- United States

- /

- Semiconductors

- /

- NasdaqGS:TER

Is It Too Late To Consider Teradyne After Its 2025 AI and Automation Rally?

Reviewed by Bailey Pemberton

- If you are wondering whether Teradyne is still worth buying after its big run, or if you might be late to the party, you are in the right place to unpack what the current share price might really be saying about value.

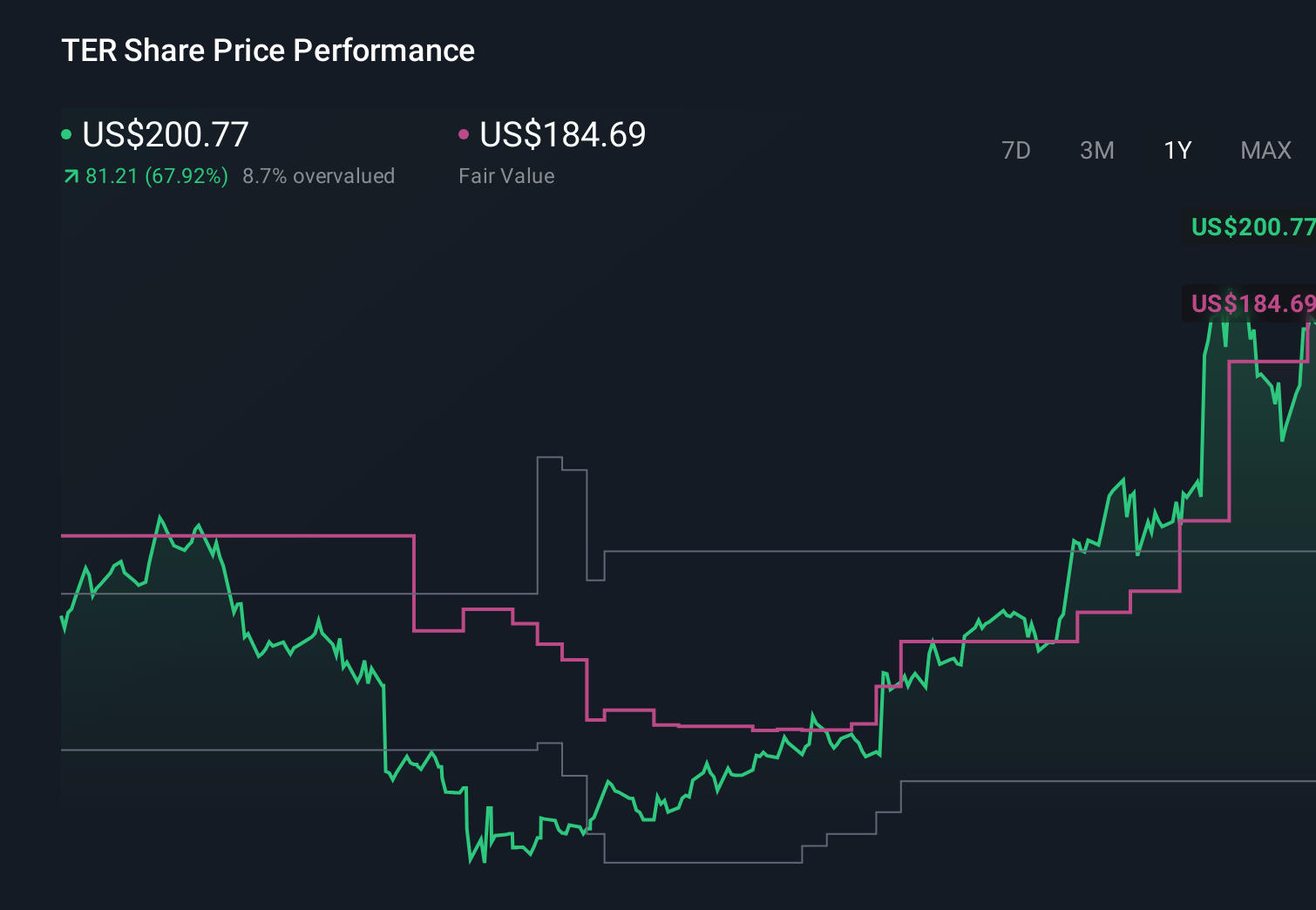

- Despite a recent 3.8% pullback over the last week, the stock is still up 13.1% over the past month, 51.9% year to date, and 50.9% over the last year. This naturally raises questions about whether expectations have run ahead of fundamentals.

- Over the past few months, investors have been reacting to Teradyne's positioning in key secular themes such as semiconductor test, industrial automation, and robotics. Sentiment has shifted as the market reassessed how central its technology could be to the next wave of chip and factory investments. At the same time, broader optimism around AI infrastructure and automation has pulled many equipment names higher, and Teradyne has been part of that narrative as traders price in a longer runway of demand.

- On our scorecard, Teradyne currently registers a valuation score of 0/6, suggesting it does not screen as undervalued on any of our standard checks. In the sections ahead we will review those traditional valuation approaches and then finish by looking at a more nuanced way to think about what the market might be missing.

Teradyne scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Teradyne Discounted Cash Flow (DCF) Analysis

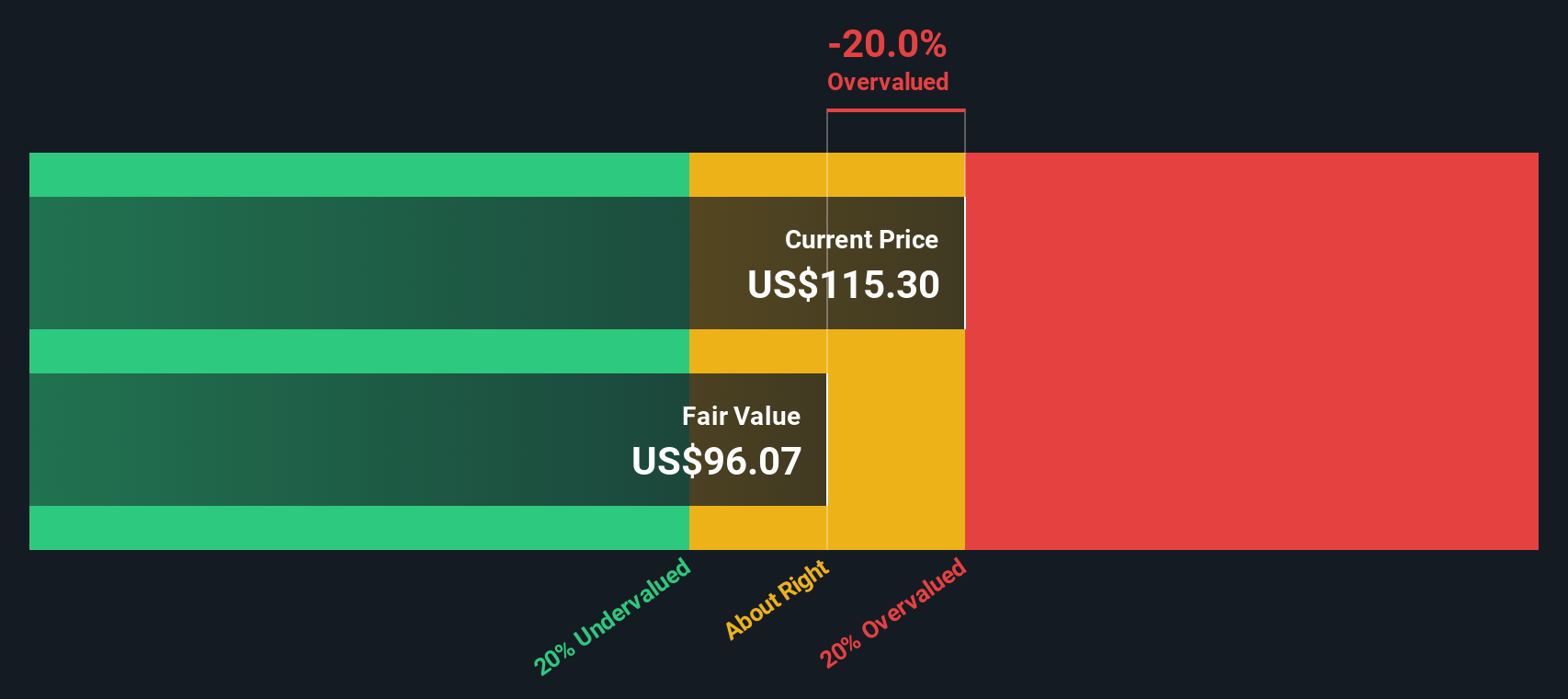

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it could generate in the future and then discounting those cash flows back to today in $ terms. For Teradyne, the 2 Stage Free Cash Flow to Equity model starts with last twelve months free cash flow of about $486 million and builds up using analyst forecasts for the next few years, then extrapolates further growth beyond that.

On this basis, Simply Wall St projects Teradyne’s free cash flow rising to around $1.76 billion by 2035, with the early years guided by analyst estimates and the later years assuming moderating growth as the business matures. When these future cash flows are discounted back to today, the model arrives at an intrinsic value of roughly $106.79 per share.

Compared with the current market price, this implies Teradyne is about 80.1% overvalued, suggesting investors are paying a substantial premium over what its projected cash generation alone would justify.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Teradyne may be overvalued by 80.1%. Discover 909 undervalued stocks or create your own screener to find better value opportunities.

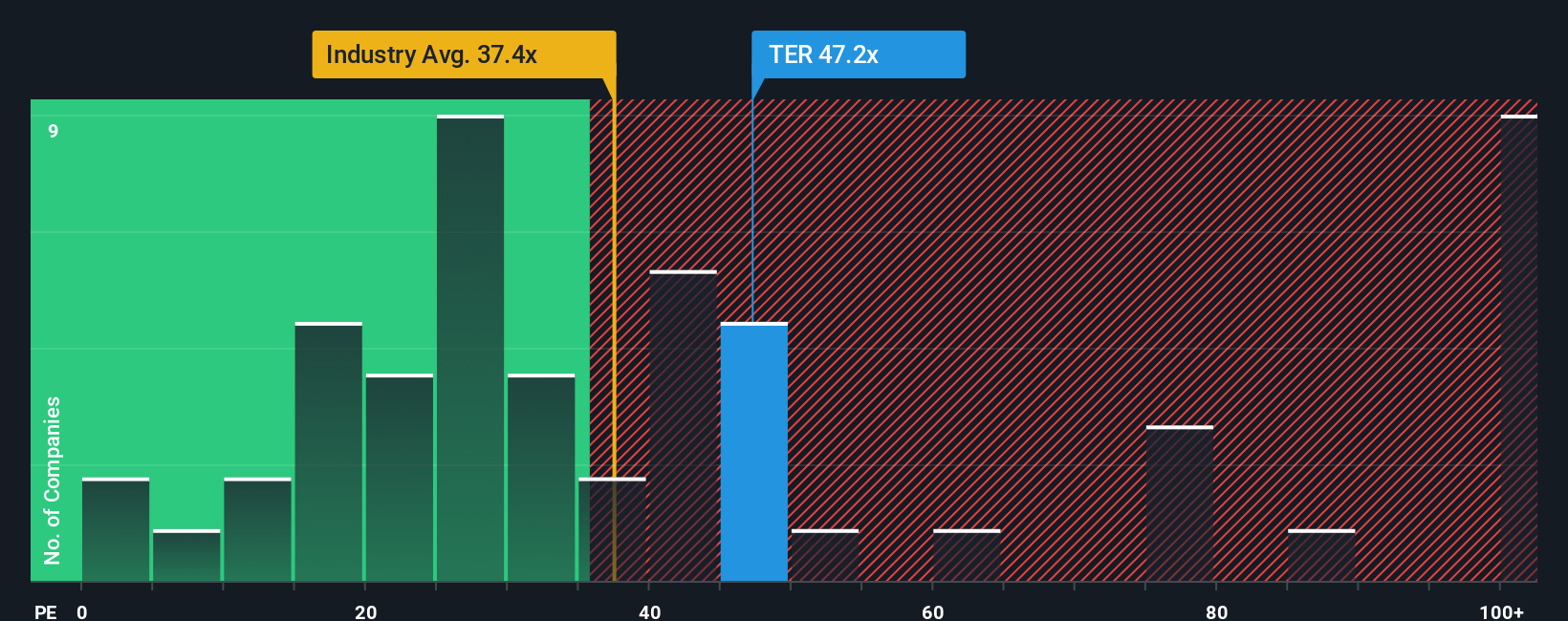

Approach 2: Teradyne Price vs Earnings

For profitable businesses like Teradyne, the price to earnings ratio is a useful yardstick because it directly links what investors pay today to the profits the company is generating. In general, faster earnings growth and lower perceived risk justify a higher multiple, while slower growth or higher uncertainty usually call for a discount.

Teradyne currently trades on about 68.0x earnings, well above the Semiconductor industry average of around 37.3x and also richer than the peer group average of roughly 34.2x. To go a step further, Simply Wall St calculates a Fair Ratio of 40.6x, which is the price to earnings multiple that would be expected for Teradyne given its specific mix of earnings growth prospects, profitability, industry positioning, size and risk profile. This tailored benchmark is more informative than a simple comparison with peers or the broad industry because it adjusts for Teradyne’s own fundamentals rather than assuming all companies deserve the same multiple.

Comparing that Fair Ratio of 40.6x with the current 68.0x suggests the stock is trading at a significant premium to what its underlying characteristics would typically support.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1457 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Teradyne Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple tool on Simply Wall St’s Community page where you connect your story about Teradyne with concrete forecasts for revenue, earnings, margins and a resulting fair value. You can then compare that fair value to today’s price to consider whether to buy, hold or sell. The platform keeps your view dynamically updated as new news and earnings arrive. For example, a bullish investor who believes AI test demand and robotics expansion can justify a fair value closer to about $192 per share and a higher growth path can choose to stay invested. A more cautious investor who focuses on execution risks and softer end markets might anchor nearer the low analyst target of about $85. Both can clearly see how their assumptions flow from business story to financial model to valuation in one intuitive framework used by millions of other investors.

Do you think there's more to the story for Teradyne? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Teradyne might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TER

Teradyne

Designs, develops, manufactures, and sells automated test systems and robotics products in the United States, Asia Pacific, Europe, the Middle East, and Africa.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)