- United States

- /

- Chemicals

- /

- NasdaqGS:GURE

Carver Bancorp Leads 3 Noteworthy US Penny Stocks

Reviewed by Simply Wall St

Amid a market rebound following a Federal Reserve-induced downturn, U.S. stocks have shown resilience with the Dow Jones, S&P 500, and Nasdaq Composite each gaining ground. Penny stocks may be considered an outdated term by some, yet they remain relevant as investment opportunities for those seeking growth in smaller or newer companies. When these stocks are supported by strong balance sheets and solid fundamentals, they can offer potential upside while mitigating some of the risks typically associated with this segment of the market.

Top 10 Penny Stocks In The United States

| Name | Share Price | Market Cap | Financial Health Rating |

| Inter & Co (NasdaqGS:INTR) | $3.95 | $1.93B | ★★★★☆☆ |

| BAB (OTCPK:BABB) | $0.905 | $6.59M | ★★★★★★ |

| QuantaSing Group (NasdaqGM:QSG) | $3.08 | $108.87M | ★★★★★★ |

| Imperial Petroleum (NasdaqCM:IMPP) | $2.78 | $87.36M | ★★★★★★ |

| ZTEST Electronics (OTCPK:ZTST.F) | $0.21 | $8.8M | ★★★★★★ |

| Permianville Royalty Trust (NYSE:PVL) | $1.445 | $47.52M | ★★★★★★ |

| Golden Growers Cooperative (OTCPK:GGRO.U) | $4.50 | $67.38M | ★★★★★★ |

| Smith Micro Software (NasdaqCM:SMSI) | $0.9632 | $17.69M | ★★★★★☆ |

| CBAK Energy Technology (NasdaqCM:CBAT) | $0.80 | $77.26M | ★★★★★☆ |

| Safe Bulkers (NYSE:SB) | $3.58 | $381.2M | ★★★★☆☆ |

Click here to see the full list of 739 stocks from our US Penny Stocks screener.

We're going to check out a few of the best picks from our screener tool.

Carver Bancorp (NasdaqCM:CARV)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Carver Bancorp, Inc. is the holding company for Carver Federal Savings Bank, offering consumer and commercial banking services to a variety of clients primarily in New York, with a market cap of $9.30 million.

Operations: Carver Bancorp generates revenue of $28.32 million from its consumer and commercial banking services segment.

Market Cap: $9.3M

Carver Bancorp, Inc. faces significant challenges as a penny stock with a market cap of US$9.30 million and ongoing unprofitability, reporting losses of US$2.11 million in the recent quarter. Despite reducing losses by 7.3% annually over five years, it struggles with high bad loans at 2.8%. The company's board recently saw changes driven by activist investor Dream Chasers Capital Group LLC, which criticized past leadership for substantial shareholder value destruction and advocated for new directors to restore growth and profitability while maintaining Carver's community role in New York's underserved areas.

- Click here and access our complete financial health analysis report to understand the dynamics of Carver Bancorp.

- Understand Carver Bancorp's track record by examining our performance history report.

Gulf Resources (NasdaqGS:GURE)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Gulf Resources, Inc. operates through its subsidiaries in the People's Republic of China, focusing on the manufacture and trading of bromine, crude salt, chemical products, and natural gas with a market cap of $6.93 million.

Operations: The company's revenue is primarily derived from its bromine segment at $10.76 million, followed by crude salt at $1.98 million, and natural gas and brine contributing $0.06 million.

Market Cap: $6.93M

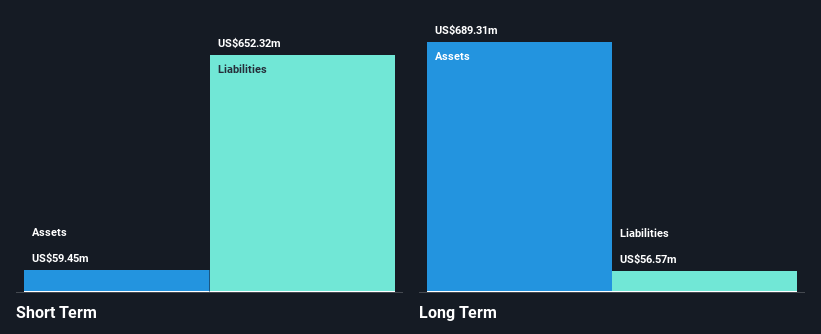

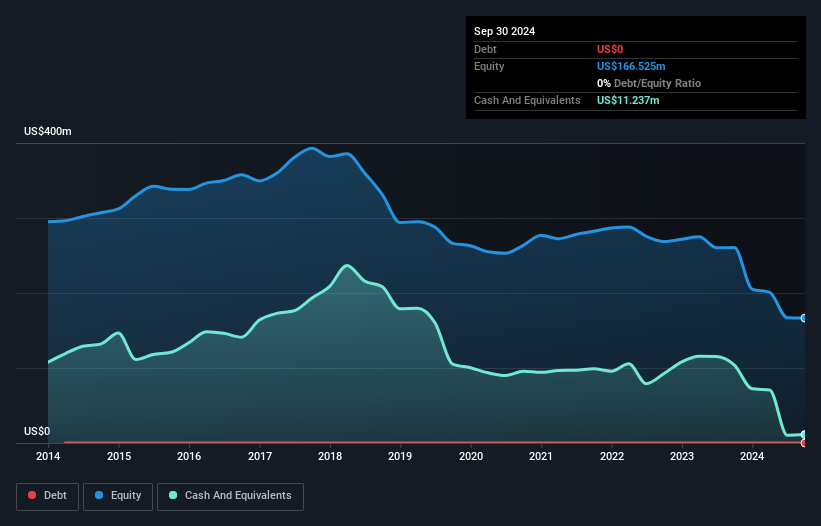

Gulf Resources, Inc. is experiencing financial difficulties, with a significant decline in sales to US$5.93 million for the first nine months of 2024 compared to US$23.17 million a year ago and escalating losses totaling US$40.58 million over the same period. The company has been issued a Nasdaq Deficiency Letter due to its stock price falling below the minimum bid requirement of $1 per share, risking delisting if compliance isn't regained by May 2025. Despite having seasoned management and no debt, Gulf Resources faces volatility and liquidity challenges with less than one year of cash runway remaining.

- Click to explore a detailed breakdown of our findings in Gulf Resources' financial health report.

- Assess Gulf Resources' previous results with our detailed historical performance reports.

Telesis Bio (OTCPK:TBIO)

Simply Wall St Financial Health Rating: ★★★★☆☆

Overview: Telesis Bio, Inc. is a synthetic biology company that manufactures and sells instruments, reagents, and related services to pharmaceutical and academic laboratories globally, with a market cap of $1.19 million.

Operations: The company's revenue is derived entirely from its Scientific & Technical Instruments segment, generating $17.03 million.

Market Cap: $1.19M

Telesis Bio, Inc. faces challenges typical of penny stocks, with declining revenue to US$5.31 million for the first nine months of 2024 from US$15.78 million a year prior and persistent losses totaling US$27.86 million over the same period. Despite a satisfactory net debt to equity ratio of 34.2%, its short-term assets fall short of covering long-term liabilities, indicating financial strain exacerbated by recent shareholder dilution and high volatility in share price. The company recently raised US$3 million through promissory notes to extend its cash runway beyond two months, reflecting ongoing capital needs amidst executive changes and market index removal concerns.

- Unlock comprehensive insights into our analysis of Telesis Bio stock in this financial health report.

- Explore historical data to track Telesis Bio's performance over time in our past results report.

Make It Happen

- Take a closer look at our US Penny Stocks list of 739 companies by clicking here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Jump on the AI train with fast growing tech companies forging a new era of innovation.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:GURE

Gulf Resources

Through its subsidiaries, engages in the manufacture and trading of bromine and crude salt, chemical products, and natural gas in the People’s Republic of China.

Moderate with adequate balance sheet.