Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:W

Wayfair (W) Is Up 5.5% After Q3 Profit Surprise and Upbeat Holiday Sales Outlook – What’s Changed

Simply Wall St

Reviewed by Sasha Jovanovic

- Wayfair reported a significant turnaround in its third-quarter 2025 results, posting non-GAAP earnings of US$0.70 per share, a GAAP operating profit of US$38 million, and announced expectations for mid-single digit revenue growth in the fourth quarter despite exiting the German market.

- This improved financial performance coincided with strong Black Friday projections for e-commerce spending in the US, positioning Wayfair to benefit from substantial consumer demand, particularly as it launches deep discounts across its extensive online furniture selection.

- We'll now explore how Wayfair's better-than-expected earnings and positive holiday outlook influence its investment narrative.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

Wayfair Investment Narrative Recap

For Wayfair, the core investment thesis centers on its ambition to grow share within the large but competitive online furniture and home categories, leveraging efficiency initiatives, technology, and customer experience enhancements. The recent earnings surprise and positive holiday sales outlook provide a boost to the main near-term catalyst, robust seasonal demand, though they do not materially reduce the most significant current risk: the company's exposure to macroeconomic factors like interest rates and housing activity, which continue to weigh on the home goods sector.

Among Wayfair’s latest announcements, the new smaller-format store in Columbus, Ohio, stands out as especially relevant. This step aligns with efforts to increase customer touchpoints and improve brand engagement, reinforcing the company’s catalyst of expanding its physical retail presence to complement online sales momentum during peak periods.

Yet, despite holiday tailwinds, investors should not overlook how sensitivity to housing trends may impact growth in times when...

Read the full narrative on Wayfair (it's free!)

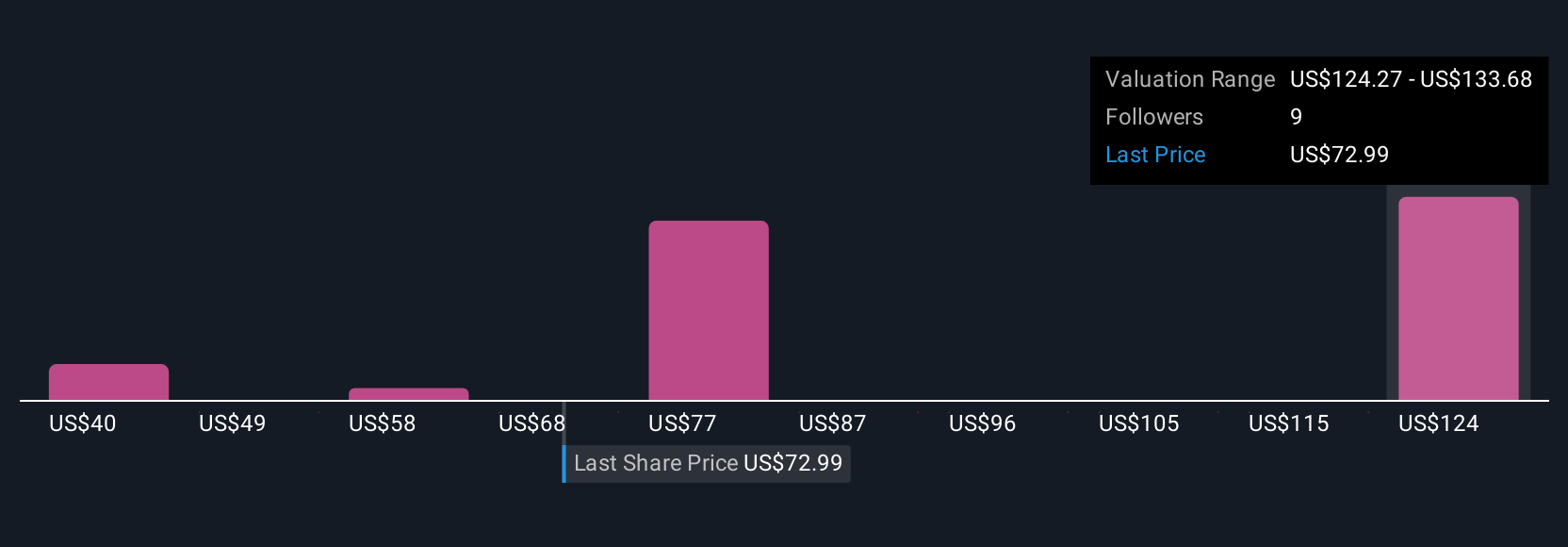

Wayfair's narrative projects $13.9 billion in revenue and $124.7 million in earnings by 2028. This requires 4.9% yearly revenue growth and a $424.7 million increase in earnings from the current -$300.0 million.

Uncover how Wayfair's forecasts yield a $114.00 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Fair value estimates from five Simply Wall St Community members for Wayfair range from US$39.54 to US$200.94, underlining high variance in sentiment. With seasonal demand surging but macro influences still in play, consider how much these perspectives can differ depending on the economic backdrop.

Explore 5 other fair value estimates on Wayfair - why the stock might be worth as much as 81% more than the current price!

Build Your Own Wayfair Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Wayfair research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Wayfair research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Wayfair's overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Wayfair might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:W

Wayfair

Engages in the e-commerce business in the United States and internationally.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

934 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative