Advertisement

- United States

- /

- Software

- /

- NasdaqGS:ADBE

Adobe (ADBE) Is Up 7.6% After Unveiling AI Foundry for Custom Enterprise Generative AI Solutions Has the Bull Case Changed?

Reviewed by Sasha Jovanovic

- Earlier this week, Adobe announced the launch of Adobe AI Foundry, a new enterprise solution designed to help companies create custom generative AI models using their own intellectual property, built on the Firefly AI platform.

- This move marks an important expansion of Adobe’s AI monetization strategy, giving brands new tools to produce personalized, on-brand content at scale while protecting intellectual property.

- We’ll explore how Adobe’s entry into enterprise-grade generative AI could impact its growth outlook and overall investment narrative.

We've found 17 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Adobe Investment Narrative Recap

To remain confident as an Adobe shareholder, you need to believe the company can stay ahead in the rapidly evolving AI-powered creative software market while managing disruptions from new competitors. The recent launch of Adobe AI Foundry brings fresh potential for enterprise growth by allowing brands to build their own generative AI models on secure, proprietary data. However, increased competition from both established players and emerging AI startups continues to be the most pressing risk and may weigh on subscription growth in the near term; this launch does not materially change that risk at the moment.

Among Adobe’s recent announcements, the rollout of over 100 new AI features across Creative Cloud, including advancements in Firefly, stands out as especially relevant. These enhancements closely tie into the Foundry launch, strengthening the ecosystem that Adobe’s enterprise clients rely on for efficient content creation and brand protection. As AI features become more deeply integrated, their adoption pace remains a short-term catalyst for revenue and customer retention.

But importantly, if the AI-driven rivalry intensifies faster than expected, that could mean...

Read the full narrative on Adobe (it's free!)

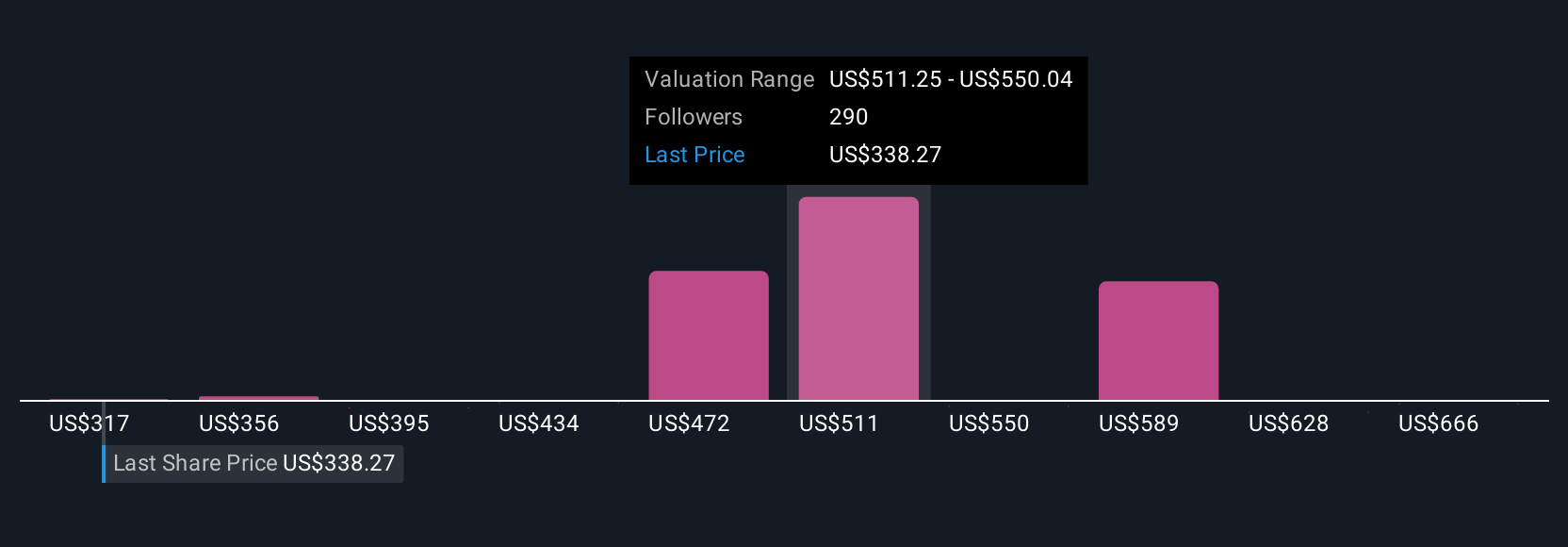

Adobe's outlook anticipates $29.3 billion in revenue and $8.7 billion in earnings by 2028. This scenario assumes a 9.0% annual revenue growth and represents an increase of $1.8 billion in earnings from the current $6.9 billion.

Uncover how Adobe's forecasts yield a $456.18 fair value, a 29% upside to its current price.

Exploring Other Perspectives

Some analysts paint a much more pessimistic picture, forecasting Adobe’s revenue to grow by just 7 percent annually and warning that heavy reliance on AI integration for user growth may not play out as planned. If you prefer to explore several viewpoints, remember both the upside and the possibility that new enterprise AI tools could shift these assumptions.

Explore 87 other fair value estimates on Adobe - why the stock might be worth as much as 70% more than the current price!

Build Your Own Adobe Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Adobe research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free Adobe research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Adobe's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 36 best rare earth metal stocks of the very few that mine this essential strategic resource.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ADBE

Adobe

Operates as a technology company worldwide.

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

4 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

Faltaren on AmpliTech Group ·

AmpliTech Group Will Triple Revenue by 2030 with O-RAN Expansion

Fair Value:US$3078.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.166.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative