- United States

- /

- Semiconductors

- /

- NasdaqGM:ACMR

Is ACM Research Still Attractive After Its 149.4% Surge in 2025?

Reviewed by Bailey Pemberton

- If you are wondering whether ACM Research is still a smart buy after its huge run, or if you might be late to the party, this breakdown will help you decide with a clear, valuation-first lens.

- The stock has surged recently, climbing 10.6% over the last week, 23.2% over the past month, and a striking 149.4% year to date. Moves like this often signal that market expectations and perceived risk are shifting fast.

- Those moves have come as investors stay focused on ACM Research's role in supplying cleaning tools to semiconductor manufacturers, a part of the supply chain that can benefit when chipmakers ramp up advanced node capacity and capital spending. At the same time, ongoing attention on US China tech tensions keeps sentiment volatile, as the market weighs both growth opportunity and geopolitical risk.

- Right now, ACM Research scores a 3/6 valuation check, suggesting some upside but also pockets where the price already bakes in optimism. Next, we will walk through the key valuation approaches investors usually rely on, before finishing with a more complete way to think about what the stock is really worth.

Approach 1: ACM Research Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business is worth by projecting its future cash flows and then discounting them back to today in $ terms, to reflect risk and the time value of money.

For ACM Research, the model used is a 2 Stage Free Cash Flow to Equity approach. The company currently generates negative free cash flow of about $66.2 million, but analysts and extrapolated estimates point to improving cash generation, with projected free cash flow reaching roughly $239.8 million by 2035. These projections combine near term analyst estimates with longer term growth assumptions from Simply Wall St, stepping up from tens of millions today toward mid hundreds of millions over the coming decade.

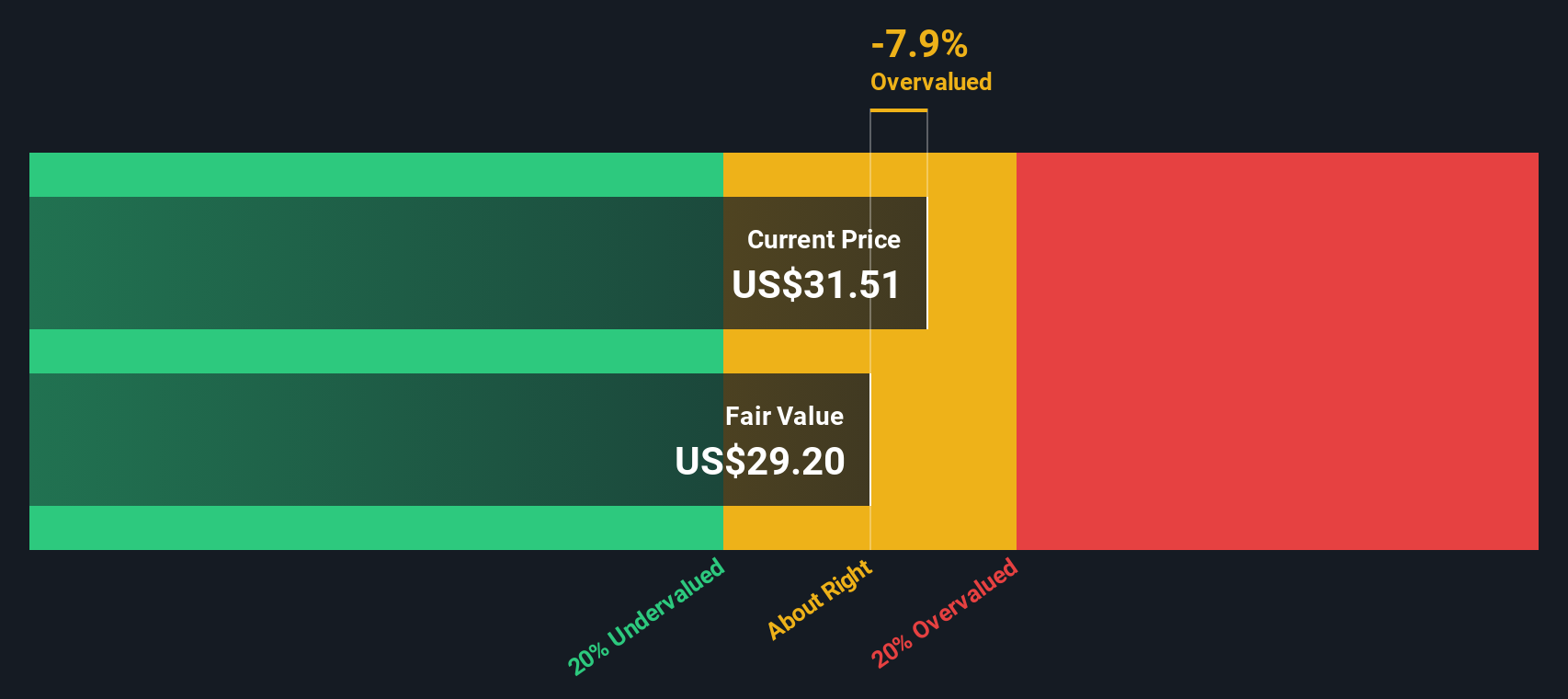

When all those future cash flows are discounted back to today, the DCF model arrives at an intrinsic value of about $30.14 per share. Based on the implied DCF discount, this suggests the stock is roughly 28.8% overvalued at its current trading price.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests ACM Research may be overvalued by 28.8%. Discover 908 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: ACM Research Price vs Earnings

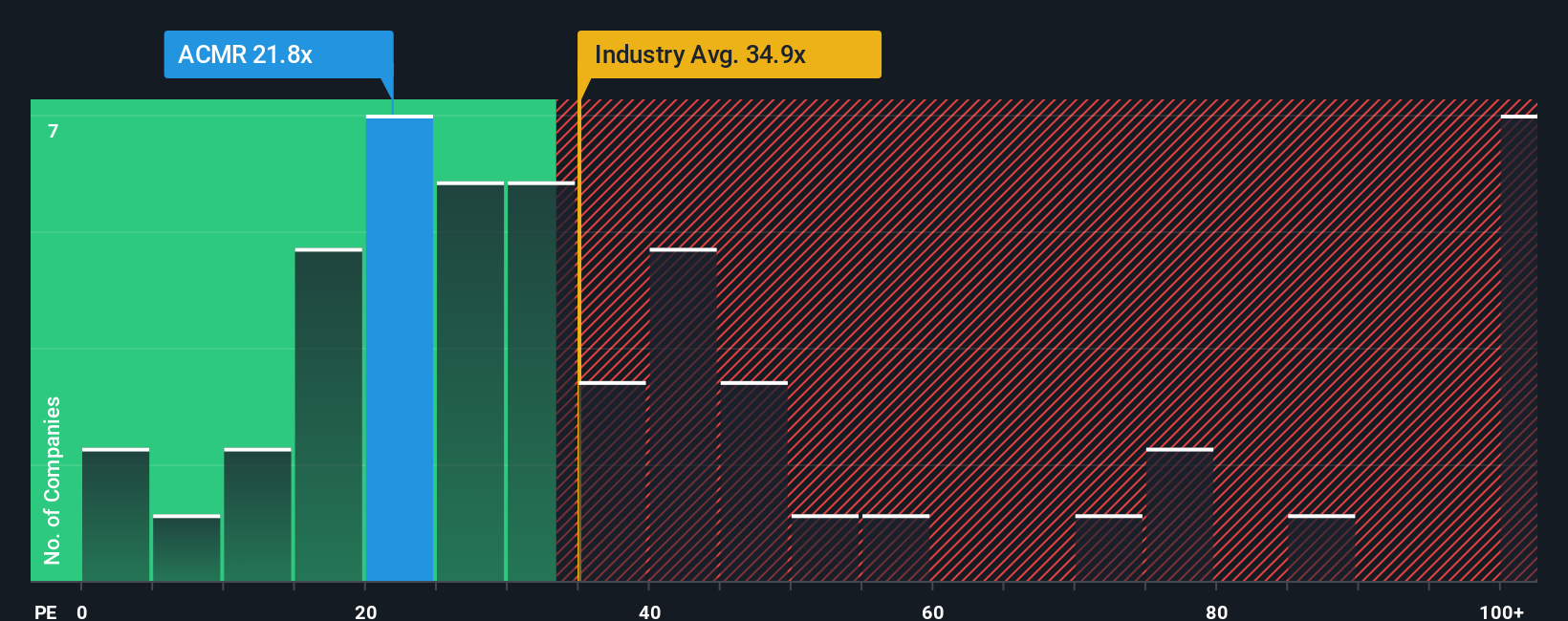

For a profitable business like ACM Research, the price to earnings, or PE, ratio is a practical way to gauge whether investors are paying a reasonable price for each dollar of current earnings. It distills expectations about future growth and risk into a single number that is easy to compare across companies.

In general, faster growing and more predictable businesses deserve a higher, or more expensive, PE, while slower, riskier names typically trade on a lower multiple. ACM Research currently trades on a PE of about 21.5x. That sits well below both the broader Semiconductor industry average of roughly 37.0x and the peer group average of around 44.9x. This suggests the market is applying a noticeable discount to ACM’s earnings.

Simply Wall St addresses the limits of simple comparisons with a proprietary Fair Ratio. This is the PE you might expect once you factor in ACM’s specific earnings growth outlook, profit margins, industry positioning, market cap and risk profile. For ACM Research, this Fair Ratio is estimated at about 33.3x, materially higher than the current 21.5x. That gap points to investors underpricing the company’s fundamentals rather than overpaying for them.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1445 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your ACM Research Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which let you attach a clear story about ACM Research’s future revenue, earnings and margins to the numbers you see on screen, link that story to a financial forecast and resulting fair value, and then compare that fair value to today’s share price to help decide whether the stock looks like a buy, hold or sell.

On Simply Wall St’s Community page, where millions of investors share their views, Narratives make this process accessible by turning your assumptions into a live model that automatically updates when new information such as earnings, guidance or major news hits the market. This way your fair value view is not static or out of date.

For example, one ACM Research Narrative might lean into strong China demand, new tools and resilient AI driven orders to justify a higher long term revenue growth rate, margin expansion and a fair value closer to the bullish 40.1 dollars target. Another, more cautious Narrative could focus on export controls, margin pressure and slower global adoption to support a fair value nearer the bearish 30.0 dollars target. This gives you a transparent way to see where you sit between those perspectives and then decide how you want to act.

Do you think there's more to the story for ACM Research? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:ACMR

ACM Research

Develops, manufactures, and sells capital equipment worldwide.

Proven track record with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion