Advertisement

- United States

- /

- Health Care REITs

- /

- NasdaqGS:SBRA

Sabra Health Care REIT (SBRA): Is the Stock’s Recent Rebound Justified by Its Current Valuation?

Kshitija Bhandaru

Reviewed by Simply Wall St

When it comes to Sabra Health Care REIT (SBRA), recent movement in the share price might be catching your eye, even if there is no single headline event driving all the attention right now. Sometimes, a quiet period can generate just as many questions as a splashy announcement, especially for investors weighing whether to stick with the stock or look elsewhere. For anyone interested in the healthcare real estate space, periods like this can be a good time to step back and re-examine valuation fundamentals.

Sabra Health Care REIT’s performance over the past year provides plenty to think about. The company has quietly delivered an 18% total return to shareholders in the last twelve months, building momentum with a 6% bump over the past three months and a 13% advance since January. Even set against multi-year returns and steady growth in both revenue and net income, it is clear that the shares have staged a solid rebound without much drama or hype.

After a year of steady gains, is Sabra Health Care REIT now attractively priced, or are investors already looking ahead and baking future growth into today’s stock price?

Most Popular Narrative: 7.8% Undervalued

According to the most widely followed narrative, Sabra Health Care REIT appears undervalued by almost 8 percent compared to its calculated fair value. The consensus blends expectations for long-term cash flow growth, strategic acquisitions, and sector tailwinds in senior living and healthcare real estate.

Persistent and accelerating demand for senior housing, assisted living, and memory care driven by the aging U.S. population, specifically the Baby Boomer cohort, continues to outpace new supply due to high barriers to development. This supports higher occupancy, rising rents, and long-term revenue and cash NOI growth across Sabra's property portfolio.

Want to see what’s powering this bullish outlook? The secret is a set of aggressive growth projections and margin forecasts that underpin the eye-catching fair value, without giving away the full playbook. Curious what assumptions analysts are making about Sabra’s future profits that could justify a higher stock price? The details might surprise you.

Result: Fair Value of $20.82 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, new operator transitions or an unexpected surge in industry competition could quickly change the outlook and test the bullish case for Sabra.

Find out about the key risks to this Sabra Health Care REIT narrative.Another View: What Do Valuation Ratios Say?

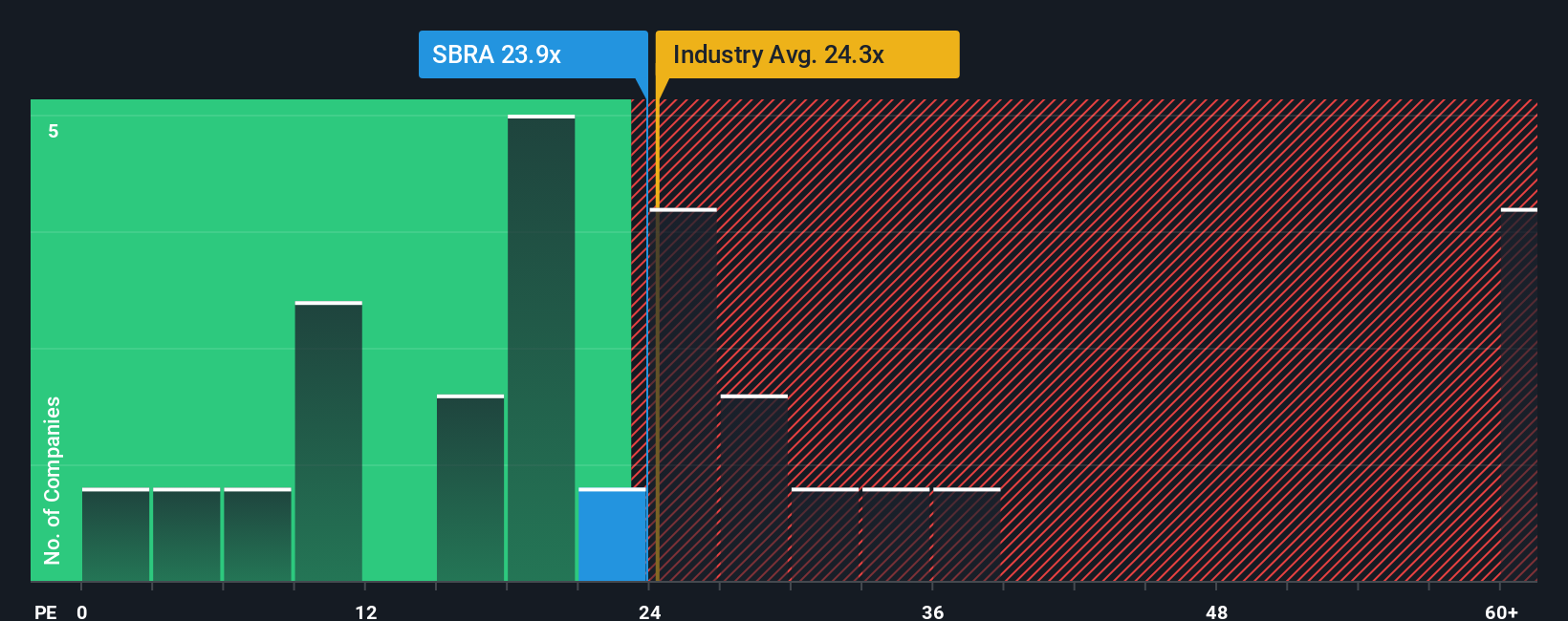

Looking at things from a different angle, valuation ratios suggest Sabra Health Care REIT is a bit pricier than the broader global health care REITs group. Could these numbers be cautioning investors?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Sabra Health Care REIT Narrative

If you see things differently or want to dig into the numbers yourself, crafting your own view takes less than three minutes. Do it your way.

A great starting point for your Sabra Health Care REIT research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Smart Investment Ideas?

Smart investors gain an edge by searching beyond the obvious. Make your next move count with distinctive stock ideas curated for your goals. Don’t let fresh opportunities slip through your fingers. See where your next win could be hiding.

- Tap into the future of medicine with leading-edge innovations sweeping the sector when you check out healthcare’s tech-forward trailblazers in healthcare AI stocks.

- Unlock resilient income streams and shield your portfolio in turbulent times by scanning companies offering dividend stocks with yields > 3%.

- Spot value gems hidden in plain sight as you hunt for shares that are potentially mispriced by the market with our undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NasdaqGS:SBRA

Sabra Health Care REIT

As of June 30, 2025, Sabra’s investment portfolio included 359 real estate properties held for investment (consisting of (i) 219 skilled nursing/transitional care facilities, (ii) 36 senior housing communities (“senior housing - leased”), (iii) 73 senior housing communities operated by third-party property managers pursuant to property management agreements (“senior housing - managed”), (iv) 16 behavioral health facilities and (v) 15 specialty hospitals and other facilities), 13 investments in loans receivable (consisting of three mortgage loans and 10 other loans), four preferred equity investments and two investments in unconsolidated joint ventures.

Solid track record, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor