- United States

- /

- Residential REITs

- /

- NYSE:INVH

Leadership Shift: Invitation Homes (NYSE:INVH) Promotes Timothy J. Lobner to COO

Reviewed by Simply Wall St

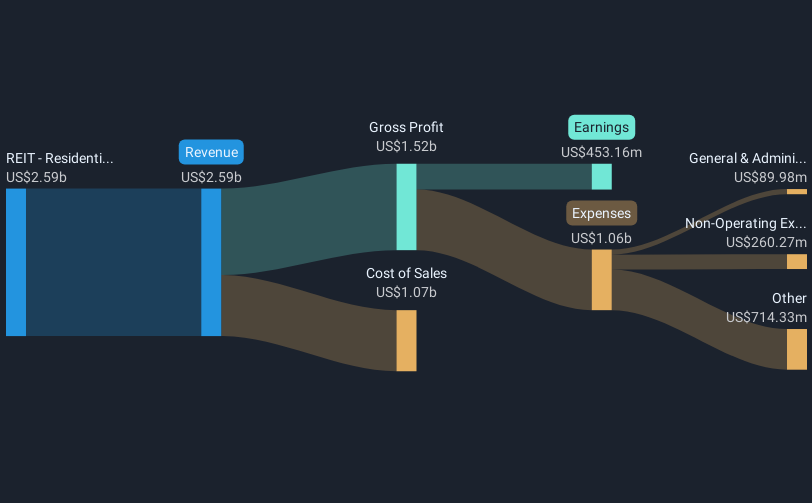

Invitation Homes (NYSE:INVH) recently declared a quarterly cash dividend of $0.29 per share, maintaining investor expectations for stable income, even as its stock price remained flat over the last quarter. During this period, the company posted strong fourth-quarter and full-year revenue growth, though full-year net income declined. Meanwhile, the promotion of Timothy J. Lobner to COO marked significant leadership changes. These corporate developments occurred amid a volatile market backdrop, characterized by a 12% drop in the S&P 500, largely driven by tariff uncertainties affecting broader economic sentiment. Invitation Homes’ actions align with maintaining resilience amidst broader market declines.

Find companies with promising cash flow potential yet trading below their fair value.

The recent dividend announcement by Invitation Homes underscores its commitment to providing stable income for investors despite a flat stock price in the short term. Over the past five years, the company's total shareholder return, including dividends, was 45.12%, offering context to its longer-term positioning. However, in the past year, the company underperformed against the US Residential REITs industry, which returned 0.2%, and the broader US market, which saw a 3.8% decline.

The company's strategic moves, such as expanding through joint ventures and optimizing its portfolio, have the potential to bolster future revenue and operational efficiency. The successful promotion of Timothy J. Lobner to COO could further enhance operational effectiveness, supporting the narrative of scale and market density contributing to margin expansion. Despite these initiatives, Invitation Homes' continued resilience may be tested by economic shifts, high mortgage rates, and increasing property tax expenses, which could constrain rental growth and profitability.

Current market conditions, alongside analyst forecasts, place Invitation Homes in a position where its price of US$34.55 trades below the consensus analyst target of about US$36.82, implying a modest potential upside. However, achieving the target would require substantive revenue and earnings growth, given the forecasted PE ratio increase to 54.5x by 2028. Potential risks, such as new home supply pressures and elevated mortgage rates, may impact these growth plans. As always, it is essential for investors to assess these factors critically to draw informed conclusions about the company's future prospects.

Understand Invitation Homes' earnings outlook by examining our growth report.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:INVH

Invitation Homes

Invitation Homes, an S&P 500 company, is the nation’s premier single-family home leasing and management company, meeting changing lifestyle demands by providing access to high-quality, updated homes with valued features such as close proximity to jobs and access to good schools.

Fair value second-rate dividend payer.

Similar Companies

Market Insights

Community Narratives