Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:CWH

Camping World Holdings' (NYSE:CWH) Shareholders Will Receive A Smaller Dividend Than Last Year

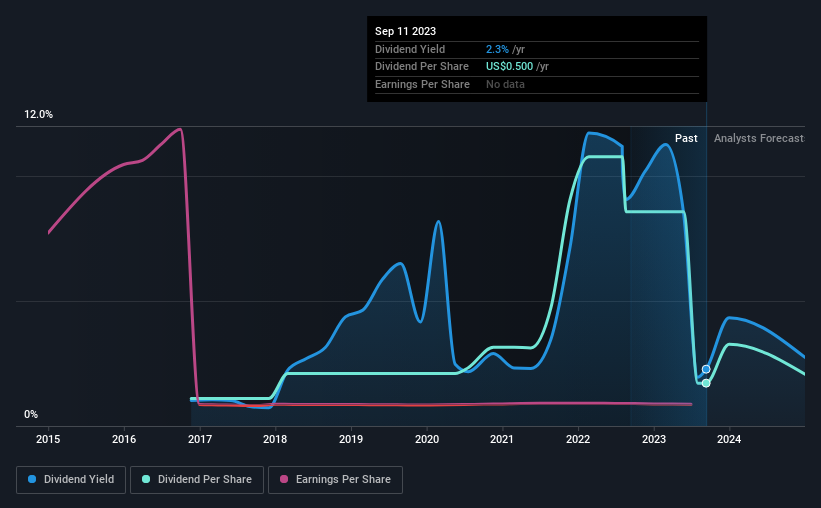

Camping World Holdings, Inc. (NYSE:CWH) is reducing its dividend from last year's comparable payment to $0.125 on the 29th of September. However, the dividend yield of 2.3% still remains in a typical range for the industry.

Check out our latest analysis for Camping World Holdings

Camping World Holdings Doesn't Earn Enough To Cover Its Payments

Solid dividend yields are great, but they only really help us if the payment is sustainable. Prior to this announcement, the company was paying out 272% of what it was earning, however the dividend was quite comfortably covered by free cash flows at a cash payout ratio of only 45%. Generally, we think cash is more important than accounting measures of profit, so with the cash flows easily covering the dividend, we don't think there is much reason to worry.

Over the next year, EPS is forecast to expand by 66.2%. If the dividend continues on its recent course, the payout ratio in 12 months could be 193%, which is a bit high and could start applying pressure to the balance sheet.

Camping World Holdings' Dividend Has Lacked Consistency

Looking back, Camping World Holdings' dividend hasn't been particularly consistent. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. Since 2016, the annual payment back then was $0.32, compared to the most recent full-year payment of $0.50. This works out to be a compound annual growth rate (CAGR) of approximately 6.6% a year over that time. We have seen cuts in the past, so while the growth looks promising we would be a little bit cautious about its track record.

Camping World Holdings May Find It Hard To Grow The Dividend

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. However, Camping World Holdings' EPS was effectively flat over the past five years, which could stop the company from paying more every year. Paying more than double what it is paying out, and not showing a track record of being able to grow earnings, we can only see dividend cuts in the future.

In Summary

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. We would probably look elsewhere for an income investment.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. To that end, Camping World Holdings has 3 warning signs (and 1 which is a bit concerning) we think you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:CWH

Camping World Holdings

Together its subsidiaries, retails recreational vehicles (RVs), and related products and services in the United States.

Reasonable growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|35.4% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.3% undervalued

MI

Community Contributor