If you hold Alexander’s (NYSE:ALX) or are watching it, the stock’s latest move is worth a closer look. On September 22nd, Alexander’s landed on the Zacks Rank #5 (Strong Sell) list after analysts revised their earnings estimates downward. This kind of shift in analyst sentiment, especially when tied to lower expected profits, often causes investors to rethink their positions, as it may be a warning about future challenges or weaker fundamentals.

Over the past year, Alexander’s share price has gained around 8%, but momentum has picked up lately. Year to date, the stock has climbed 22%, and its return over the past 3 months has also been solid. While those numbers suggest a degree of resilience, the recent addition to the sell list highlights a change in risk perception, putting a spotlight on earnings expectations and future growth prospects.

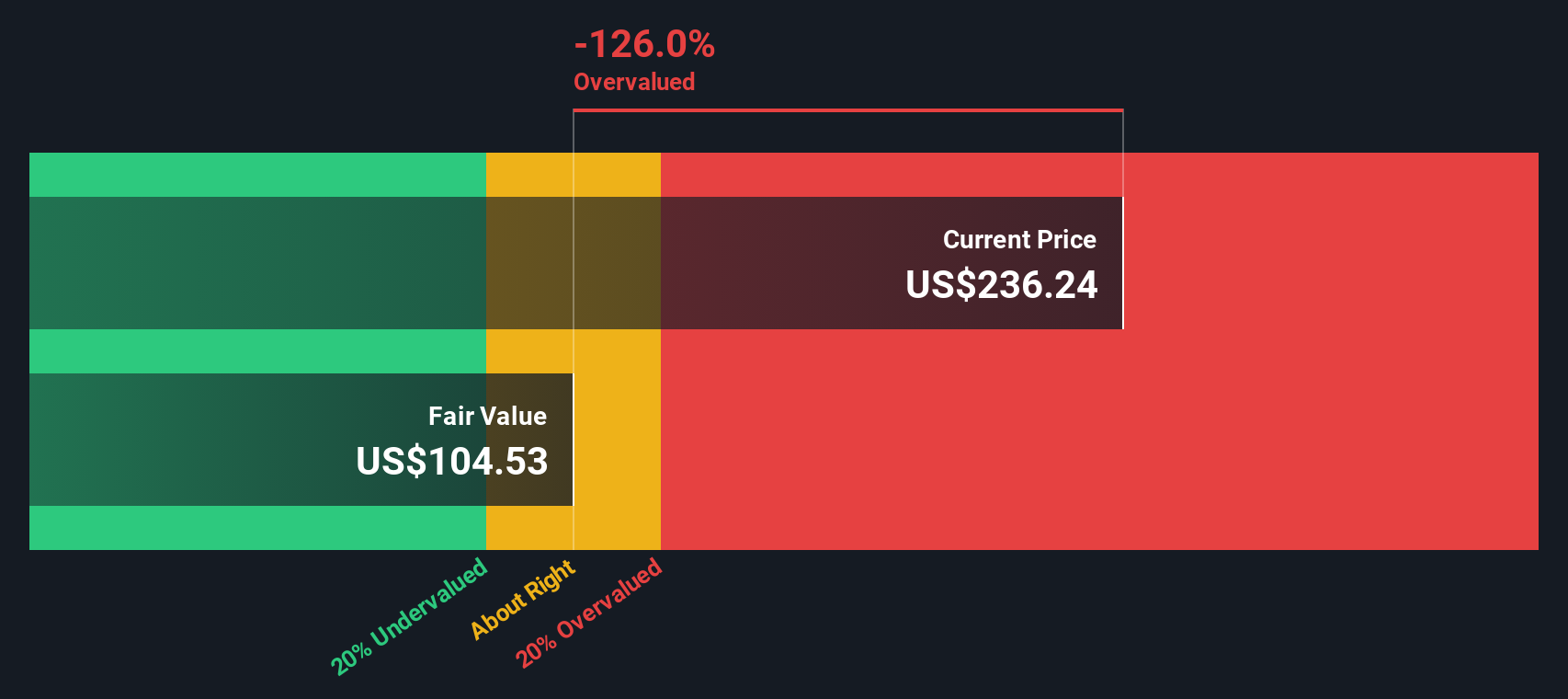

After this shakeup, it is time to consider the big question: is Alexander’s undervalued after its recent price swing, or is the market simply adjusting to new expectations for the company’s future performance?

Advertisement

Price-to-Earnings of 32.8x: Is it justified?

Alexander’s currently trades at a Price-to-Earnings (P/E) ratio of 32.8x, which is significantly higher than both the estimated fair P/E ratio of 20.4x and the peer average of 20.6x. This indicates that shares look expensive compared to what investors are paying for similar companies in the market and industry.

The P/E ratio measures the market price of a company’s shares relative to its earnings. For real estate investment trusts like Alexander’s, the P/E ratio is an important indicator for comparing relative valuation within the sector because it reflects both investor sentiment and expectations for future growth or stability.

The premium in Alexander’s P/E suggests that the market is pricing in higher future earnings or stability than industry peers, even though there have been recent declines in both profits and revenue growth outlook. Investors should consider whether this optimism is warranted in light of the company’s fundamentals.

However, slowing annual revenue growth and sharply declining net income remain significant risks. These factors could quickly shift investor sentiment and challenge the current valuation.

While the market price suggests optimism, our SWS DCF model offers a more grounded perspective and indicates the shares may be overvalued. Could this gap signal that investors are too hopeful, or is something being overlooked?

Stay updated when valuation signals shift by adding Alexander's to your watchlist or portfolio. Alternatively, explore our screener to discover other companies that fit your criteria.

Build Your Own Alexander's Narrative

If you would rather reach your own conclusions or take a different view, you can easily craft a personalized story in just a few minutes with Do it your way.

A great starting point for your Alexander's research is our analysis highlighting 3 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

Smart investors keep an eye out for new opportunities every day. With the Simply Wall St Screener, you can take control and act on fresh, promising investment ideas that match your strategy before others catch on.

Power your portfolio with steady income growth by uncovering companies offering dividend stocks with yields > 3% to investors seeking yields above 3%.

Tap into surging industries and spot potential early winners by checking out the latest AI penny stocks making headlines in artificial intelligence.

Target compelling value plays by searching for undervalued stocks based on cash flows that could be set for a market re-rating based on strong cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks