Advertisement

Kohl’s Shares Surge 56% Amid M&A Chatter, Is the Rally Backed by Value?

Simply Wall St

Reviewed by Bailey Pemberton

- If you have ever wondered whether Kohl's stock offers good value or if the recent buzz is just noise, you are not alone. Let’s dive into what is actually happening with the share price.

- Kohl’s has caught the market’s attention by surging a remarkable 56.5% in the past week and boasting a 75.3% return year-to-date, signaling shifting sentiment or renewed growth potential.

- Much of this momentum has been linked to industry chatter around M&A interest and potential strategic shifts in the retail landscape, as headlines suggest possible suitors and activist investors are circling Kohl’s. These stories have injected fresh volatility and speculation into an already lively trading environment.

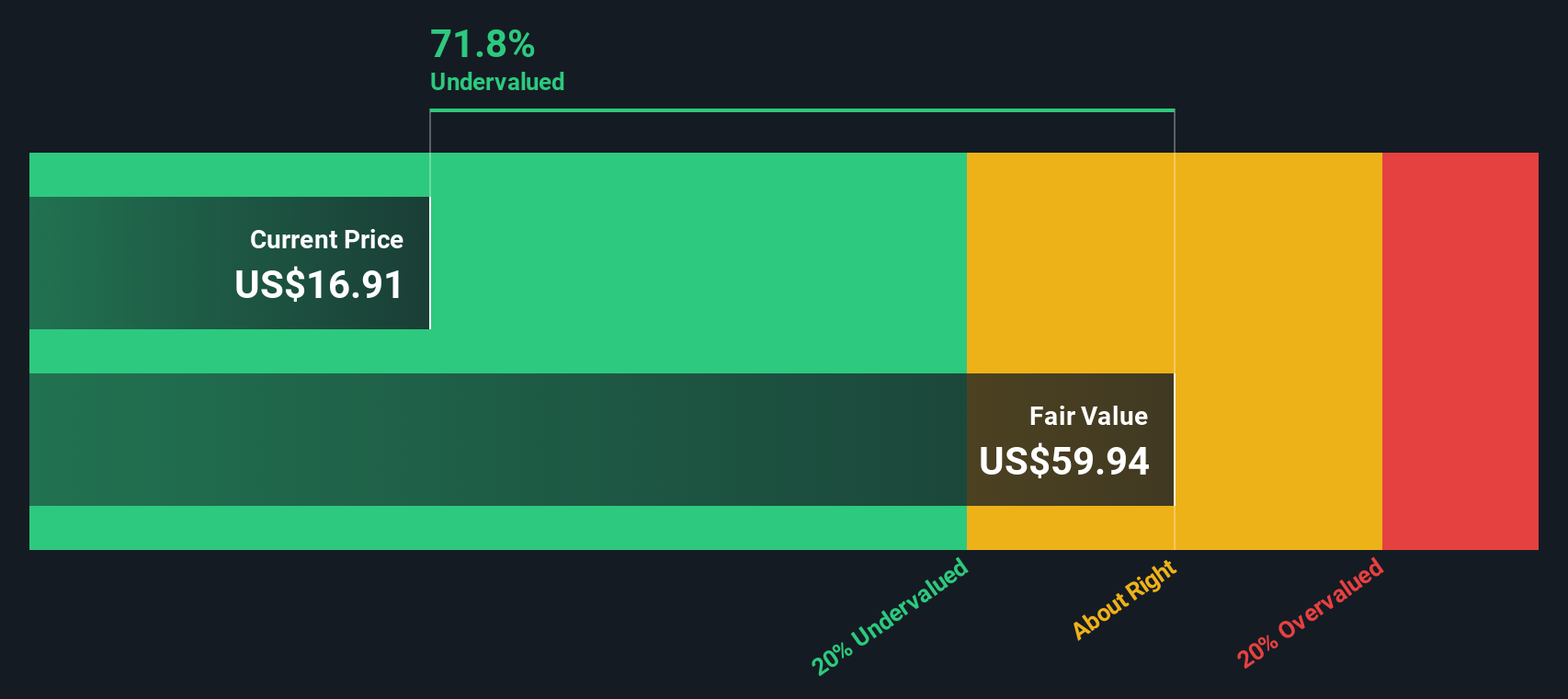

- According to our valuation analysis, Kohl’s currently earns a score of 5 out of 6 for undervaluation, suggesting there may be solid value locked in the stock. In the next sections, we will walk through how this score is calculated using different valuation methods. We will also share an even better way to think about value that could change how you view this company.

Approach 1: Kohl's Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's intrinsic value by projecting its future cash flows and then discounting them back to today using a rate that reflects risk and the time value of money. This approach helps investors assess what a business is fundamentally worth, regardless of daily market fluctuations.

For Kohl's, the DCF model is based on the “2 Stage Free Cash Flow to Equity” method. Currently, the company's Free Cash Flow stands at $771.8 million. Analyst projections, which extend up to five years, are then extrapolated for the following years, resulting in an estimated Free Cash Flow of $830.5 million in 2035. All values are reported in US dollars.

Taking these projections into account, the estimated intrinsic (fair) value for Kohl's is $62.91 per share. According to the DCF analysis, the stock is trading at a 60.9% discount to its fair value, which indicates it is significantly undervalued at current market prices.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Kohl's is undervalued by 60.9%. Track this in your watchlist or portfolio, or discover 920 more undervalued stocks based on cash flows.

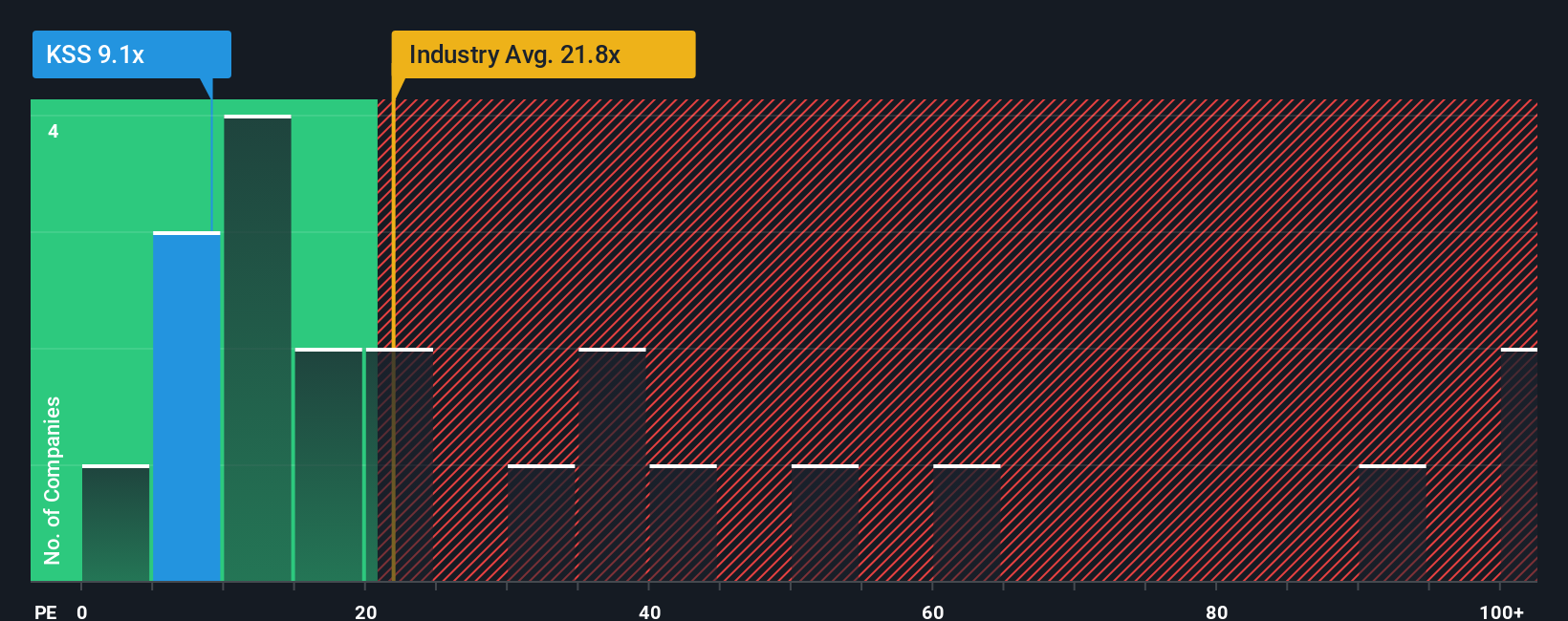

Approach 2: Kohl's Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used valuation tool for profitable companies because it directly relates a company’s current share price to its per-share earnings. For investors, the PE ratio offers a quick snapshot of what the market is willing to pay today for a dollar of those earnings. This makes it particularly useful for businesses with stable or growing profits like Kohl's.

A suitable or “fair” PE ratio generally reflects growth expectations and perceived risk. Higher expected earnings growth and lower risk usually justify a higher PE, while lower growth or elevated risk lead to a lower ratio. For Kohl's, the current PE ratio stands at 14.1x, which is notably below both the Multiline Retail industry average of 19.8x and the peer group average of 17.3x. This comparison may suggest the market is pricing Kohl's shares lower than some of its competitors, possibly due to company-specific concerns or industry sentiment.

To get a clearer perspective, Simply Wall St’s Fair Ratio combines a range of factors like a company’s earnings growth outlook, profit margins, business risks, industry type, and market cap. Unlike a simple peer or industry comparison, the Fair Ratio offers a more tailored benchmark for each business, allowing for a more nuanced and accurate fair value assessment. For Kohl’s, the proprietary Fair Ratio is calculated at 21.5x, materially higher than its current 14.1x PE multiple. This reinforced perspective suggests the stock may be undervalued based on the company’s fundamentals and expected growth versus risks.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Kohl's Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let’s introduce Narratives. A Narrative is a simple, powerful way for investors to connect their perspective on a company to its financials by telling the story behind the numbers. This includes your assumptions about future revenue, earnings, margins, and resulting fair value.

Narratives go beyond classic valuation formulas by linking what you believe about a company's future to an actual financial forecast and updated fair value. They are easy to create and share on Simply Wall St's Community page, making them accessible to millions of investors seeking clarity and collaboration.

With Narratives, you can quickly see if your story suggests it is time to buy, sell, or sit tight by comparing your Fair Value to the current price. As new news or earnings reports are released, each Narrative is updated in real-time, ensuring your outlook adapts to the latest developments.

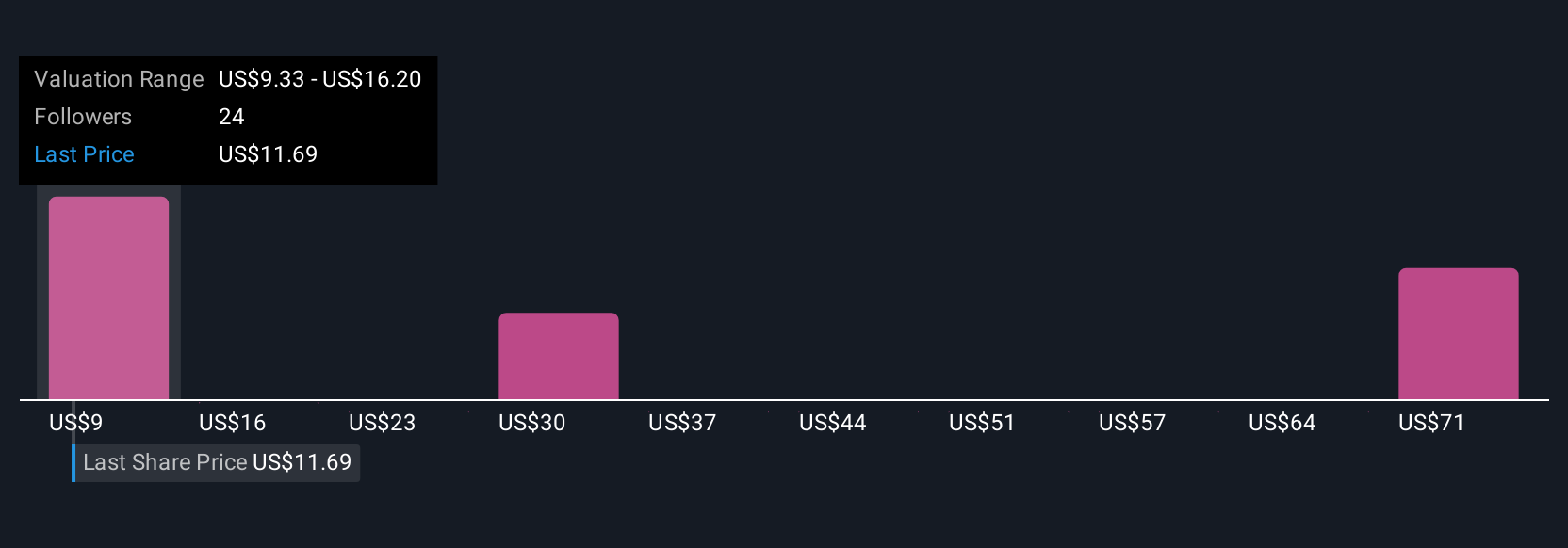

For example, some investors see Kohl's fair value as high as $34, based on optimism about real estate assets and cash flow, while others believe fair value is closer to $15, reflecting concerns about customer trends and retail headwinds. Which story matches your view? That is the power of Narratives. You can invest and track your thesis with clarity, context, and confidence.

For Kohl's, we offer easy-to-follow previews of two leading Kohl's Narratives:

- 🐂 Kohl's Bull Case

Fair Value: $34.00

Currently trading at 27.7% below this fair value

Expected Revenue Growth: 48.01%

- Kohl's market cap is now far below its $8 billion in real estate assets and the company still generates sizable free cash flows. Some view current stock prices as an overreaction with significant upside potential.

- The high short interest, around 50%, may be adding to downside pressure. Business fundamentals remain more resilient than market sentiment suggests.

- Current pricing is viewed by some as an attractive entry point. Even conservative valuations suggest significant room for long-term gains, and there is potential for buyouts or privatization at these levels.

- 🐻 Kohl's Bear Case

Fair Value: $15.61

Currently trading at 57.6% above this fair value

Expected Revenue Growth: -1.60%

- Analysts are concerned about ongoing declines in core customer transactions, weak sales growth, and limited progress in digital transformation, which may negatively affect future revenue and profitability.

- Rising labor costs, heavy promotions, and slow improvements in store traffic are expected to keep profit margins under pressure, despite efforts to manage inventory and expenses.

- The analyst consensus price target is $14.28, which is 16.4% below the current price. This suggests that recent optimism may have elevated market expectations above underlying fundamentals.

Do you think there's more to the story for Kohl's? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kohl's might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KSS

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative