- United States

- /

- Specialty Stores

- /

- NYSE:CHWY

Consumers' and Investor's Satisfaction is Diverging at Chewy (NYSE:CHWY)

Hopes and dreams often lead the market by a decent margin, as was the case with Chewy, Inc. (NYSE: CHWY), which reached peak valuation before temporarily turning profitable in 2021.

Yet, after missing the earnings for the third consecutive time, the stock is now over 60% below the highs as rising costs threaten the growth story.

Q4 Earnings Results

- Non-GAAP EPS: - US$0.11 (miss by US$0.03)

- Revenue: US$2.39b (miss by US$30m)

- Revenue Growth: +17.2% Y/Y

Check out our latest analysis for Chewy

The Nature of the Problem

Chewy is an online retailer offering a variety of pet food and pet-related items to order online. In the era of digital data, this provides a lot of space for personalization where Chewy can leverage the platform to cater to each client and drive sales by offering the pre-selected product for their pet.

Naturally, this creates large net sales per customer (US$430), but it also drives shipping & logistics costs. These costs hurt many businesses over the last months. For Chewy, they erased about 170 basis points from the gross margin, flipping the adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) to negative.

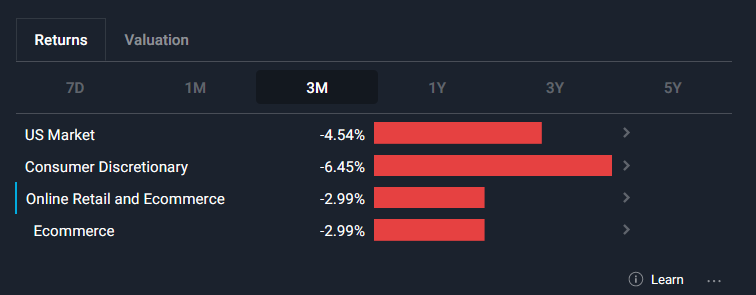

Current Sector Performance

The following chart shows the vertical sector breakdown:

After the first quarter of the year, the online retail and eCommerce market is down, but it is still slightly outperforming the broad market.

Analysts expect annual earnings growth of 25%, which is lower than the prior year's growth of 36%. You can find the analysis of the U.S online retail industry on our platform.

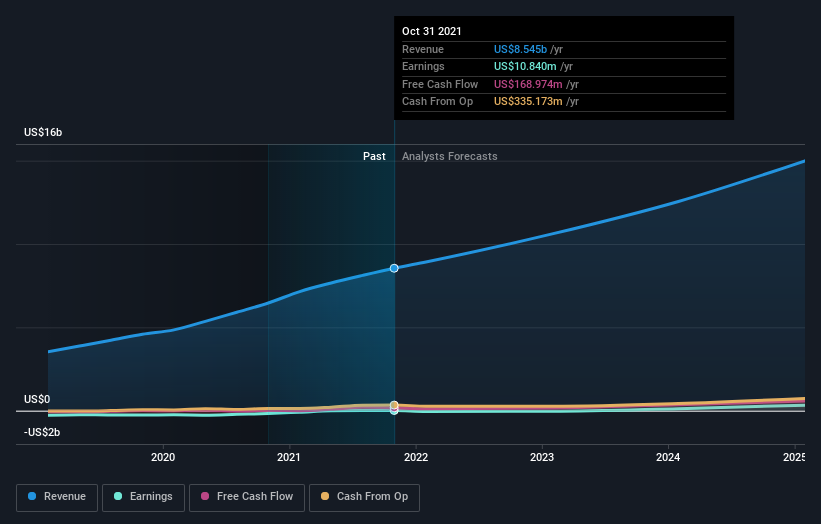

Forecasted Growth

Despite the near-term turbulence, the forecast for CHWY remains optimistic. Multiple analysts expect the company to return to profitability by 2024 while significantly growing its cash flow.

Currently, the growth forecast is 54%, more than double the industry forecast, which sits at 24.7%.

Conclusion

From a consumer standpoint, Chewy has all the marks of a quality company which can be seen by the growing net sale per customer. Yet, from an investors' perspective, it can be a headache, with extreme volatility and short interest reaching almost 30%.

While shorting the company can be a risky endeavor, given the cult following of the co-founder Ryan Cohen (CEO of GME), long-only investors who make the majority still have to evaluate the company's moat to see whether the growth story can survive the competitors like Amazon.com (NASDAQ: AMZN) - who are, if anything, much better positioned to fight-off the logistical pressures.

In terms of investment risks, we've identified 1 warning sign with Chewy, and understanding this should be part of your investment process.

If you are no longer interested in Chewy, you can use our free platform to see our list of over 50 other stocks with high growth potential.

If you're looking to trade Chewy, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Stjepan Kalinic

Stjepan is a writer and an analyst covering equity markets. As a former multi-asset analyst, he prefers to look beyond the surface and uncover ideas that might not be on retail investors' radar. You can find his research all over the internet, including Simply Wall St News, Yahoo Finance, Benzinga, Vincent, and Barron's.

About NYSE:CHWY

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives