Advertisement

- United States

- /

- General Merchandise and Department Stores

- /

- NasdaqGS:AMZN

Assessing Amazon.com (AMZN) Valuation After Launch Of Amazon Supply Chain Services

Why Amazon.com (AMZN) is suddenly a logistics stock story too

Amazon.com (AMZN) has turned a logistics-focused corner with the launch of Amazon Supply Chain Services, opening its freight, distribution, fulfillment, and parcel network to external businesses in direct competition with UPS and FedEx.

See our latest analysis for Amazon.com.

The launch of Amazon Supply Chain Services comes amid strong recent interest in the stock, with a 30 day share price return of 28.55% and a 1 year total shareholder return of 44.96%. This points to building momentum after recent earnings, AI spending updates, and new enterprise wins in logistics and cloud.

If this logistics and AI story has your attention and you want more potential opportunities tied to the same theme, it could be worth scanning 38 AI infrastructure stocks

With Amazon trading around $273.55 after a 1 year total shareholder return of about 45%, a value score of 3 and an indicated 25% intrinsic discount, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 39.2% Undervalued

Market pricing of $273.55 compared with a narrative fair value of $450 suggests a wide gap, and the narrative argues that current margins are not telling the full story.

Amazon is not underperforming. It is investing ahead of the curve.

The company is making disciplined, intelligent, long-term expenditures that temporarily suppress margins while dramatically expanding future earnings capacity. This is the same playbook Amazon has run for decades and the same playbook that has repeatedly rewarded patient investors.

Want to see what sits behind that $450 fair value? The narrative focuses on AI led AWS growth, rising advertising profits, and a richer margin mix. Curious which earnings and revenue paths are included in those expectations, and how they aim to justify that valuation gap?

Result: Fair Value of $450 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on AI and logistics investments scaling as planned, and any slowdown in AWS or ad demand could quickly challenge that $450 fair value story.

Find out about the key risks to this Amazon.com narrative.

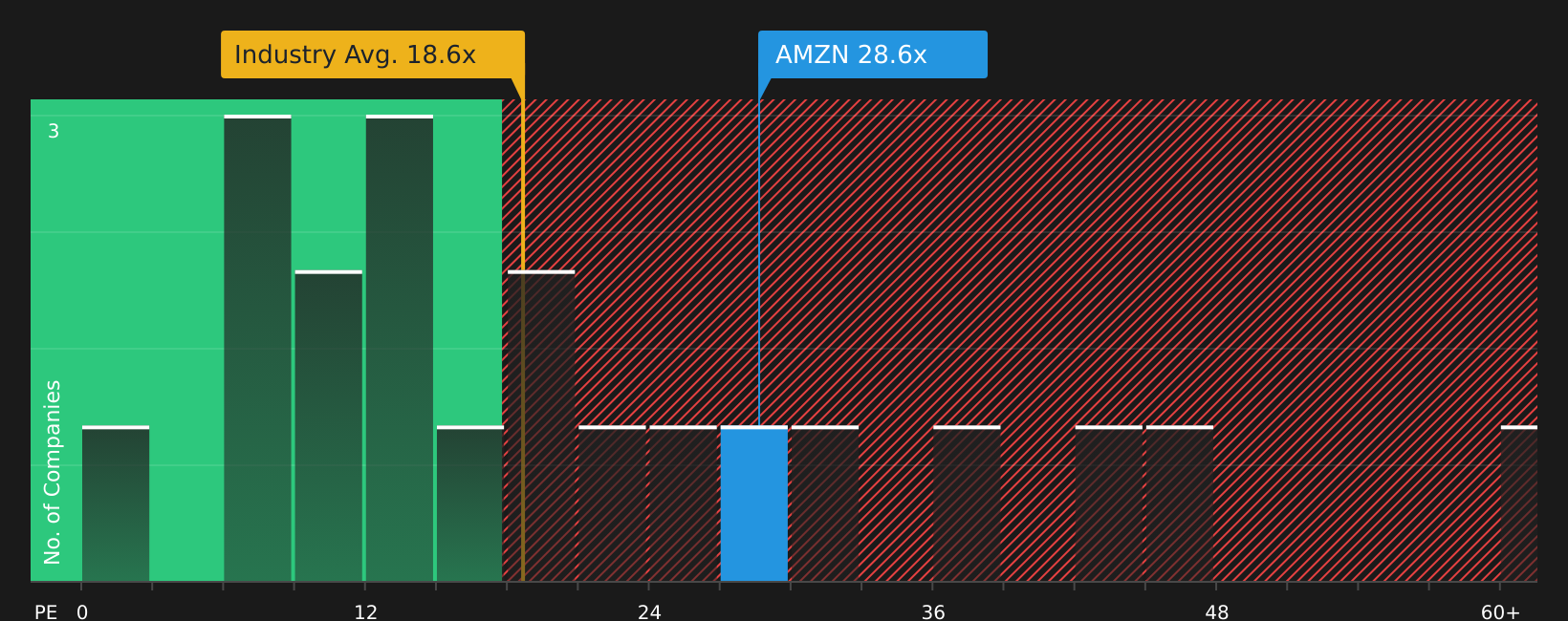

Another View: Earnings Multiple Sends a Different Signal

While the user narrative sees Amazon.com as materially undervalued, the P/E of 32.4x tells a tighter story. It sits above both the North American Multiline Retail average of 22.6x and the peer average of 27.6x, yet below a fair ratio of 41.5x that the market could move toward.

In practice, that means you are paying more than the sector and peer pack for each dollar of earnings today, but still at a discount to where the fair ratio suggests the P/E might settle. Is that a reasonable premium for Amazon.com’s earnings profile, or a margin of safety that could close?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Seeing mixed signals on value and growth potential here? Act quickly: look through the full set of risk and reward data, and weigh it against your own expectations with 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop with just one stock, you could miss out on opportunities that fit your style even better, so keep hunting for ideas that truly match your goals.

- Target potential mispricing by scanning 51 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect their financial strength.

- Strengthen your income focus by checking 13 dividend fortresses featuring higher yielding companies that prioritize returning cash to shareholders.

- Sleep a little easier by reviewing 72 resilient stocks with low risk scores that score well on financial resilience and business risk.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:AMZN

Amazon.com

Engages in the retail sale of consumer products, advertising, and subscriptions service through online and physical stores in North America and internationally.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

18 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5297.0% undervalued

4 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

Faltaren on AmpliTech Group ·

AmpliTech Group Will Triple Revenue by 2030 with O-RAN Expansion

Fair Value:US$3076.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.166.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative