Advertisement

- United States

- /

- Specialty Stores

- /

- NasdaqGS:FIVE

Five Below's (NASDAQ:FIVE) Solid Earnings May Rest On Weak Foundations

The stock price didn't jump after Five Below, Inc. (NASDAQ:FIVE) posted decent earnings last week. We think that investors might be worried about some concerning underlying factors.

View our latest analysis for Five Below

Zooming In On Five Below's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. The accrual ratio subtracts the FCF from the profit for a given period, and divides the result by the average operating assets of the company over that time. The ratio shows us how much a company's profit exceeds its FCF.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

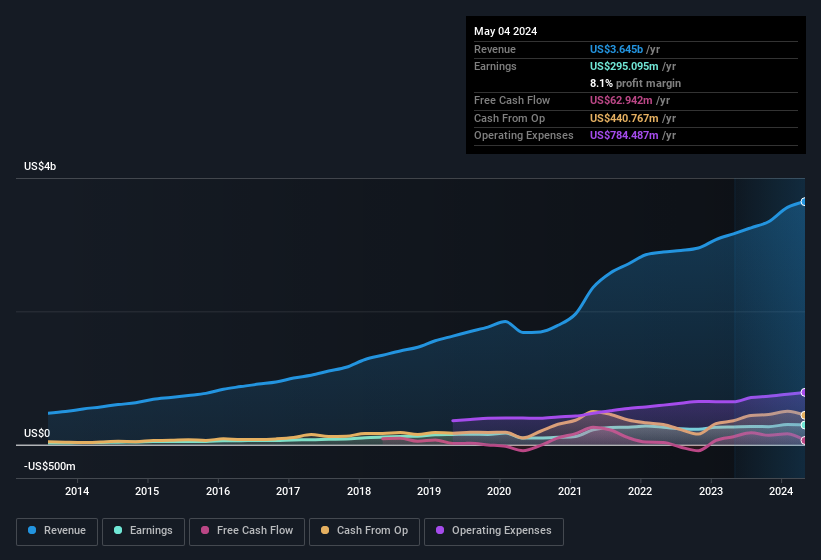

For the year to May 2024, Five Below had an accrual ratio of 0.21. We can therefore deduce that its free cash flow fell well short of covering its statutory profit. To wit, it produced free cash flow of US$63m during the period, falling well short of its reported profit of US$295.1m. Five Below's free cash flow actually declined over the last year, but it may bounce back next year, since free cash flow is often more volatile than accounting profits.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Five Below's Profit Performance

Five Below didn't convert much of its profit to free cash flow in the last year, which some investors may consider rather suboptimal. Because of this, we think that it may be that Five Below's statutory profits are better than its underlying earnings power. Nonetheless, it's still worth noting that its earnings per share have grown at 33% over the last three years. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. If you want to do dive deeper into Five Below, you'd also look into what risks it is currently facing. At Simply Wall St, we found 1 warning sign for Five Below and we think they deserve your attention.

This note has only looked at a single factor that sheds light on the nature of Five Below's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:FIVE

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8230.1% undervalued

63 followersusers have followed this narrative

5 commentsusers have commented on this narrative

31 likesusers have liked this narrative

WO

woodworthfund on Bumble ·

Swiped Left by Wall Street: The BMBL Rebound Trade

Fair Value:US$960.6% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Duolingo ·

Duolingo (DUOL): Why A 20% Drop Might Be The Entry Point We've Been Waiting For

Fair Value:US$268.6439.8% undervalued

37 followersusers have followed this narrative

5 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

DA

davidlsander on 01 Quantum ·

QDay is coming - 01 Quantum hold the key

Fair Value:CA$1.554.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IV

Ivoed on Alexandria Real Estate Equities ·

Alexandria Real Estate Equities Is Going to Transform With a 27.2% Future Pe Ratio

Fair Value:US$8838.2% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15077.5% undervalued

69 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8230.1% undervalued

63 followersusers have followed this narrative

5 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AG

Agricola on Excellon Resources ·

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Fair Value:CA$31.898.3% undervalued

71 followersusers have followed this narrative

14 commentsusers have commented on this narrative

23 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25440.9% overvalued

75 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative