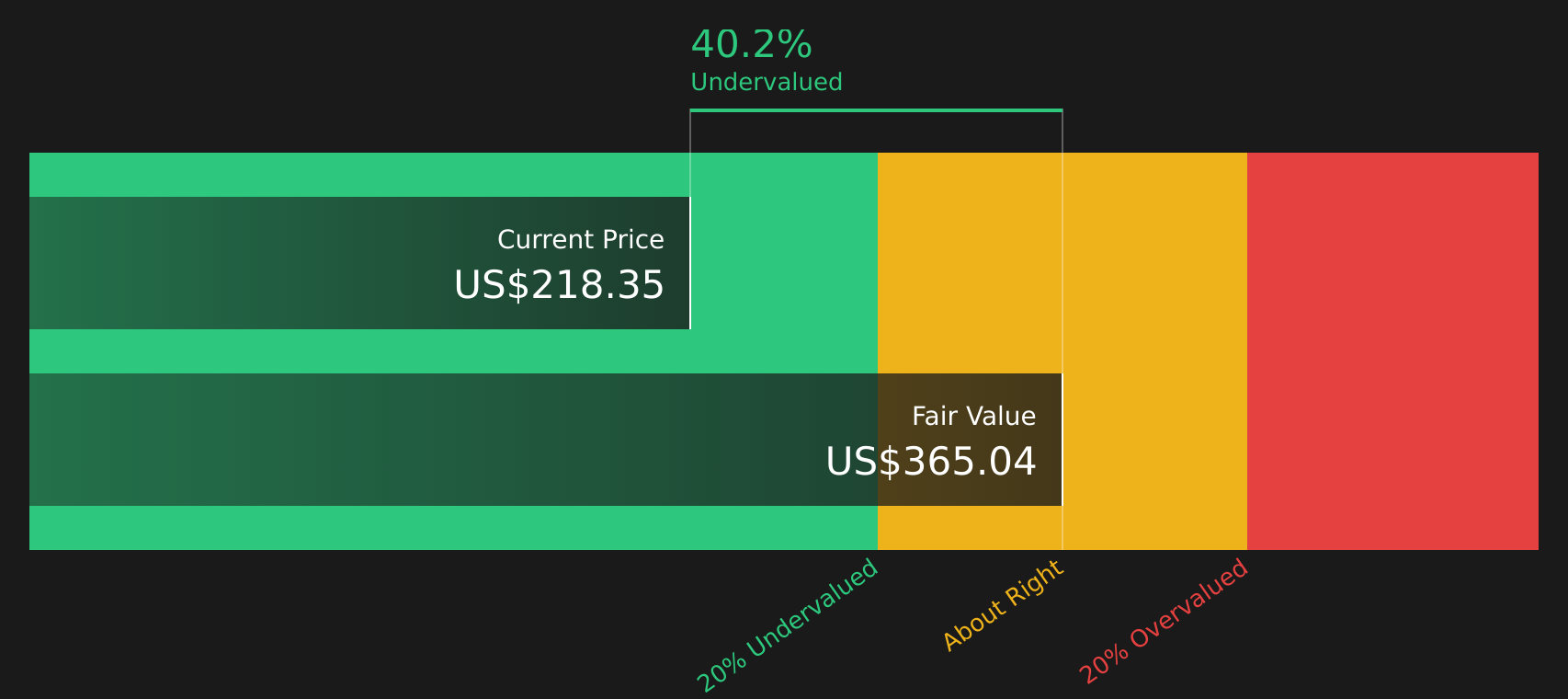

Pulling those cash flows together and discounting them back to today gives an estimated intrinsic value of about US$308.66 per share. Compared with the recent share price of US$253.85, this implies Autodesk trades at roughly a 17.8% discount to that DCF estimate, which suggests the stock is currently undervalued on this model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Autodesk is undervalued by 17.8%. Track this in your watchlist or portfolio, or discover 48 more high quality undervalued stocks.

Approach 2: Autodesk Price vs Earnings

For profitable companies like Autodesk, the P/E ratio is a useful way to relate what you pay for each share to the earnings that support it. It gives you a quick sense of how much investors are currently willing to pay for US$1 of earnings.

What counts as a “normal” P/E depends a lot on how quickly earnings are expected to grow and how risky those earnings look. Higher expected growth and perceived stability usually support a higher P/E, while slower growth or higher risk tend to justify a lower one.

Autodesk currently trades on a P/E of 47.65x. That sits above the broader Software industry average of 27.27x, but below the 56.14x average of its peer group. Simply Wall St also calculates a proprietary “Fair Ratio” for Autodesk of 34.08x. This is an estimate of what a reasonable P/E could be for the company, taking into account its earnings growth profile, industry, profit margins, market cap and key risks, rather than just comparing it to a simple industry or peer average.

Because the current P/E of 47.65x is meaningfully higher than the Fair Ratio of 34.08x, this approach points to Autodesk looking expensive on earnings.

Result: OVERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Start investing in legacies, not executives. Discover our 20 top founder-led companies.

Upgrade Your Decision Making: Choose your Autodesk Narrative

Earlier we mentioned that there is an even better way to understand valuation. On Simply Wall St's Community page you can use Narratives, where you attach your own story about Autodesk to concrete forecasts for revenue, earnings and margins. You then use that forecast to calculate a Fair Value and compare it to the current share price to help decide if Autodesk looks attractive or not. Narratives update automatically when fresh news or earnings arrive. One investor might align with a bullish Fair Value around US$413.07 per share, another might lean closer to a cautious Fair Value near US$262.20. You can quickly see which story feels closer to what you believe and how that lines up against the latest market price.

Do you think there's more to the story for Autodesk? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ADSK

Autodesk

Engages in the provision of 3D design, engineering, and entertainment technology solutions worldwide.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2552.0% undervalued

139 followersusers have followed this narrative

0 commentsusers have commented on this narrative

26 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0332.5% undervalued

11 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.528.6% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.725.6% undervalued

8 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

RC

rcb9 on DocuSign ·

Strip The Tax Benefit And Earnings Grew 36%

Fair Value:US$60.999.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RC

rcb9 on Boeing ·

The Operations Turned Profitable, The Balance Sheet Has Not

Fair Value:US$160.0145.9% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6814.9% undervalued

81 followersusers have followed this narrative

2 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28026.2% undervalued

245 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9116.1% overvalued

114 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$202.6284.3% overvalued

129 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

GR

greg_xasak on Fiserv ·

As someone who has dealt directly with them as a CTO for a credit union, I have 8 years of horror stories about doing business with them. If there was any other competitor than could deliver 80% of Fiserv services, there would be a mad rush to migrate to them. They should thank their lucky stars they are a near monopoly. this industry is so ripe for a well funded competitor. Their integration of technology is awful, their ability to fix their own implementation screwups is sadly tragic. Sometimes they just silently kill support tickets without resolution and you never find out until you do a follow up inquiry. Why, because sometimes no one you are dealing with knows how to fix it and knows no one to ask for help. They can not meet their own implementation deadlines and sometimes there is no one on a technical team dealing with you that has any banking or credit union experience. The is an industry insider phrase when you meet other Fiserv customers called being "Fiserved". It means telling others of your worst stories of dealing with them. Ask around, all CTO's have some doozies.

4

|0

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0