Advertisement

- United States

- /

- Specialty Stores

- /

- NasdaqCM:RMBL

RumbleON's (NASDAQ:RMBL) Earnings Aren't As Good As They Appear

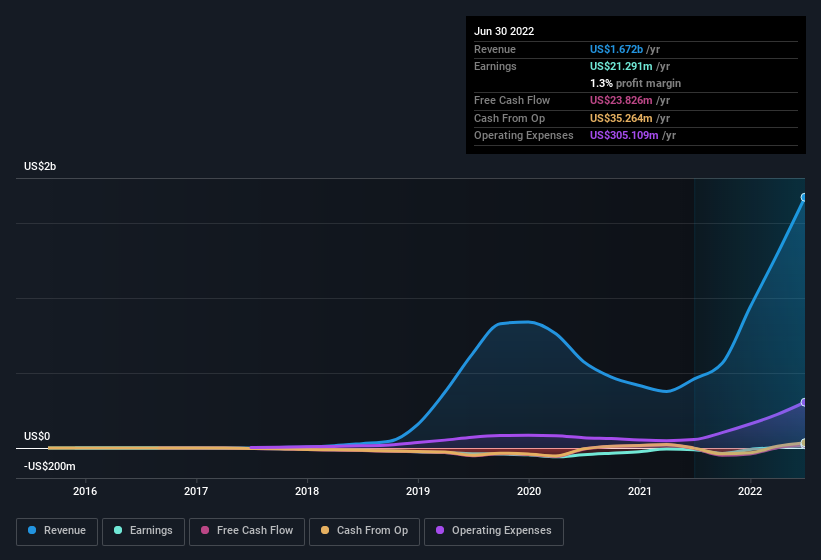

Strong earnings weren't enough to please RumbleON, Inc.'s (NASDAQ:RMBL) shareholders over the last week. Our analysis found several concerning factors in the earnings report beyond the strong statutory profit number.

Check out our latest analysis for RumbleON

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. RumbleON expanded the number of shares on issue by 371% over the last year. That means its earnings are split among a greater number of shares. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. Check out RumbleON's historical EPS growth by clicking on this link.

A Look At The Impact Of RumbleON's Dilution On Its Earnings Per Share (EPS)

RumbleON was losing money three years ago. Zooming in to the last year, we still can't talk about growth rates coherently, since it made a loss last year. What we do know is that while it's great to see a profit over the last twelve months, that profit would have been better, on a per share basis, if the company hadn't needed to issue shares. Therefore, one can observe that the dilution is having a fairly profound effect on shareholder returns.

In the long term, if RumbleON's earnings per share can increase, then the share price should too. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Operating Revenue Or Not?

Most companies divide classify their revenue as either 'operating revenue', which comes from normal operations, and other revenue, which could include government grants, for example. Oftentimes, non-operating revenue spikes are not repeated, so it makes sense to be cautious where non-operating revenue has made a very large contribution to total profit. Importantly, the non-operating revenue often comes without associated ongoing costs, so it can boost profit by letting it fall straight to the bottom line, making the operating business seem better than it really is. Alongside the dilution mentioned above, we think shareholders should note that RumbleON had a significant increase in non-operating revenue over the last year. Indeed, its non-operating revenue rose from US$1.69m last year to US$106.9m this year. If that non-operating revenue fails to manifest in the current year, then there's a real risk the bottom line profit result will be impacted negatively. In order to better understand a company's profit result, it can sometimes help to consider whether the result would be very different without a sudden increase in non-operating revenue.

Our Take On RumbleON's Profit Performance

In the last year RumbleON's non-operating revenue really gave it a boost, but not in a way that is necessarily going to be sustained. And the fact that it issued more shares means that its results look weaker from a per-share perspective. For the reasons mentioned above, we think that a perfunctory glance at RumbleON's statutory profits might make it look better than it really is on an underlying level. If you'd like to know more about RumbleON as a business, it's important to be aware of any risks it's facing. For instance, we've identified 3 warning signs for RumbleON (2 are a bit unpleasant) you should be familiar with.

Our examination of RumbleON has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:RMBL

RumbleOn

Provides powersports dealership and vehicle transportation services in the United States.

Undervalued with moderate growth potential.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor