Advertisement

- United States

- /

- Specialty Stores

- /

- NasdaqGS:PLCE

Why We Like The Returns At Children's Place (NASDAQ:PLCE)

There are a few key trends to look for if we want to identify the next multi-bagger. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. Speaking of which, we noticed some great changes in Children's Place's (NASDAQ:PLCE) returns on capital, so let's have a look.

Return On Capital Employed (ROCE): What Is It?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Children's Place:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.49 = US$186m ÷ (US$1.2b - US$793m) (Based on the trailing twelve months to July 2022).

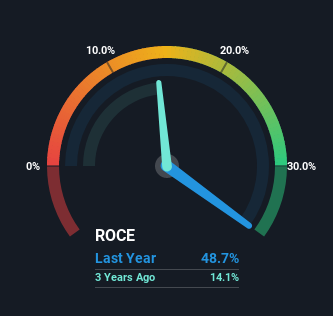

Thus, Children's Place has an ROCE of 49%. That's a fantastic return and not only that, it outpaces the average of 18% earned by companies in a similar industry.

Our analysis indicates that PLCE is potentially undervalued!

Above you can see how the current ROCE for Children's Place compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Children's Place.

What Can We Tell From Children's Place's ROCE Trend?

We're pretty happy with how the ROCE has been trending at Children's Place. We found that the returns on capital employed over the last five years have risen by 72%. The company is now earning US$0.5 per dollar of capital employed. In regards to capital employed, Children's Place appears to been achieving more with less, since the business is using 34% less capital to run its operation. A business that's shrinking its asset base like this isn't usually typical of a soon to be multi-bagger company.

On a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in current liabilities. Essentially the business now has suppliers or short-term creditors funding about 68% of its operations, which isn't ideal. Given it's pretty high ratio, we'd remind investors that having current liabilities at those levels can bring about some risks in certain businesses.

The Bottom Line

In a nutshell, we're pleased to see that Children's Place has been able to generate higher returns from less capital. Astute investors may have an opportunity here because the stock has declined 61% in the last five years. That being the case, research into the company's current valuation metrics and future prospects seems fitting.

If you'd like to know more about Children's Place, we've spotted 2 warning signs, and 1 of them is a bit concerning.

High returns are a key ingredient to strong performance, so check out our free list ofstocks earning high returns on equity with solid balance sheets.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:PLCE

Children's Place

Operates an omni-channel children’s specialty portfolio of brands in North America.

Moderate and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value US$31.72|41.9% undervalued

KI

Community Contributor

EasyJet weirdly unloved by investors in spite of relatively attractive metrics

Fair Value UK£6.95|31.9% undervalued

PI

Community Contributor

HEXPOL AB: Sustained Long Term Growth, Stable Margins, and Strategic M&A

Fair Value SEK 122.27|24.9% undervalued

MA

Community Contributor