Advertisement

- United States

- /

- General Merchandise and Department Stores

- /

- NasdaqGS:BZUN

Baozun (NasdaqGS:BZUN) Net Loss Deepens in Q3, Raising Doubts on Profitability Turnaround Narratives

Simply Wall St

Reviewed by Simply Wall St

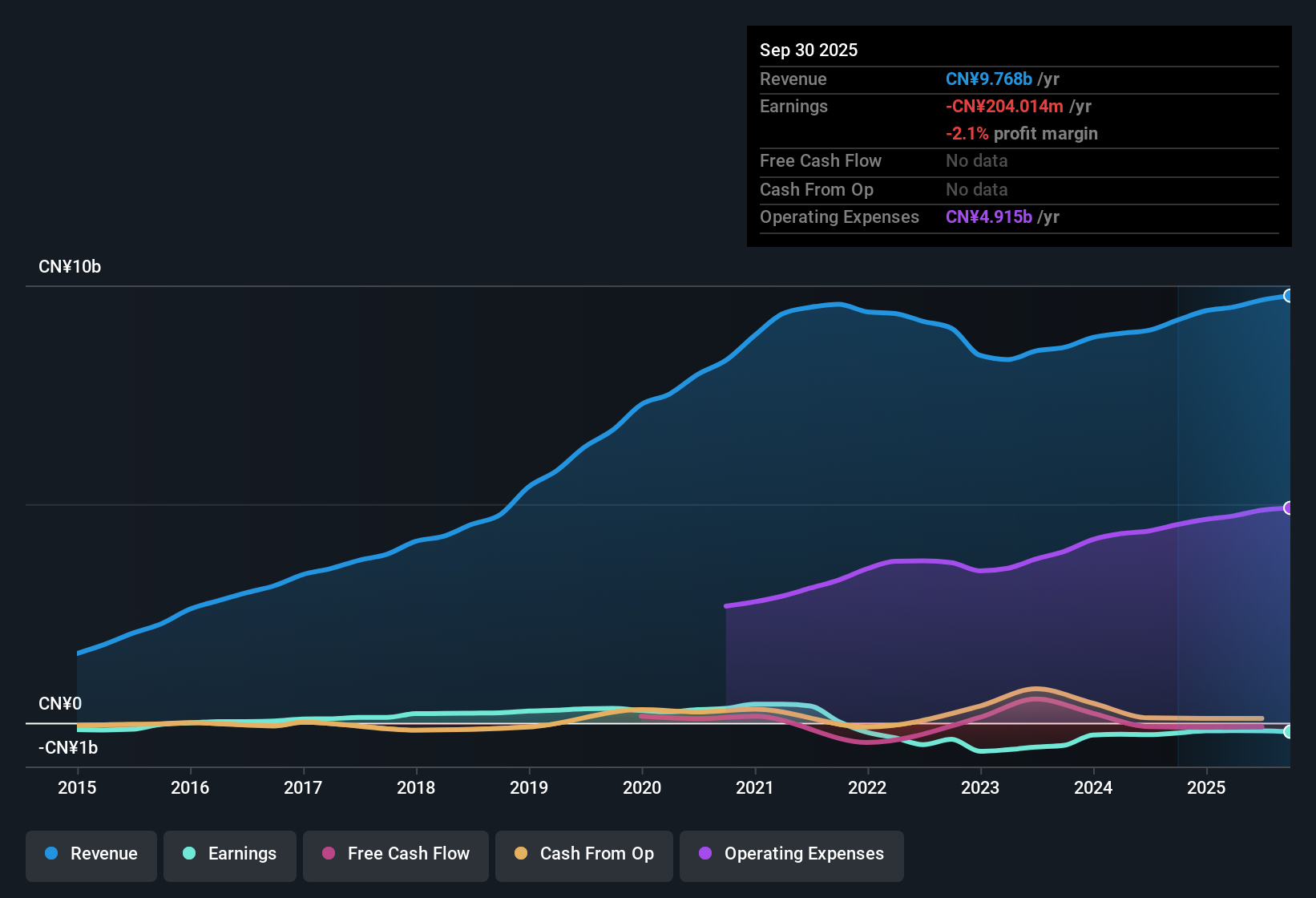

Baozun (NasdaqGS:BZUN) just released its Q3 2025 results, posting revenue of ¥2.2 billion and a basic EPS of -¥1.85. The company’s performance across the prior quarters shows revenue ranging from ¥2.1 billion to ¥3.0 billion, with basic EPS varying between 0.00 and -¥1.09. Investors will be closely watching as margins continue to be pressured by persistent losses.

See our full analysis for Baozun.Next, we compare these latest numbers with the top narrative themes from the Simply Wall St community to see which investor stories are confirmed and which may be challenged by the data.

See what the community is saying about Baozun

Losses Deepen, But Turnaround Hints Remain

- Baozun’s trailing twelve month net income stands at -204.0 million CNY, nearly double the loss from last year’s -107.1 million CNY for Q3 alone. This continues the negative trend from -184.9 million CNY in Q2 and -181.6 million CNY in Q1.

- According to the consensus narrative, ongoing integration of new brands and a shift toward higher-margin services are expected to drive an earnings rebound. However, the fact that margins have not improved year-over-year directly undercuts hopes for near-term profitability.

- The analysts’ consensus view highlights that net profit margin remains in negative territory despite management’s focus on expansion into digital marketing and SaaS, which were intended to lift earnings power.

- Persistent deepening of net losses and lack of sequential operating margin progress prompt caution even as revenue grows, challenging the strength of the turnaround case.

- Consensus narrative points to digital adoption and omnichannel expansion setting the stage for future gains, but real world losses continue to overshadow the recovery thesis. See if the full consensus narrative changes your perspective. 📊 Read the full Baozun Consensus Narrative.

DCF Fair Value Sits Four Times Above Share Price

- Baozun trades at 2.77 CNY per share, a 75.4% discount to its DCF fair value of 11.27 CNY, with a Price-to-Sales Ratio of just 0.1x compared to the multiline retail industry average of 1.5x.

- The consensus narrative acknowledges bargain-level valuation, drawing attention to growth catalysts like expanding brand management and scalable tech platforms. It also warns that a discount this steep is tied to real risks, mainly unproven earnings growth and competitive threats, which means the upside potential hinges on Baozun overcoming persistent profitability issues.

- What surprises many is how the company's severely discounted share price reflects not just below-industry growth, but also skepticism that forecasted earnings improvements will be realized in the next three years.

- Industry comparisons highlight Baozun’s relative value, but also serve as a warning that market doubts are deeply rooted as long as margin recovery remains out of reach.

Revenue Growth Lags Market, Earnings Forecast to Rebound

- Baozun’s revenue is forecast to rise by 4.4% per year over the next three years, well below the US market average of 10.5% per year. Earnings per share are projected to jump 87.43% annually, with expectations that the company will reach profitability by 2028.

- Consensus narrative notes the company’s ability to expand through omnichannel strategies and new service lines, supporting the outlook for a sharp earnings turnaround. However, it highlights that bears remain unconvinced unless revenue growth accelerates to offset rising costs and competition.

- Baozun’s reliance on a small pool of retail and brand partners means that a slowdown in topline growth, as seen in the latest quarters, could quickly erode the projected path to profitability.

- The earnings trajectory is set for a strong climb, but only if margin expansion and successful integration of new brands start translating into net income improvements.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Baozun on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Spot a different trend in the results? Share your unique take in just a few minutes and shape your own interpretation. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Baozun.

See What Else Is Out There

Baozun’s deepening losses and inconsistent margin recovery make its path to stable, predictable growth less certain than investors would like.

If steady performance matters to you, check out stable growth stocks screener (2073 results) to discover companies with consistent revenue and earnings expansion through market ups and downs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Baozun might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:BZUN

Baozun

Through its subsidiaries, engages in the provision of end-to-end e-commerce solutions in the People's Republic of China.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

74 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

45 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative