- United States

- /

- Specialty Stores

- /

- OTCPK:PRTY.Q

Earnings growth of 0.1% over 5 years hasn't been enough to translate into positive returns for Party City Holdco (NYSE:PRTY) shareholders

Some stocks are best avoided. We don't wish catastrophic capital loss on anyone. For example, we sympathize with anyone who was caught holding Party City Holdco Inc. (NYSE:PRTY) during the five years that saw its share price drop a whopping 89%. And it's not just long term holders hurting, because the stock is down 82% in the last year. Even worse, it's down 48% in about a month, which isn't fun at all. We really hope anyone holding through that price crash has a diversified portfolio. Even when you lose money, you don't have to lose the lesson.

With the stock having lost 19% in the past week, it's worth taking a look at business performance and seeing if there's any red flags.

Check out the opportunities and risks within the US Specialty Retail industry.

While markets are a powerful pricing mechanism, share prices reflect investor sentiment, not just underlying business performance. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

While the share price declined over five years, Party City Holdco actually managed to increase EPS by an average of 0.7% per year. Given the share price reaction, one might suspect that EPS is not a good guide to the business performance during the period (perhaps due to a one-off loss or gain). Alternatively, growth expectations may have been unreasonable in the past.

By glancing at these numbers, we'd posit that the the market had expectations of much higher growth, five years ago. Having said that, we might get a better idea of what's going on with the stock by looking at other metrics.

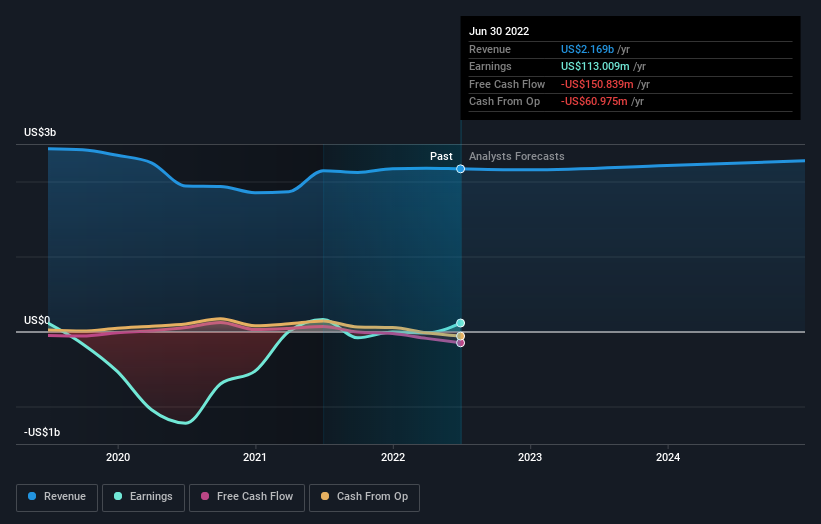

Arguably, the revenue drop of 3.7% a year for half a decade suggests that the company can't grow in the long term. That could explain the weak share price.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

We consider it positive that insiders have made significant purchases in the last year. Even so, future earnings will be far more important to whether current shareholders make money. If you are thinking of buying or selling Party City Holdco stock, you should check out this free report showing analyst profit forecasts.

A Different Perspective

While the broader market lost about 44% in the twelve months, Party City Holdco shareholders did even worse, losing 82%. However, it could simply be that the share price has been impacted by broader market jitters. It might be worth keeping an eye on the fundamentals, in case there's a good opportunity. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 14% per year over five years. Generally speaking long term share price weakness can be a bad sign, though contrarian investors might want to research the stock in hope of a turnaround. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Even so, be aware that Party City Holdco is showing 2 warning signs in our investment analysis , you should know about...

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OTCPK:PRTY.Q

Party City Holdco

Party City Holdco Inc. designs, manufactures, sources, and distributes party goods worldwide.

Slightly overvalued with weak fundamentals.

Market Insights

Community Narratives