Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:SIG

Signet Jewelers (SIG) Q3: Margin Rebound Lifts EPS, Tests Skeptical Valuation Narratives

Simply Wall St

Reviewed by Simply Wall St

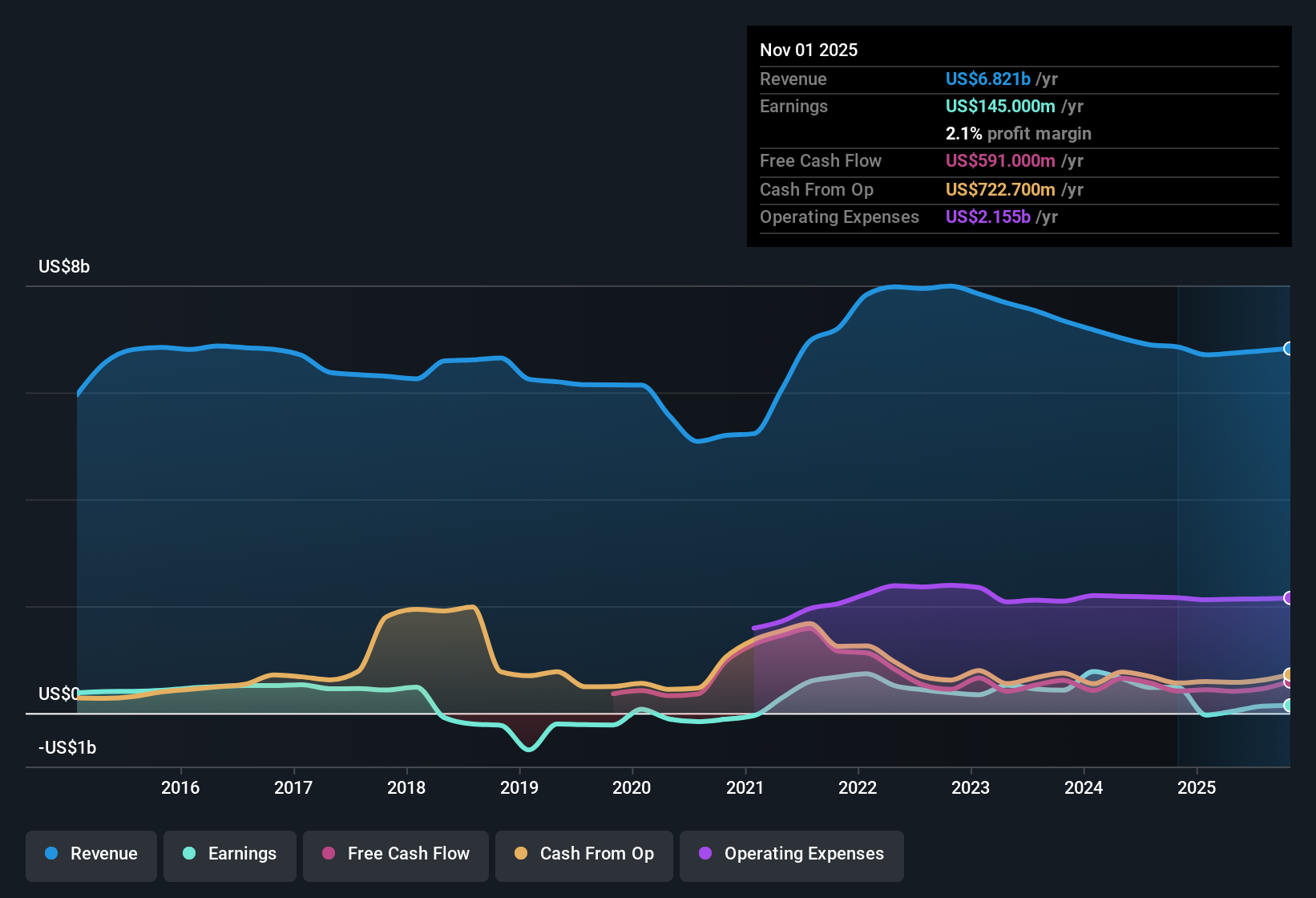

Signet Jewelers (SIG) has just posted Q3 2026 results with revenue of $1.4 billion and basic EPS of $0.49, setting the stage for investors to reassess the trajectory after a choppy first half. The company has seen quarterly revenue move from $1.49 billion in Q2 2025 to $1.35 billion in Q3 2025 and then to $1.39 billion in Q3 2026, while basic EPS has swung from a loss of $2.28 in Q2 2025 to $0.12 in Q3 2025 and $0.49 in the latest quarter. This puts the focus firmly on how sustainable the margin recovery really is.

See our full analysis for Signet Jewelers.With the latest numbers on the table, the next step is to line them up against the dominant market narratives to see which stories about Signet’s growth, earnings power, and margins actually hold up, and which ones start to look stretched.

See what the community is saying about Signet Jewelers

Margins Stabilize With $145 Million Trailing Profit

- Over the last 12 months, Signet generated $145 million of net income on $6.8 billion of revenue, which works out to a 2.1% net margin compared with 7% in the prior year.

- Consensus narrative highlights that gross margin and profit stability should benefit from lab grown diamonds and better inventory management, yet the drop in net margin to 2.1% shows that rising costs and structural demand pressures are still weighing on the bottom line.

- The trailing net margin of 2.1% contrasts with analysts expecting margins to rise toward 8.8% over the next three years. This means the story depends on a meaningful profitability lift from here.

- The $304.1 million one off loss in the last 12 months undercuts the idea of a smooth margin trajectory, even if product mix and services are helping at the gross margin level.

Earnings Growth Forecasted At 36% Per Year

- Analysts expect earnings to grow about 36.2% per year, taking profit from $130.4 million today to a projected $612.3 million by around 2028, even though revenue is only forecast to grow roughly 1.3% per year.

- Consensus narrative leans on younger consumers, lab grown diamond penetration at 14%, and higher average unit retail as key growth drivers, but the modest 1.3% revenue growth outlook and flat to slightly positive jewelry unit trends show that much of the forecasted earnings ramp hinges on mix, pricing, and margin expansion rather than strong volume growth.

- Forecast margins rising from roughly 1.9 to 8.8% over three years would have to offset the expected 1.0 to 1.3% annual revenue decline or low growth. This leaves little room for execution missteps.

- Expected share count shrinking by about 7% per year also contributes to the EPS growth story, so part of that 36.2% per year earnings growth is financial engineering rather than underlying demand acceleration.

Premium P/E Versus Peers Despite One Off Loss

- At a share price of $89.19, Signet trades on a trailing P/E of 25.2 times compared with a peer average of 14.4 times and a US Specialty Retail industry average of 18.1 times, even though net margin over the last year was only 2.1% after absorbing a $304.1 million one off loss.

- Critics highlight that this richer multiple, combined with structurally challenged bridal units and higher tariffs on imports from India, could be hard to sustain if the expected margin recovery stalls, yet the stock also sits about 37.8% below a DCF fair value of roughly $143.36, which keeps valuation arguments in play on both sides.

- Bears focus on the elevated 25.2 times P/E versus peers and industry, arguing that any disappointment in the 36.2% earnings growth outlook could hit the multiple hard from here.

- Supporters point out that the DCF fair value of about $143.36 and an analyst target around $111.71 are both above the current $89.19 price, so part of the market may be pricing in the one off loss and low trailing margin as temporary.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Signet Jewelers on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Spot patterns in the numbers that others might be missing, capture that angle in your own narrative in just a few minutes, and Do it your way.

A great starting point for your Signet Jewelers research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Explore Alternatives

Signet’s low trailing margins, reliance on aggressive earnings forecasts, and premium valuation versus peers leave little room for error if growth or profitability disappoints.

If you feel that setup looks fragile, you may want to shift your focus toward these 926 undervalued stocks based on cash flows to look for companies where current prices already bake in caution and potential upside appears more skewed in your favor.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SIG

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

31 followersusers have followed this narrative

6 commentsusers have commented on this narrative

7 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1919.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5190.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Applied Digital ·

Staggered by dilution; positions for growth

Fair Value:US$35.4520.9% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.5% undervalued

949 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.1% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative