Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:AMD

Here is why Advanced Micro Devices' (NASDAQ:AMD) Earnings and Free Cash Flows Don't Match

Advanced Micro Devices, Inc. (NASDAQ:AMD) recently released a strong earnings report, and the market responded by raising the share price. However, we think that shareholders should be aware of some other factors beyond the profit numbers.

The company exhibits a large and scalable revenue growth, and with the high demand for their products this trend can be sustainable.

AMD will also benefit from the new U.S. government bill that will pump some US$52b into semiconductor manufacturers such as AMD, Intel (NASDAQ:INTC), NVIDIA (NASDAQ:NVDA). The goal of this bill, that recently passed the senate, is to lessen the reliance of the U.S. on Chinese manufacturers.

AMD also keeps innovating and improving their product offerings. It recently released a new AMD Radeon™ PRO W6000X series GPUs for Mac Pro.

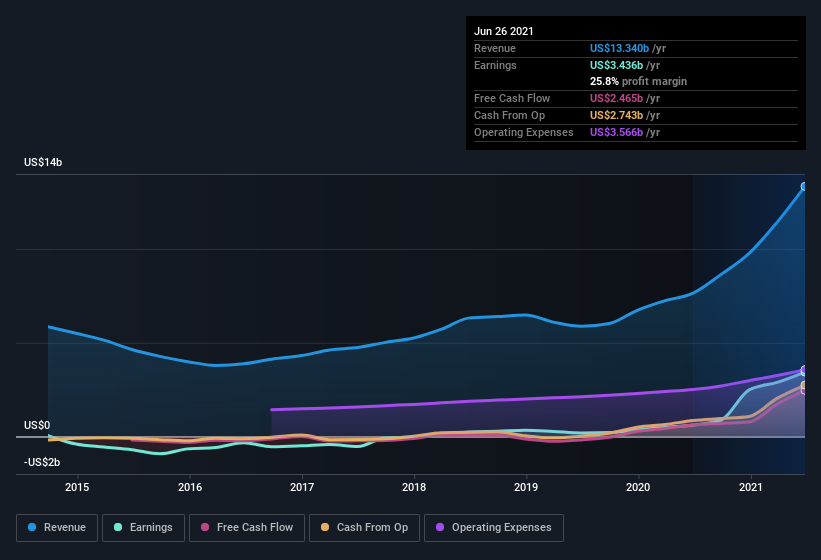

With this in mind, it is not so surprising to see how, this can continue in future quarters. The chart below, shows us key aspects of AMD's fundamental performance.

See our latest analysis for Advanced Micro Devices

We can see that besides growth, the company is doing a great job at keeping operating expenses leveled and profits increasing.

There seems to be a difference between the net income and free cash flows, which is what we will analyze in more detail.

Examining Cashflow Against Advanced Micro Devices' Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period.

To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period.

You could think of the accrual ratio from cashflow as the portion of net income that did not convert into free cash flows.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest.

Some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

Advanced Micro Devices has an accrual ratio of 0.34 for the year to June 2021.

Unfortunately, that means its free cash flow was a lot less than its statutory profit. It produced free cash flow of US$2.5b during the period, falling well short of its reported profit of US$3.44b.

We note, however, that Advanced Micro Devices grew its free cash flow over the last year. However, as we will discuss below, we can see that the company's accrual ratio has been impacted by its tax situation. This would certainly have contributed to the weak cash conversion.

One positive for Advanced Micro Devices shareholders is that it's accrual ratio was significantly better last year, providing reason to believe that it may return to stronger cash conversion in the future. As a result, some shareholders may be looking for stronger cash conversion in the current year.

An Unusual Tax Situation

Moving on from the accrual ratio, we note that Advanced Micro Devices profited from a tax benefit which contributed US$1.0b to profit.

Of course, at first glance, it's great to receive a tax benefit. However, our data indicates that tax benefits can temporarily boost statutory profit in the year it is booked, but subsequently profit may fall back. In the likely event the tax benefit is not repeated, we'd expect to see its statutory profit levels drop, at least in the absence of strong growth. So while we think it's great to receive a tax benefit, it does tend to imply an increased risk that the statutory profit overstates the sustainable earnings power of the business.

Our Take On Advanced Micro Devices' Profit Performance

This year, Advanced Micro Devices couldn't match its profit with cashflow, primarily because of the US$1b in tax benefit. Investors should be mindful when the company reports earnings, because sometimes they partly result from one time events.

On top of that, the unsustainable nature of tax benefits mean that there's a chance profit may be lower next year, certainly in the absence of strong growth.

AMD is clearly in a great position to grow, as its products are loved by clients and backed by the U.S. Government and their top line is looking great. That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Considering all this, we'd argue Advanced Micro Devices' profits probably give an overly generous impression of its sustainable level of profitability.

In this article, we've looked at a number of factors that can impair the utility of profit numbers, and we've come away cautious. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NasdaqGS:AMD

Advanced Micro Devices

Operates as a semiconductor company internationally.

Exceptional growth potential with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1947.9% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7719.6% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19017.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

BL

BlackGoat on Micron Technology ·

Micron's New Supercycle: Riding the High-Bandwidth Memory Wave

Fair Value:US$1.48k41.5% undervalued

90 followersusers have followed this narrative

8 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on COVER ·

Significant headwinds will temper expectations for FY2027

Fair Value:JP¥1.91k15.0% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

AN

AnimalDoctorKwon on Teladoc Health ·

Pandemic Relic or Cash-Flow Bargain?

Fair Value:US$1535.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75027.0% undervalued

96 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5457.4% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6512.6% undervalued

65 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

2

|0

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0