- United States

- /

- Life Sciences

- /

- NYSE:WAT

Waters (NYSE:WAT) Achieves Strong Q3 Performance with Innovative Product Adoption and Revenue Growth

Reviewed by Simply Wall St

Waters (NYSE:WAT) has recently showcased impressive financial results, particularly in Q3 2024, where they surpassed expectations in revenue, margins, and earnings per share. This success is driven by strong market strategies and the introduction of innovative products like the Xevo TQ Absolute, which saw significant sales growth. However, challenges such as slower revenue growth compared to the US market and financial risks due to high net debt remain. The company report will delve into key areas including operational excellence, market opportunities like PFAS testing, and the regulatory challenges impacting Waters' competitive positioning.

Dive into the specifics of Waters here with our thorough analysis report.

Key Assets Propelling Waters Forward

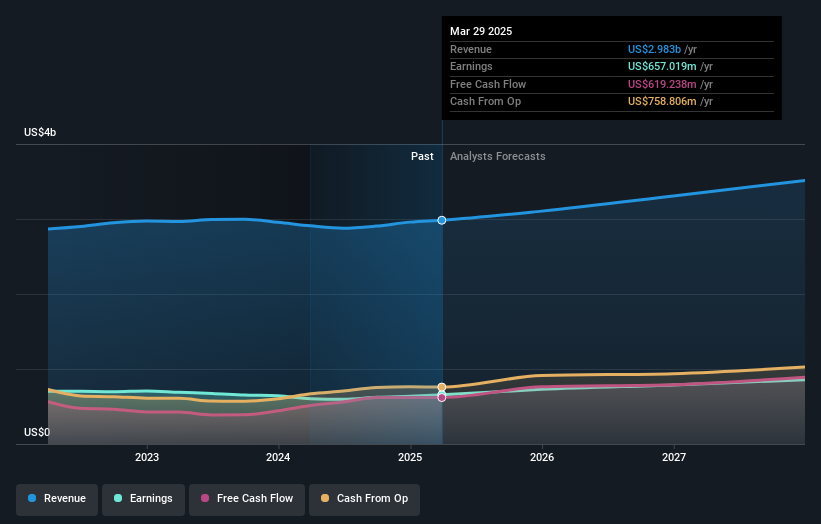

Waters Corporation has demonstrated strong financial performance, particularly in Q3 2024, where they exceeded expectations across revenue, margins, and earnings per share. This achievement underscores the effective market strategies and execution employed by the leadership team, led by CEO Udit Batra. The company's innovative drive is evident in the successful adoption of products like the Xevo TQ Absolute, which saw a 70% increase in unit sales year-over-year, highlighting their ability to meet market demands through technological advancements. Operational excellence has also been a cornerstone, with Waters achieving a gross margin expansion of 20 basis points to 59.3%, as noted by CFO Amol Chaubal. This focus on cost management and productivity reflects the company's strong internal processes and financial discipline.

Internal Limitations Hindering Waters's Growth

Waters faces certain challenges. The company's slow revenue growth forecast of 5.5% per year lags behind the US market's 9.1%, which could impact its competitive positioning. Additionally, the high net debt to equity ratio of 94.9% presents financial risks, especially in volatile markets. The Chinese market continues to be a significant hurdle, with sales declining mid-single digits in Q3, although there has been sequential improvement. Currency fluctuations and inflationary pressures have also posed challenges, impacting financial performance with an estimated 3% headwind from unfavorable foreign exchange rates.

Areas for Expansion and Innovation for Waters

Waters is well-positioned to capitalize on emerging opportunities, particularly with the initiation of the replacement cycle in the liquid chromatography (LC) segment. This cycle is expected to drive sales as customers upgrade their equipment. Furthermore, the company is poised to benefit from high-growth markets such as PFAS testing, projected to be a $300 million to $350 million global market opportunity growing at 20% annually. The ongoing adoption of GLP-1 within the pharmaceutical sector also presents substantial revenue potential, reinforcing Waters' strategic focus on high-growth adjacencies.

Regulatory Challenges Facing Waters

The dynamic nature of market conditions poses threats to Waters' growth trajectory, with economic uncertainties and fluctuating customer spending patterns potentially impacting future performance. Competitive pricing pressures remain a concern, particularly in China, where government policies and funding can significantly influence market dynamics. Waters continues to engage actively with customers to navigate these challenges, as highlighted by CFO Amol Chaubal. The company's valuation, with a Price-To-Earnings Ratio of 36.6x, is considered expensive compared to industry and peer averages, despite trading below estimated fair value, suggesting a need for careful financial navigation.

Conclusion

Waters Corporation's strong financial performance in Q3 2024, driven by effective strategies and innovative product adoption, positions the company well for future growth. However, its slower revenue growth forecast compared to the US market and high net debt to equity ratio highlight potential risks, particularly in volatile markets like China. The company's strategic focus on high-growth areas such as PFAS testing and the liquid chromatography replacement cycle offers significant revenue opportunities, yet economic uncertainties and competitive pressures remain challenges. Furthermore, while Waters trades below its estimated fair value, its Price-To-Earnings Ratio of 36.6x, higher than industry and peer averages, suggests that careful financial management will be crucial to sustaining its market position and capitalizing on growth prospects.

Taking Advantage

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

```If you're looking to trade Waters, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Waters might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WAT

Waters

Provides analytical workflow solutions in Asia, the Americas, and Europe.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives