- United States

- /

- Specialty Stores

- /

- NasdaqGS:KIRK

Health Check: How Prudently Does Kirkland's (NASDAQ:KIRK) Use Debt?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Kirkland's, Inc. (NASDAQ:KIRK) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Kirkland's

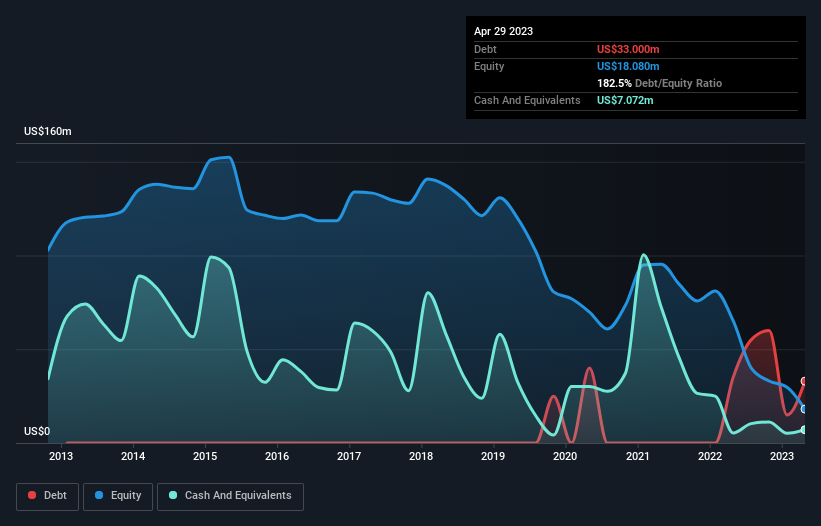

What Is Kirkland's's Net Debt?

As you can see below, Kirkland's had US$33.0m of debt at April 2023, down from US$35.0m a year prior. However, it does have US$7.07m in cash offsetting this, leading to net debt of about US$25.9m.

How Healthy Is Kirkland's' Balance Sheet?

The latest balance sheet data shows that Kirkland's had liabilities of US$104.8m due within a year, and liabilities of US$147.0m falling due after that. Offsetting this, it had US$7.07m in cash and US$590.0k in receivables that were due within 12 months. So its liabilities total US$244.1m more than the combination of its cash and short-term receivables.

The deficiency here weighs heavily on the US$40.0m company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we definitely think shareholders need to watch this one closely. After all, Kirkland's would likely require a major re-capitalisation if it had to pay its creditors today. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Kirkland's's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, Kirkland's made a loss at the EBIT level, and saw its revenue drop to US$492m, which is a fall of 8.5%. We would much prefer see growth.

Caveat Emptor

Importantly, Kirkland's had an earnings before interest and tax (EBIT) loss over the last year. Its EBIT loss was a whopping US$40m. When you combine this with the very significant balance sheet liabilities mentioned above, we are so wary of it that we are basically at a loss for the right words. Sure, the company might have a nice story about how they are going on to a brighter future. But the reality is that it is low on liquid assets relative to liabilities, and it lost US$49m in the last year. So we're not very excited about owning this stock. Its too risky for us. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Be aware that Kirkland's is showing 2 warning signs in our investment analysis , you should know about...

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Kirkland's might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:KIRK

Kirkland's

Operates as a specialty retailer of home décor and furnishings in the United States.

Low and slightly overvalued.

Similar Companies

Market Insights

Community Narratives