Advertisement

- United States

- /

- Pharma

- /

- NasdaqGS:TLRY

Decriminalization Buzz is Moving Tilray (NASDAQ:TLRY), but The Company may have some Significant Issues

Hopes on cannabis decriminalization have rallied the market for companies like Tilray Brands ( NASDAQ:TLRY ), which gained 14% on the news. This comes after news that the U.S. House is cooking up the "Marijuana Opportunity Reinvestment" bill, which also needs to pass in the Senate in order to be successful. A similar bill in 2020 failed in the Senate, however this time the Senate is controlled by the Democrats that support the bill.

While the company may capitalize on penetrating the U.S. market, there are significant risks to the company, which we will analyze today.

There is a reason why investors are excited about the stock, as the company might be valuable, especially if it gains more market exposure.

What is the Company Worth?

In order for Tilray to become a worthwhile business for investors, it needs to grow and come up with positive cash flows.

We can build a projected cash flow model based on analyst forecasts and the assumption that growth decelerates as the company's market matures. For Tilray, analysts project negative cash flows until 2023, at which point the company is expected to start turning positive and reach about US$483 in 2031. Summing up and discounting to present value, we get an intrinsic value of US$8.6b for the company.

Take a look how we do our discounted cash flow valuations HERE.

Keep in mind that unprofitable companies like Tilray have difficulties executing, and analyst forecasts may change as things progress.

Analyzing Key Risks

In order to see if Tilray is a good investment, we need to assess some of the risks of the company. In this early stage of the lifecycle, Tilray is likely a high risk stock, and we need to see if they can develop their business into a good investment.

The first signs of risk were spotted by our team in January , where our analysts discussed the unusual CEO compensation of the unprofitable company, as well as the issue with the 47% share dilution from last year. Even if a company manages to turn a profit, poor management discipline and lack of responsibility to shareholders can make this company a bad investment for shareholders.

Diving into the financials, we can see some possible financial problems for the company.

View our latest analysis for Tilray Brands

Tilray's Financial Standing

In order for the company to become profitable, it needs to exist, and the byrocratic decriminalization (and possibly licensing) process in the U.S. may take longer than anticipated.

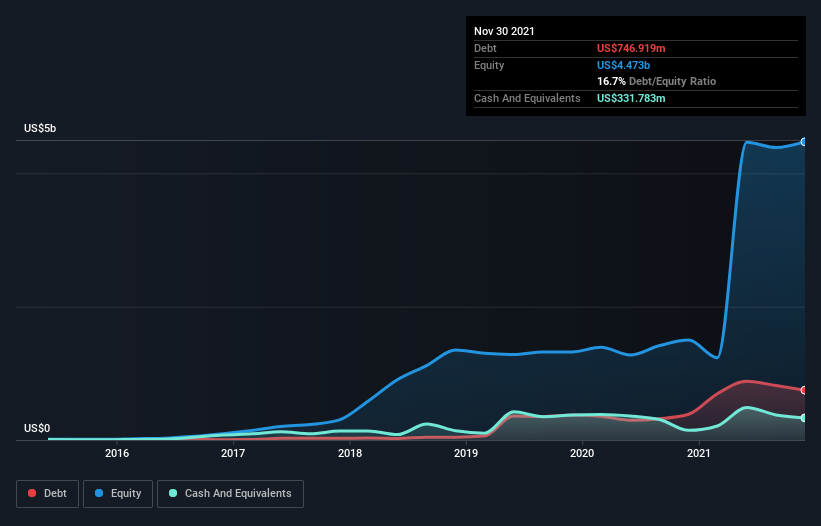

Tilray Brands has engaged in debt financing since 2019. This is generally bad for pre-profit companies, as it imposes future fixed costs and increases financial risk. While analysts can argue that the company used this debt in productive ways, it currently represents some 22% of the market value of equity and that is a significant level for a pre-profit company.

So we have one factor that may be quite concerning.

Now, we will evaluate if the company has enough cash to develop until it can touch positive territory For this, we analyze Tilroy's cash runway.

Cash Runway

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn.

The company held about US$332m in cash by November 2021. Looking at the last year, the company burned through US$134m.

Therefore, from November 2021 it had 2.5 years of cash runway. More importantly though, some analysts have revised their timeline on when they think Tilray Brands will reach cashflow breakeven; the company may even be in need of additional financing.

Depicted below, you can see how its cash holdings have changed over time.

The best case scenario would be if the company picks up revenue growth and the U.S. allows it to enter the market. Hopefully the company is able to pull it off just in time.

Future Financing Options

What can the company do if it needs more financing?

The company can raise more debt, with the caveat that this will be harder in the future if interest rates keep increasing. Alternatively, they can raise funds from issuing more shares, but that comes at the expense of investors who are arguably already unimpressed with the 65% drop in share price from a year ago and the current amount of share dilution. Management has arguably some explaining to do, and should be held accountable to the people that fund the company.

Key Takeaways

While it is great to hear buzz that the U.S. may decriminalize marijuana, we hope that this process happens soon enough in order for the company to smoothly enter the market.

While not drastic, Tilray has some financing risks and management doesn't seem to be able to execute as well as investors had hoped.

If investors believe that the company will overcome these challenges, then they may potentially see significant upside, as the company's cash flows seem to have a value of US$20 per share. In any case, Tilray is a high risk-return stock.

On another note, Tilray Brands has 2 warning signs (and 1 of which is concerning) that we think you should know about.

Of course, you may also find fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

Valuation is complex, but we're here to simplify it.

Discover if Tilray Brands might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NasdaqGS:TLRY

Tilray Brands

A lifestyle consumer products company, engages in the research, cultivation, processing, and distribution of medical cannabis products in Canada, the United States, Europe, the Middle East, Africa, and internationally.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|69.8% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|15.0% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|36.1% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.1% undervalued

AN

Based on Analyst Price Targets