Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGM:MRAM

Is Everspin Technologies (MRAM) Fully Valued As Russell Index Inclusion Draws More Attention?

Everspin Technologies (MRAM) has been added to multiple Russell indexes, including the Russell 3000 and Russell 2000. This change can influence how index funds and institutional investors treat the stock.

See our latest analysis for Everspin Technologies.

The Russell index additions come after a sharp run in Everspin Technologies’ share price, with a 90 day share price return of 110.74% and a year to date share price return of 95.03%. Its 1 year total shareholder return of 191.96% contrasts with a 30 day share price pullback of 17.08%, which suggests momentum has cooled in the very short term even as the longer term story remains strong.

If you are looking beyond Everspin Technologies for other potential opportunities in related areas of the market, it can be useful to see what is happening across 52 AI infrastructure stocks

Everspin Technologies now trades around $19.62 after a sharp run and some short term cooling, so the key issue is whether recent index-driven enthusiasm has already priced in most of the upside, or if valuation still leaves meaningful room ahead.

Most Popular Narrative: 9% Overvalued

The most followed narrative on Everspin Technologies compares a fair value of $18 to the last close of $19.62, framing the recent run as pricing in more than the modeled outcome under a detailed cash flow and growth scenario that uses an 11.1% discount rate.

Broader adoption of MRAM for data center and industrial automation, driven by increasing demand for persistent, low-latency memory in AI, IoT, and edge computing, is supporting sequential revenue growth and expanding Everspin's addressable markets, which can lead to sustained top-line revenue growth.

Want to see what kind of revenue curve and margin lift would need to sit behind that fair value, and how rich a profit multiple this narrative is willing to underwrite on those future earnings? The full breakdown walks through compounded top line growth, margin expansion and the profit base Everspin Technologies is modeled to reach before that valuation math starts to line up.

Result: Fair Value of $18 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this Everspin Technologies narrative could be tested if margin pressures persist or if key government related projects and contracts do not renew as expected.

Find out about the key risks to this Everspin Technologies narrative.

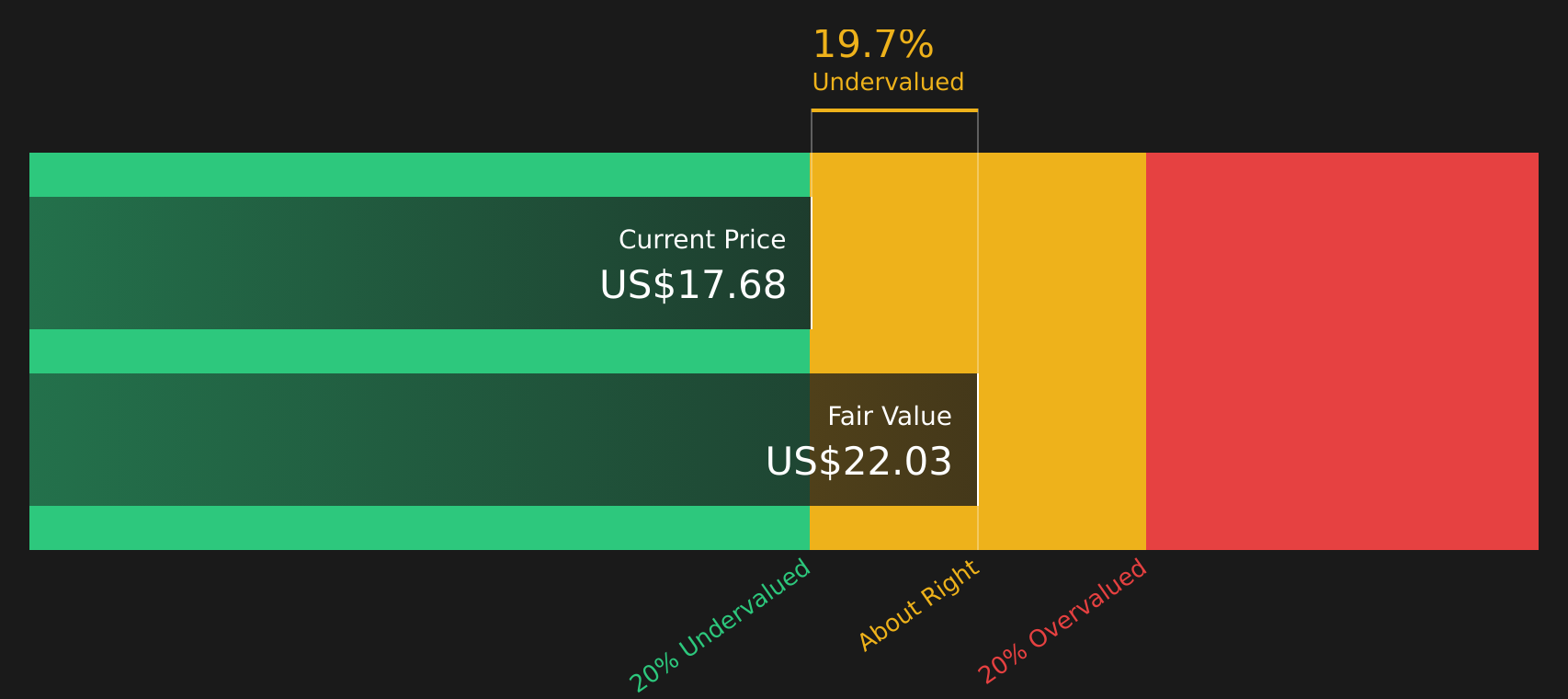

Another View: SWS DCF Fair Value Check

The most followed Everspin Technologies narrative leans on analyst targets and earnings projections, but the SWS DCF model points in a different direction. At a share price of $19.62, it indicates Everspin Technologies is trading about 11% below an estimated fair value of $22.03. This frames current levels as a discount rather than a premium and raises the question of which story investors should put more weight on.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Everspin Technologies for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such mixed sentiment around Everspin Technologies, it helps to move quickly, review the underlying data and decide where you stand in this debate. To see how the potential upside stacks up against the issues investors are watching, take a closer look at the 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond Everspin Technologies?

If Everspin Technologies has caught your attention, do not stop here. Broaden your watchlist with other focused stock ideas that might suit your style and risk tolerance.

- Target potential value opportunities by scanning companies that currently look attractively priced with solid fundamentals using the 41 high quality undervalued stocks.

- Prioritize resilience by checking companies that feature stronger balance sheets and steadier financial profiles through the solid balance sheet and fundamentals stocks screener (47 results).

- Hunt for future standouts by reviewing lesser known companies with strong underlying metrics via the screener containing 18 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Everspin Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:MRAM

Everspin Technologies

Manufactures and sells magnetoresistive random access memory (MRAM) technologies in the United States, Japan, Hong Kong, Germany, Singapore, Canada, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2540.2% undervalued

94 followersusers have followed this narrative

0 commentsusers have commented on this narrative

23 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.828.5% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23059.3% overvalued

37 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32040.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Revival Gold ·

7,000% US Based Idaho & Utah Gold Miner Play, Beartrack + Mercur: $1.2B+ NAV Leverage with Strong Management

Fair Value:CA$12.7194.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

NO

NordicWolf on Carlsberg ·

Defensive Beverage Compounder With Britvic Upside

Fair Value:DKK 870.327.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

DaneDruss on Cloudflare ·

Q-Day: Quantum Hype vs Quantum-Safe Infrastructure

Fair Value:US$167.4547.8% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.9% undervalued

84 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9631.8% undervalued

64 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5453.8% undervalued

58 followersusers have followed this narrative

1 commentusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

MW

mwod31 on Greatland Resources ·

A great comment, WSB have not done the research imo. I intend to buy more shares in 2026.

0

|0