Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:DASH

Producing a Successful Business may be Harder than it Seems for DoorDash, Inc's (NYSE:DASH)

There has been a decent amount of debate on the profitability of DoorDash, Inc. (NYSE:DASH) lately. While it is true, that the company's business model is not fully validated, we will attempt to make a weighted analysis between the risks and opportunities of the business.

Here is what we found with our analysis:

- DoorDash is unprofitable but actually free cash flow positive

- The main problem is not the cash burn, but creating lasting returns from marketing

- The company needs to build barriers to entry, otherwise risks losing business to competitors

Financial Snapshot

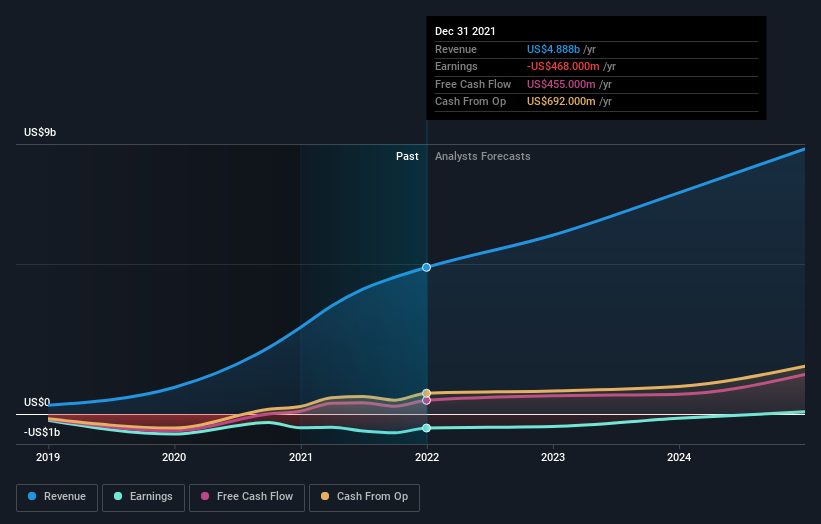

We start with the fundamental performance of the company. Many investors worry that the business expenses are so high, which can make the business unsustainable. There is good reason for concern - costs of revenue are US2.27b, making the gross profit US$2.6b, but high business expenses such as Sales and Marketing are US$1.6b. This, along with other business expenses, put the company "in the red", resulting in a net loss of US$465m.

These worries are not fully justified because the company is actually free cash flow positive - US$455m, and profits are expected to move to the right side of 0 by 2024.

There is a caveat here, which requires either growth to keep going or margins to improve for this to come true - In the next section, we will see why that is easier said than done.

Check out our latest analysis for DoorDash

There are two things to look at when assessing business expenses for DSAH. First, what is the logic behind them, and second, is whether the company gains long term or temporary growth. Investors understand that a business needs to spend in order to grow, but the concern is: if the consumer incentives disappear, will these consumers keep using the service?

Growth & Market Share

Looking at growth, it seems that the company did experience a large amount of growth between 2020 and 2022, with revenues jumping 452%. However, as people point out, revenue growth is decelerating as the company has reached the majority of market share in the industry.

We can see how this looks in the chart below:

In the last 12 months, DASH grew revenue by 69%, while in the year before that, they grew by 326%. At the same time, the company spent US$1.619b on marketing, a 70% increase from 2020.

While it is natural to assume that a young growth company will decelerate over time, investors need to know what is the company gaining in return for the marketing spend. To the extent that they are trying to reach and familiarize people as much as possible with their platform, they may be doing a good job. However, they need a way to make these customers stick with them, otherwise all of that marketing will just be an operating expense with no value-adding benefits. In this business, it seems that both vendors and customers converge to the lowest price, unless DoorDash has some barriers to entry in place.

Let's be specific, a barrier to entry is something that would be expensive to replicate, such as a quality app, network, exclusive contracts with vendors, etc. Even finding a way to derive local benefits or leasing high quality equipment to seasoned employees may make operations more efficient.

For example, one competitor, Uber Technologies (NASDAQ:UBER) with their Uber Eats division, is placing some competitive advantages in place. These include leveraging 1 app for all features (ride + delivery), utilizing a network of drivers, providing their drives with loyalty incentives such as car insurance benefits via Uber.

Also, can Uber launch an expensive campaign to grow market share?

Probably. It seems quite doable with a US$4.3b cash balance and a US$72.7b market cap.

Are they preparing the terrain before they jump into aggressive marketing?

Perhaps, or they just may be taking it one step at a time.

The last thing investors want to see is another ContextLogic (NASDAQ:WISH) scenario, where management bumped up sales through marketing, and it went crashing down (1Y return -83%) after the model became unsustainable.

Financial Health

In order to assess how long can management keep up with this approach, we need to analyze the balance sheet and the cash burn.

Well, the good news is that DASH has a healthy US$3.9b in cash, and with the current expenses, they are actually free cash flow positive. In reality, the company is making money with this setup.

We will still see a cash drain in the future, but it is good to know that management can scale back if they need to.

The company has a large market value of US$43b, so in case then need extra funding, they can issue a bit more shares. Investors should also expect that the company will start taking some debt as it approaches profitability. The interest is tax-deductible, so this will allow them to focus on some more growth projects.

Conclusion

As we have seen throw ought this analysis, DoorDash doesn't really have a spending problem, it has difficulties in creating lasting returns from all the money it spends.

The company needs to find a way to lift barriers to entry, otherwise most of their profits will be competed away, and the business will struggle with keeping the lights on.

On the bullish side, the company is in a favorable position regarding risk management - as a public entity, it has more tools at their disposal in order to manage funds and start more expensive projects.

Finally, the current valuation implies that DoorDash will eventually make US$2b+ in free cash flows, which may seem slightly optimistic, unless they find a way to keep competitors out.

Calculation: Market Cap * (Cost of Capital - Risk Free Rate) = US$43b * (0.072 - 0.024) = US$2b

So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. In terms of investment risks, we've identified 3 warning signs with DoorDash, and understanding them should be part of your investment process.

If you are no longer interested in DoorDash, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NasdaqGS:DASH

DoorDash

Operates a commerce platform that connects merchants, consumers, and independent contractors in the United States and internationally.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor