Advertisement

- United States

- /

- Software

- /

- NasdaqGS:ADSK

Autodesk (ADSK): Assessing Valuation Potential Following Recent Steady Share Performance

Autodesk (ADSK) stock has been relatively steady with slight movements over the past week. This has attracted attention from investors who are looking for updates on its growth story. Many are watching how its recent growth trends might influence upcoming quarters.

See our latest analysis for Autodesk.

Autodesk’s stock has posted a modest share price return year to date, and while short-term moves have been mild, its total shareholder return over the past three years sits at an impressive 42%, hinting at momentum that investors continue to watch.

If Autodesk’s steady pace has you thinking about what else is out there, take a look at fast growing stocks with high insider ownership for more potential growth stories and insider-backed opportunities.

But with Autodesk’s valuation hovering near analyst targets and growth metrics remaining solid, the key question is whether the stock still offers upside for new investors or if the market has already factored in future gains.

Most Popular Narrative: 17.7% Undervalued

At $299.39, Autodesk’s last close sits well below what the most-followed narrative considers a fair price. With a calculated fair value of $363.71 per share, the storyline points to meaningful upside potential if analysts’ growth assumptions hold true.

Accelerating adoption of cloud-based platforms, such as Autodesk Construction Cloud and Fusion 360, and ongoing rollout of subscription and SaaS models are increasing recurring revenue, improving revenue visibility, and enhancing net margin stability due to higher operating leverage and sales efficiency improvements.

Want to know what’s really powering this optimistic target? There is a specific growth engine in play, with projected profit expansion and a premium multiple that rivals industry leaders. Which bold assumptions are fueling this confidence and could change the stakes for Autodesk? Click through and discover the full calculations that justify this eye-catching price estimate.

Result: Fair Value of $363.71 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, risks such as rising competition from open-source alternatives and shifting customer preferences could challenge Autodesk's pricing power and long-term profit outlook.

Find out about the key risks to this Autodesk narrative.

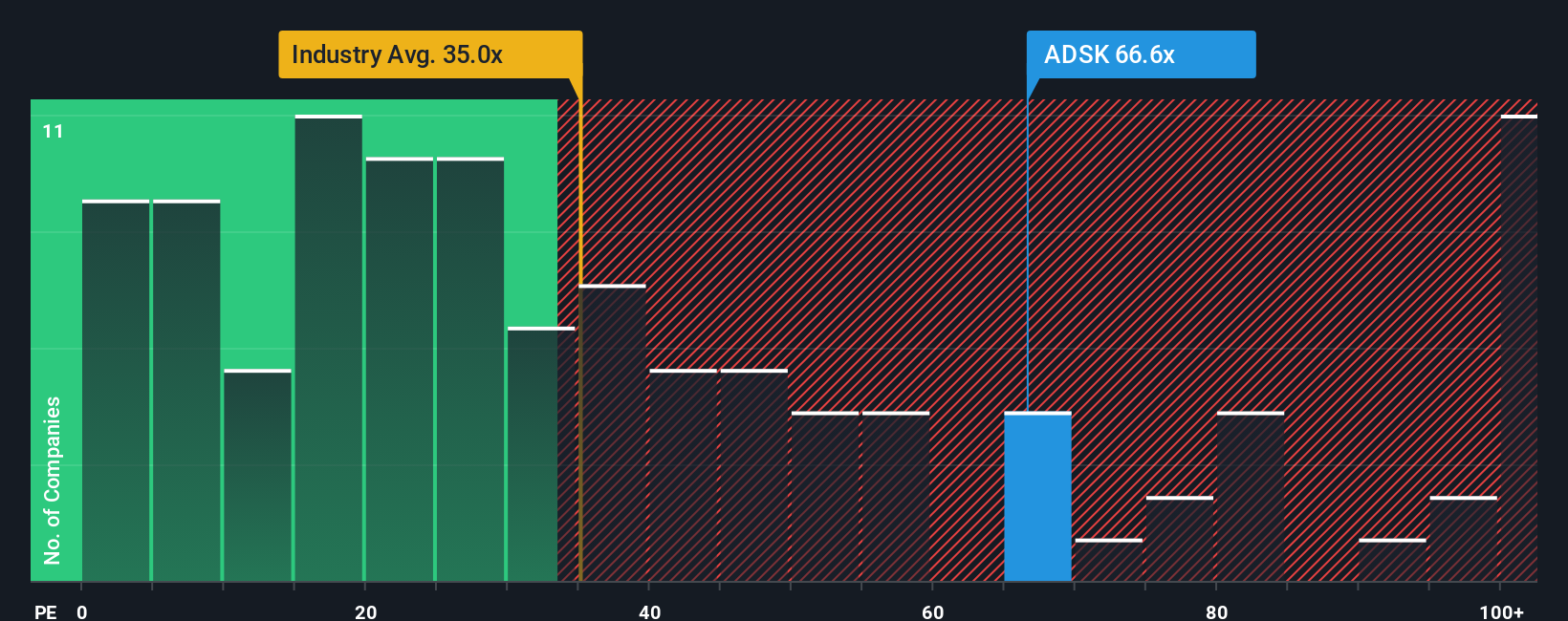

Another View: High Multiples Signal Caution

Looking at Autodesk’s price-to-earnings ratio, the stock seems expensive compared to both its industry and its peers. With a P/E of 61.1x against a US Software industry average of 31.2x and a peer average of 51.5x, it also trades far above the fair ratio of 41.8x. This premium poses valuation risk if growth expectations slip. Could the market be pricing in too much good news, or will Autodesk justify these elevated multiples?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Autodesk Narrative

If you want to challenge these views or dig further into the numbers yourself, you can craft your own version of Autodesk’s story in just a few minutes by using Do it your way.

A great starting point for your Autodesk research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Don’t settle for just one opportunity. Expand your watchlist with market themes that could boost your portfolio. Make your next move count with these proven ideas:

- Boost your income potential by targeting companies with steady yields through these 16 dividend stocks with yields > 3%, which highlights stocks delivering attractive dividends above 3%.

- Get in early on emerging tech leaders by checking out these 24 AI penny stocks and spot innovation powerhouses driving the artificial intelligence revolution forward.

- Capitalize on value with these 885 undervalued stocks based on cash flows, which spotlights quality businesses trading at compelling prices compared to their cash flow outlook.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ADSK

Autodesk

Engages in the provision of 3D design, engineering, and entertainment technology solutions worldwide.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7061.6% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17036.6% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38026.3% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7448.8% undervalued

41 followersusers have followed this narrative

0 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

IM

Imthetxarbi on Maha Capital ·

Is It worth SEK 16? Arbitrage opportunity?

Fair Value:SEK 0.681.1k% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AR

ariz_scribe on Marti Technologies ·

$MRT at Roth - Pick of the Panel

Fair Value:US$1.968.7% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CJ

cjimi on Wise Group ·

Wise: A Quality Cross-Border Payments Compounder, But Not A Bargain

Fair Value:UK£12.0232.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.7% undervalued

124 followersusers have followed this narrative

2 commentsusers have commented on this narrative

35 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9722.1% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1930.3% undervalued

46 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative