Advertisement

- United States

- /

- General Merchandise and Department Stores

- /

- NasdaqGS:AMZN

Assessing Amazon.com (AMZN) Valuation After Recent Share Price Volatility

Amazon.com (AMZN) continues to attract attention as investors weigh its recent share price moves, including a return of about 4% over the past month and a negative 10% over the past 3 months.

See our latest analysis for Amazon.com.

The recent rebound, including a 5.1% 7 day share price return and a 3.6% 30 day share price return, contrasts with a 10.2% 90 day share price decline, while the 1 year total shareholder return of 15.8% reflects stronger longer term momentum.

If you are looking beyond Amazon.com for other tech driven opportunities, this could be a useful moment to scan 36 AI infrastructure stocks

With Amazon.com trading at $221.25 and shown as a 37% discount to one intrinsic value estimate, the key question is whether this reflects genuine undervaluation or if the market is already factoring in much of its future growth potential?

Most Popular Narrative: 50.8% Undervalued

At $221.25 per share, the most followed narrative pegs Amazon.com’s fair value at $450. This frames the current price as a deep discount and presents a very bullish long term story.

Amazon (AMZN) enters 2026 materially misunderstood by the market. My valuation of $450 per share implies the stock is approximately 48% undervalued, not because Amazon is executing poorly, but because the market is mispricing intentional margin compression driven by some of the most strategically sound investments in the company’s history.

The narrative emphasizes how AI heavy capex, margin compression, and future earnings power intersect. It links cloud, advertising, and retail into one valuation story. It also raises the question of which specific revenue mix and margin path are used to support that $450 figure.

Result: Fair Value of $450 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this story can break if heavy AI and infrastructure spending lasts longer than expected or if AWS and advertising growth assumptions prove too optimistic.

Find out about the key risks to this Amazon.com narrative.

Another View: Richer On Earnings

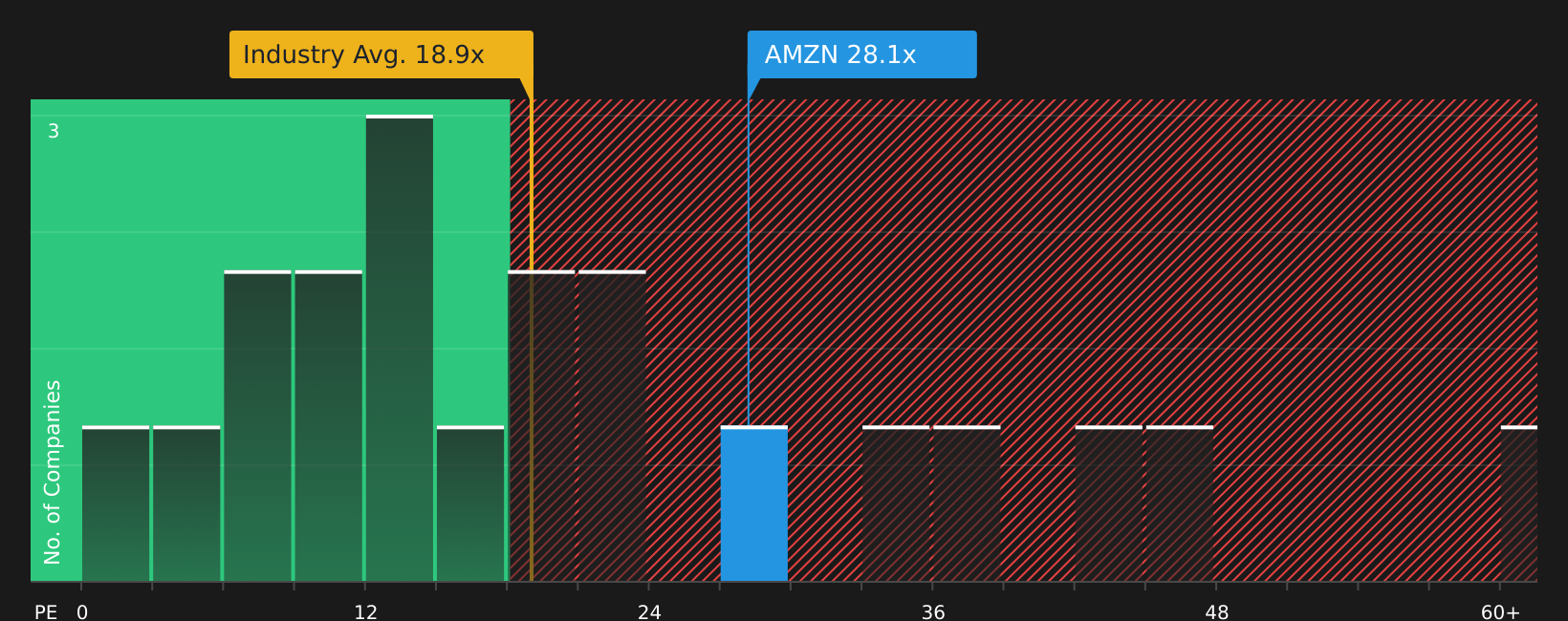

While one narrative sees Amazon.com as deeply undervalued, the earnings based view tells a tighter story. At a P/E of 30.6x versus peers on 27x and the Multiline Retail industry on 21.5x, Amazon.com already carries a premium even though the fair ratio points to 38.3x as a level the market could move toward. Is that premium a cushion or a source of valuation risk if sentiment cools?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment clearly split between opportunity and risk, this is a good moment to look through the data yourself and decide what really matters to you, starting with 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If Amazon.com is already on your radar, now is a smart time to broaden your watchlist with other clear, data backed ideas before the crowd spots them.

- Target potential mispricings by scanning a focused set of 63 high quality undervalued stocks that pair strong fundamentals with supportive valuations.

- Strengthen your income stream by reviewing 12 dividend fortresses that combine high yields with the potential for more dependable payouts.

- Dial down portfolio stress by checking 72 resilient stocks with low risk scores that score well on financial resilience and downside protection.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:AMZN

Amazon.com

Engages in the retail sale of consumer products, advertising, and subscriptions service through online and physical stores in North America and internationally.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

67 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8210.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

4 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

Faltaren on AmpliTech Group ·

AmpliTech Group Will Triple Revenue by 2030 with O-RAN Expansion

Fair Value:US$3078.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

67 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative