- United States

- /

- Pharma

- /

- NYSE:ELAN

Elanco Animal Health Incorporated (NYSE:ELAN) Surges 25% Yet Its Low P/S Is No Reason For Excitement

Those holding Elanco Animal Health Incorporated (NYSE:ELAN) shares would be relieved that the share price has rebounded 25% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Looking further back, the 25% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

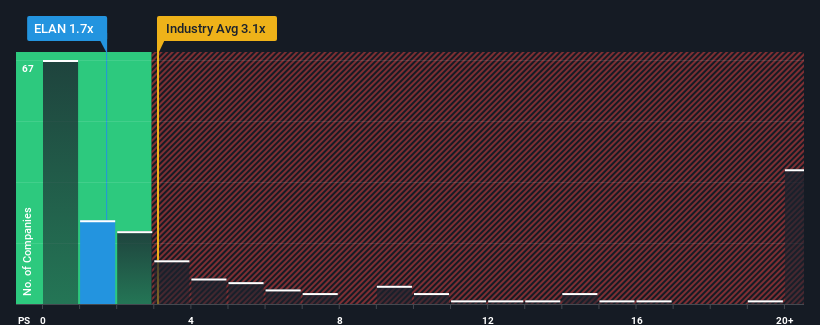

In spite of the firm bounce in price, Elanco Animal Health may still be sending bullish signals at the moment with its price-to-sales (or "P/S") ratio of 1.7x, since almost half of all companies in the Pharmaceuticals industry in the United States have P/S ratios greater than 3.1x and even P/S higher than 12x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

See our latest analysis for Elanco Animal Health

How Has Elanco Animal Health Performed Recently?

With revenue growth that's inferior to most other companies of late, Elanco Animal Health has been relatively sluggish. The P/S ratio is probably low because investors think this lacklustre revenue performance isn't going to get any better. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

Keen to find out how analysts think Elanco Animal Health's future stacks up against the industry? In that case, our free report is a great place to start.How Is Elanco Animal Health's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as low as Elanco Animal Health's is when the company's growth is on track to lag the industry.

If we review the last year of revenue growth, the company posted a worthy increase of 3.9%. However, this wasn't enough as the latest three year period has seen an unpleasant 1.3% overall drop in revenue. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 3.2% per annum during the coming three years according to the ten analysts following the company. With the industry predicted to deliver 16% growth per annum, the company is positioned for a weaker revenue result.

With this information, we can see why Elanco Animal Health is trading at a P/S lower than the industry. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Final Word

Despite Elanco Animal Health's share price climbing recently, its P/S still lags most other companies. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

As expected, our analysis of Elanco Animal Health's analyst forecasts confirms that the company's underwhelming revenue outlook is a major contributor to its low P/S. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

Many other vital risk factors can be found on the company's balance sheet. Take a look at our free balance sheet analysis for Elanco Animal Health with six simple checks on some of these key factors.

If these risks are making you reconsider your opinion on Elanco Animal Health, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Elanco Animal Health might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:ELAN

Elanco Animal Health

An animal health company, innovates, develops, manufactures, and markets products for pets and farm animals.

Fair value with questionable track record.

Similar Companies

Market Insights

Community Narratives