Advertisement

- United States

- /

- Specialized REITs

- /

- NYSE:EXR

What You Need To Know Before Investing In Extra Space Storage Inc. (NYSE:EXR)

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Extra Space Storage Inc. is a US$14b large-cap, real estate investment trust (REIT) based in Salt Lake City, United States. REIT shares give you ownership of the company than owns and manages various income-producing property, whether it be commercial, industrial or residential. The structure of EXR is unique and it has to adhere to different requirements compared to other non-REIT stocks. Below, I'll look at a few important metrics to keep in mind as part of your research on EXR.

Check out our latest analysis for Extrace Storage

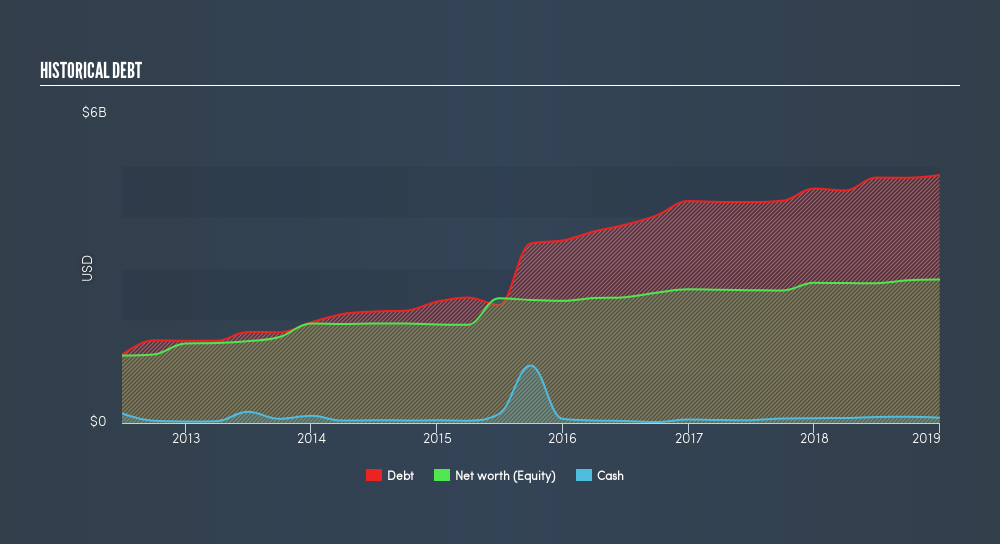

REIT investors should be familiar with the term Fund from Operations (FFO) – a REIT’s main source of cash flow from its day-to-day business activities. FFO is a higher quality measure of earnings because it takes out the impact of non-recurring sales and non-cash items such as depreciation. These items can distort the bottom line and not necessarily reflective of EXR’s daily operations. For EXR, its FFO of US$678m makes up 74% of its gross profit, which means the majority of its earnings are high-quality and recurring.

EXR's financial stability can be gauged by seeing how much its FFO generated each year can cover its total amount of debt. The higher the coverage, the less risky EXR is, broadly speaking, to have debt on its books. The metric I'll be using, FFO-to-debt, also estimates the time it will take for the company to repay its debt with its FFO. With a ratio of 14%, the credit rating agency Standard & Poor would consider this as significantly high risk. This would take EXR 7.1 years to pay off using just operating income, which is a long time, and risk increases with time. But realistically, companies have many levers to pull in order to pay back their debt, beyond operating income alone.

Next, interest coverage ratio shows how many times EXR’s earnings can cover its annual interest payments. Usually the ratio is calculated using EBIT, but for REITs, it’s better to use FFO divided by net interest. This is similar to the above concept, but looks at the nearer-term obligations. With an interest coverage ratio of 3.7x, it’s safe to say EXR is generating an appropriate amount of cash from its borrowings.

I also use FFO to look at EXR's valuation relative to other REITs in United States by using the price-to-FFO metric. This is conceptually the same as the price-to-earnings (PE) ratio, but as previously mentioned, FFO is more suitable. In EXR’s case its P/FFO is 20.19x, compared to the long-term industry average of 16.5x, meaning that it is overvalued.

Next Steps:

In this article, I've taken a look at Funds from Operations using various metrics, but it is certainly not sufficient to derive an investment decision based on this value alone. Extrace Storage can bring about diversification for your portfolio, but before you decide to invest, take a look at the other aspects you must consider before investing:

- Future Outlook: What are well-informed industry analysts predicting for EXR’s future growth? Take a look at our free research report of analyst consensus for EXR’s outlook.

- Valuation: What is EXR worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether EXR is currently mispriced by the market.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:EXR

Extra Space Storage

Extra Space Storage Inc., headquartered in Salt Lake City, Utah, is a self-administered and self-managed REIT and a member of the S&P 500.

Established dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor