Advertisement

- United States

- /

- Semiconductors

- /

- NasdaqGS:ACLS

Assessing Axcelis Technologies (ACLS) Valuation After Recent Share Price Momentum And Mixed Earnings Outlook

Axcelis Technologies overview and recent performance context

Axcelis Technologies (ACLS) has attracted attention after a period of mixed financial trends, with annual revenue growth of 2.99% and a 13.63% decline in net income, prompting investors to reassess the current share price of $95.72.

See our latest analysis for Axcelis Technologies.

Recent trading has been positive, with a 1 month share price return of 11.81% and a 90 day share price return of 14.27%. The 1 year total shareholder return of 37.41% sits against a slightly negative 3 year total shareholder return and a strong 5 year record of 145.50%. This suggests momentum has picked up again after a mixed medium term.

If Axcelis has you looking closer at chip makers, this could be a good moment to scan other semiconductors and related names through high growth tech and AI stocks.

With Axcelis trading at $95.72, close to its analyst price target of $93.50 and with an intrinsic discount figure that is slightly negative, investors may question whether there is meaningful upside remaining or whether the market is already fully reflecting expectations for future growth.

Most Popular Narrative: 2% Overvalued

At a last close of $95.72 versus a narrative fair value of $93.50, the story here hinges on how future margins and earnings are expected to reset.

Analysts expect earnings to reach $66.7 million (and earnings per share of $4.29) by about August 2028, down from $158.5 million today. The analysts are largely in agreement about this estimate.

Curious why a lower earnings path still lines up with a higher future earnings multiple and a positive price target gap? The core assumptions sit in the revenue glide path, margin reset, and the premium P/E investors are expected to accept. The tension between shrinking profits and a richer valuation multiple is what shapes this fair value number.

Result: Fair Value of $93.50 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, heavy China exposure and reliance on mature node demand mean that any shift in export controls or customer spending could quickly challenge this optimistic setup.

Find out about the key risks to this Axcelis Technologies narrative.

Another View: Earnings Multiple Sends a Different Signal

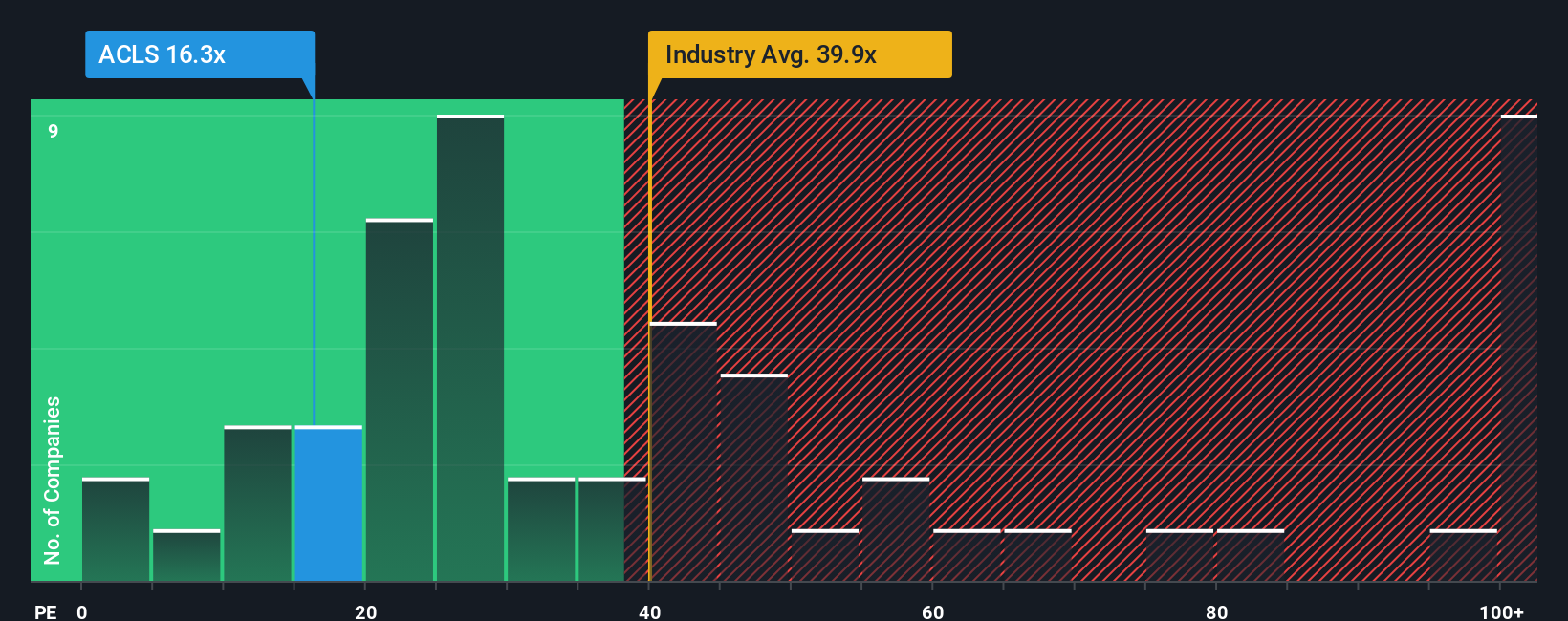

While the fair value narrative suggests Axcelis Technologies is about 2% overvalued, the current P/E of 21.6x tells a different story. It is far below the US Semiconductor industry average of 42x and the peer average of 56.1x, yet sits above the fair ratio of 15.7x.

In practical terms, that mix points to a share price that is cheaper than many direct comparisons but richer than what our fair ratio suggests the market could eventually lean toward. Is this a reasonable premium for Axcelis's position in ion implantation, or a valuation risk you want to be paid more for taking?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Axcelis Technologies Narrative

If you see the data differently or want to stress test these assumptions yourself, you can build a full Axcelis view in just a few minutes. Do it your way

A great starting point for your Axcelis Technologies research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Ready for more investment ideas?

If Axcelis has sharpened your focus, do not stop here. Broaden your watchlist now so you are not the one hearing about the best ideas later.

- Spot potential value plays early by tracking these 880 undervalued stocks based on cash flows that might offer more for every dollar of future cash flow.

- Ride the AI build out by scanning these 26 AI penny stocks positioned around data centers, chips, and intelligent software.

- Add higher income potential to your shortlist by checking out these 12 dividend stocks with yields > 3% that already clear a 3% yield hurdle.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ACLS

Axcelis Technologies

Designs, manufactures, and services ion implantation and other processing equipment used in the fabrication of semiconductor chips in the United States, Europe, and the Asia Pacific.

Flawless balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

34 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

HU

Hunter_Z on Lagenda Properties Berhad ·

Lagenda Continues To Offer Earnings Visibility Backed By Strong Sales Pipeline

Fair Value:RM 2.0330.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AntonioS on CAR Group ·

CAR Group. A wonderful compounding franchise at a fair-not-cheap price.

Fair Value:AU$3223.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GA

GaryB on Palantir Technologies ·

Palantir hits 52 week low.

Fair Value:US$274.861.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative