Advertisement

- United States

- /

- Hotel and Resort REITs

- /

- NYSE:RLJ

3 Undervalued Small Caps With Recent Insider Activity In Global Markets

Simply Wall St

Reviewed by Simply Wall St

The United States market has shown positive momentum, climbing by 2.8% over the past week and rising 7.6% over the last year, with earnings growth anticipated at 14% per annum in the coming years. In this environment, identifying stocks that are potentially undervalued can be crucial for investors seeking opportunities, especially when these stocks also exhibit recent insider activity which may suggest confidence in their future prospects.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Shore Bancshares | 10.5x | 2.4x | 6.92% | ★★★★★☆ |

| First United | 9.8x | 2.6x | 46.62% | ★★★★★☆ |

| MVB Financial | 11.3x | 1.5x | 28.11% | ★★★★★☆ |

| Thryv Holdings | NA | 0.8x | 14.07% | ★★★★★☆ |

| S&T Bancorp | 10.9x | 3.7x | 42.31% | ★★★★☆☆ |

| Citizens & Northern | 12.4x | 3.0x | 43.36% | ★★★☆☆☆ |

| West Bancorporation | 14.3x | 4.4x | 42.32% | ★★★☆☆☆ |

| Columbus McKinnon | 57.3x | 0.5x | 40.62% | ★★★☆☆☆ |

| Franklin Financial Services | 14.6x | 2.3x | 31.53% | ★★★☆☆☆ |

| Delek US Holdings | NA | 0.1x | -224.98% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

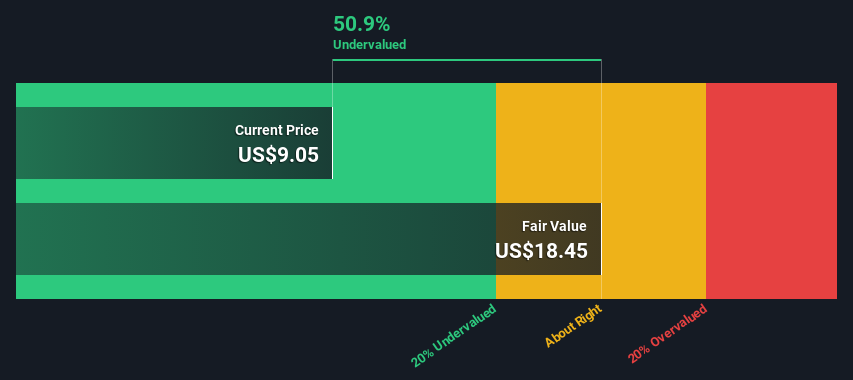

Amplitude (NasdaqCM:AMPL)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Amplitude is a company that specializes in providing digital optimization system software and programming services, with a market cap of approximately $1.33 billion.

Operations: The company generates revenue primarily from its Software & Programming segment, with a recent figure of $299.27 million. Over time, the gross profit margin has shown an upward trend, reaching 74.30% by the end of 2024. Operating expenses are largely driven by Sales & Marketing and R&D costs, which were $168.31 million and $97.57 million respectively in the latest period reported.

PE: -16.2x

Amplitude, a small company in the tech sector, recently welcomed Tien Tzuo to its board, bringing valuable expertise from his time at Salesforce and Zuora. Despite reporting a net loss of US$32.59 million for Q4 2024, revenue grew to US$78.13 million from US$71.4 million year-on-year. The company's revenue is expected to rise between US$324.8 and US$330.8 million in 2025, although profitability remains elusive due to reliance on external borrowing for funding without customer deposits as a buffer.

- Click here to discover the nuances of Amplitude with our detailed analytical valuation report.

Examine Amplitude's past performance report to understand how it has performed in the past.

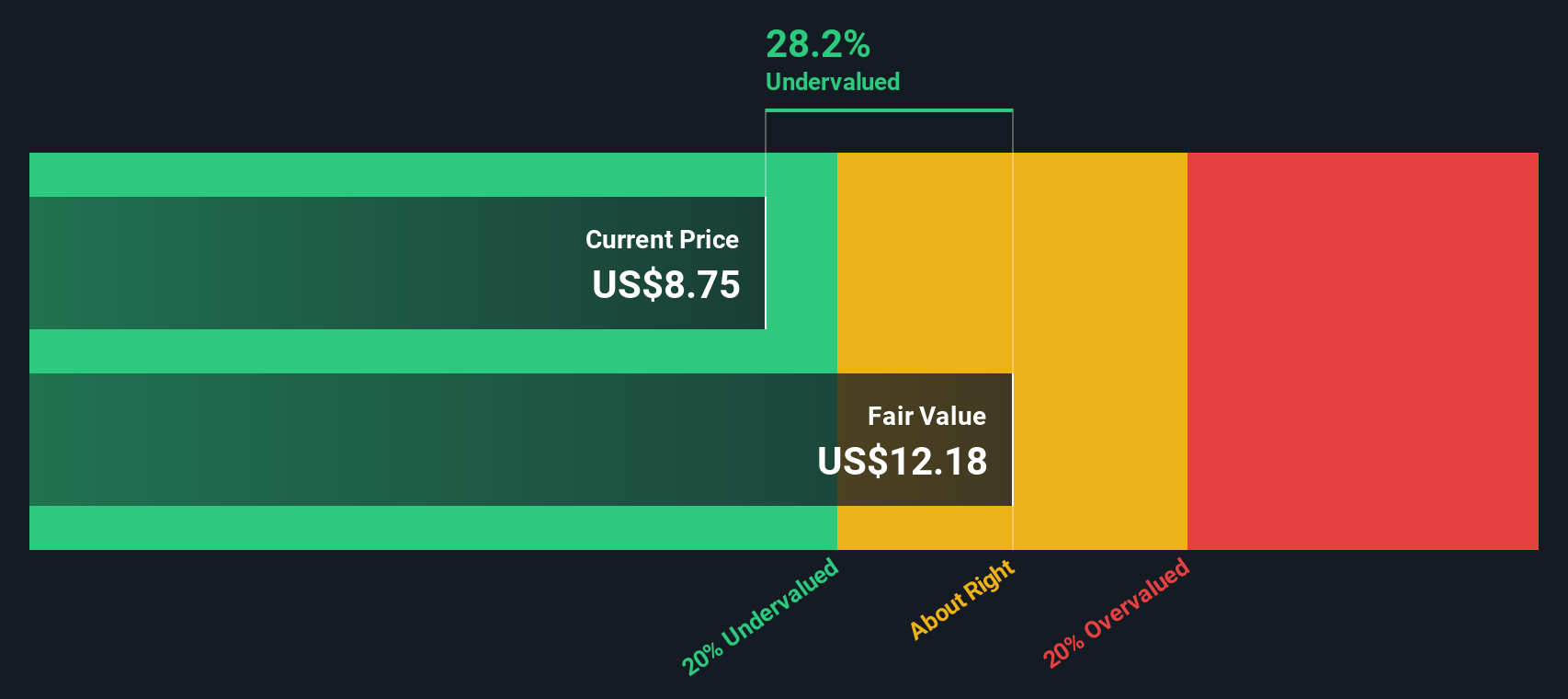

Enviri (NYSE:NVRI)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Enviri operates through three main segments: Clean Earth, Harsco Rail, and Harsco Environmental, with a combined market presence in waste management and environmental services.

Operations: Enviri generates revenue primarily from its Clean Earth, Harsco Rail, and Harsco Environmental segments. The company has experienced fluctuations in its gross profit margin, reaching 24.87% in Q4 2018 and 17.59% in Q2 2022. Operating expenses are a significant cost component, with general and administrative expenses consistently forming a large part of these costs across the periods reviewed.

PE: -4.4x

Enviri, a small-cap company facing challenges in profitability, recently amended its Credit Agreement and Securitization Facility to enhance financial flexibility amid global steel industry uncertainties. Despite reporting a net loss of US$83 million for Q4 2024, the company is actively engaging shareholders with proposed board changes at the upcoming AGM. Investor activism highlights governance and strategic issues, urging leadership overhaul to unlock potential value. While insider confidence isn't evident through recent purchases, strategic adjustments may position Enviri for future improvements.

- Get an in-depth perspective on Enviri's performance by reading our valuation report here.

Assess Enviri's past performance with our detailed historical performance reports.

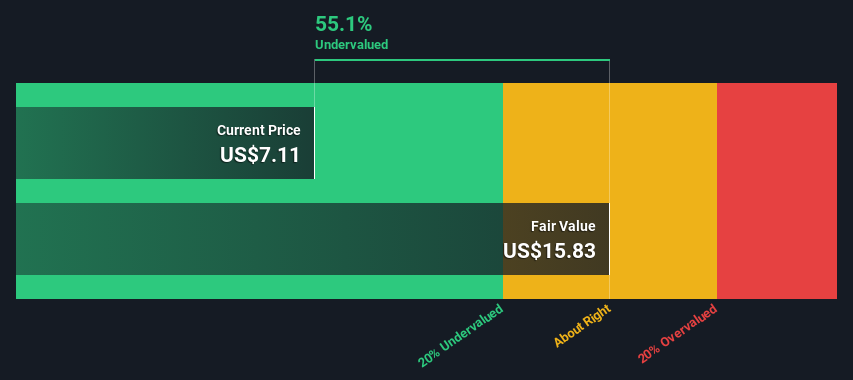

RLJ Lodging Trust (NYSE:RLJ)

Simply Wall St Value Rating: ★★★★★☆

Overview: RLJ Lodging Trust is a real estate investment trust that primarily invests in premium-branded, focused-service and compact full-service hotels, with a market capitalization of approximately $2.66 billion.

Operations: The primary revenue stream is from hotel operations, generating $1.37 billion. The gross profit margin has shown a declining trend, reaching 28.07% by the end of 2024. Operating expenses and cost of goods sold significantly impact profitability, with notable allocations towards depreciation and amortization expenses.

PE: 31.8x

RLJ Lodging Trust, a hospitality-focused REIT, is gaining attention in the investment community due to its potential for growth and recent strategic moves. The company completed a buyback of 3.39 million shares for US$32.24 million by February 2025, reflecting management's confidence in its valuation. Despite reporting a slight decline in net income to US$68 million for 2024, RLJ continues to pay dividends on both common and preferred shares, showcasing commitment to shareholder returns. With anticipated earnings growth of 10.53% annually and ongoing leadership transitions following CFO Sean Mahoney's retirement announcement, RLJ is positioning itself strategically within the market while navigating higher-risk external funding sources effectively.

- Unlock comprehensive insights into our analysis of RLJ Lodging Trust stock in this valuation report.

Summing It All Up

- Dive into all 74 of the Undervalued US Small Caps With Insider Buying we have identified here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:RLJ

RLJ Lodging Trust

RLJ Lodging Trust ("RLJ") is a self-advised, publicly traded real estate investment trust that owns 94 premium-branded, rooms-oriented, high-margin, urban-centric hotels located within the heart of demand locations.

Average dividend payer and fair value.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor