Advertisement

- United States

- /

- General Merchandise and Department Stores

- /

- NasdaqGS:AMZN

Assessing Amazon.com (AMZN) Valuation As AI And Cloud Partnerships Draw Fresh Investor Focus

Amazon.com (AMZN) is back in focus after a fresh wave of AI and cloud related news, including deeper ties with Anthropic and Snowflake and heavy capital spending on data center infrastructure.

See our latest analysis for Amazon.com.

The recent AI and cloud headlines sit on top of strong market interest, with a 30.5% 90 day share price return and a 33.2% 1 year total shareholder return, suggesting momentum has been building rather than fading.

If you are curious what other AI focused companies are attracting attention right now, it could be a good moment to scan the market using our screener of 47 AI infrastructure stocks

With Amazon trading at $274.00 and sitting about 14.1% below the average analyst price target and roughly 31% below one intrinsic value estimate, the key question is simple: is this genuine mispricing, or is the market already baking in years of AI driven growth?

Most Popular Narrative: 39.1% Undervalued

Against a last close of $274.00, the most followed narrative sets fair value at $450.00 per share, framing Amazon as materially mispriced rather than fairly valued.

Amazon is sacrificing short-term margins to secure long-duration dominance in AI infrastructure, advertising, and automated commerce. These investments are already working, and margins are positioned to inflect upward by the end of 2026.

This raises the question of what kind of growth and margin profile could justify a move from $274 to $450 per share. The narrative emphasizes AI-led cloud services, higher margin advertising, and a more profitable retail engine. The full story links those elements into a single valuation roadmap.

Result: Fair Value of $450.00 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upbeat view can be tested if AI and cloud spending fail to translate into stronger profitability, or if heavy capital investment keeps margins under pressure for longer than expected.

Find out about the key risks to this Amazon.com narrative.

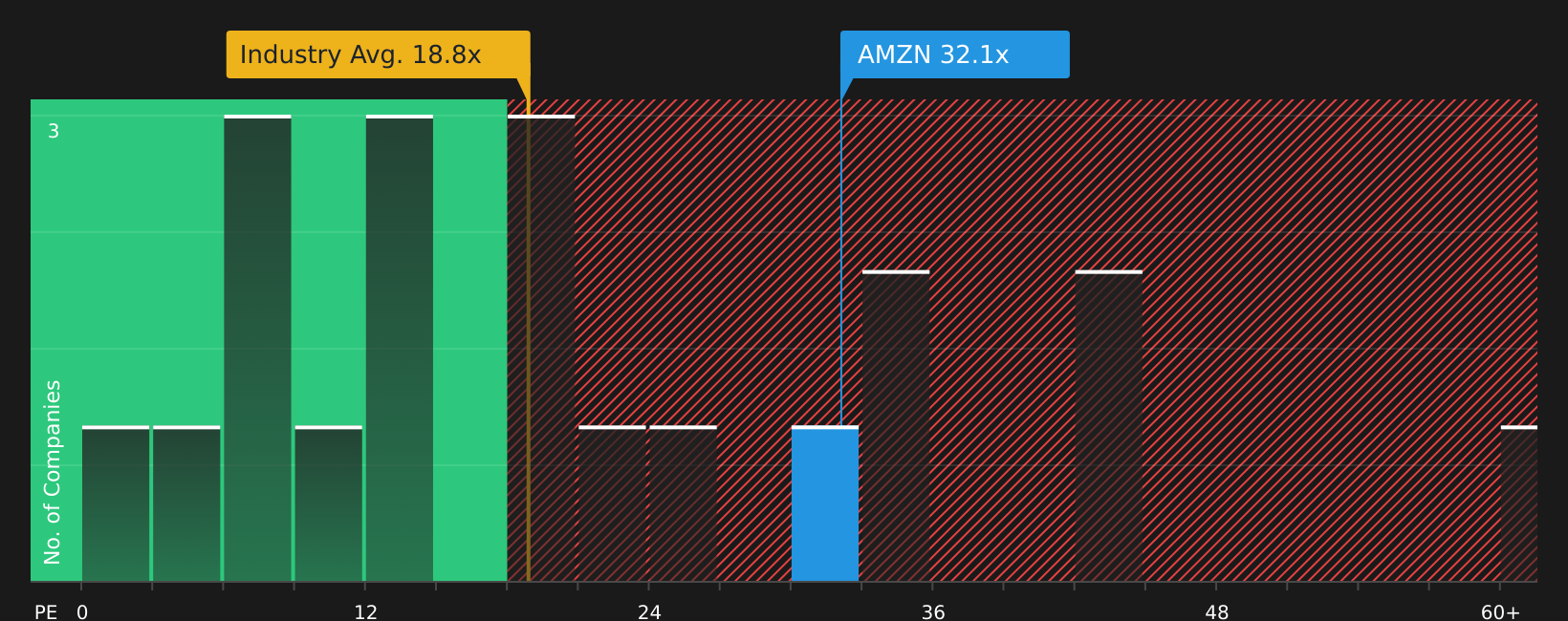

Another View: What The P/E Ratio Is Saying

While the user narrative leans on a $450 fair value, the current P/E of 32.5x tells a different story. It sits well above the global Multiline Retail industry at 18.9x and above a 24.1x peer average, yet below a 41.6x fair ratio that the market could move toward. For investors, that mix of premium pricing and theoretical headroom raises a simple question: is this justified strength or valuation risk if expectations cool?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With so much optimism and concern in the mix, it helps to see the full picture for yourself and decide where you stand. To weigh both sides in one place, review the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If Amazon has your attention, do not stop there. Broaden your watchlist with other focused stock ideas that could sharpen your overall approach.

- Spot potential long term compounders by scanning a curated set of 46 high quality undervalued stocks that pair quality fundamentals with prices below one estimate of fair value.

- Strengthen your income focus by reviewing 10 dividend fortresses that combine higher yields with an emphasis on durability of payouts.

- Prioritize resilience by checking 64 resilient stocks with low risk scores that aim to keep overall risk scores on the lower side while still offering equity upside.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:AMZN

Amazon.com

Engages in the retail sale of consumer products, advertising, and subscriptions service through online and physical stores in North America and internationally.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2537.3% undervalued

140 followersusers have followed this narrative

0 commentsusers have commented on this narrative

26 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0330.9% undervalued

15 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.528.6% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.726.1% undervalued

21 followersusers have followed this narrative

3 commentsusers have commented on this narrative

14 likesusers have liked this narrative

Recently Updated Narratives

ON

Ontological on Ryde Group ·

Ryde Group Ltd (NYSE American: RYDE): A High-Growth Challenger in Asia’s Digital Mobility and Quick Commerce

Fair Value:US$8.1789.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DR

DrPotato on Yum! Brands ·

Yum! Brands: A High-Quality Compounder With Continued Global Growth Potential

Fair Value:US$179.8317.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

tripledub on EDU Holdings ·

The Tiny Australian School Stock That Bought Back a Quarter of Itself While Nobody Was Looking

Fair Value:AU$1.7732.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28024.3% undervalued

248 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9117.4% overvalued

118 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$202.6286.4% overvalued

133 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

GR

greg_xasak on Fiserv ·

As someone who has dealt directly with them as a CTO for a credit union, I have 8 years of horror stories about doing business with them. If there was any other competitor than could deliver 80% of Fiserv services, there would be a mad rush to migrate to them. They should thank their lucky stars they are a near monopoly. this industry is so ripe for a well funded competitor. Their integration of technology is awful, their ability to fix their own implementation screwups is sadly tragic. Sometimes they just silently kill support tickets without resolution and you never find out until you do a follow up inquiry. Why, because sometimes no one you are dealing with knows how to fix it and knows no one to ask for help. They can not meet their own implementation deadlines and sometimes there is no one on a technical team dealing with you that has any banking or credit union experience. The is an industry insider phrase when you meet other Fiserv customers called being "Fiserved". It means telling others of your worst stories of dealing with them. Ask around, all CTO's have some doozies.

4

|0

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0