Advertisement

- United States

- /

- Pharma

- /

- NasdaqGS:TLRY

Tilray's (NASDAQ:TLRY) Earnings Need a Scratch Below the Surface

Tilray, Inc.'s (NASDAQ: TLRY)story of 2021 has been the one of boom and bust (once again), as the stock repeated the performance from 2018 – albeit on a much smaller scale.

Although the stock gained on earnings results, digging deeper shows things are not what they seem.

Check out our latest analysis for Tilray

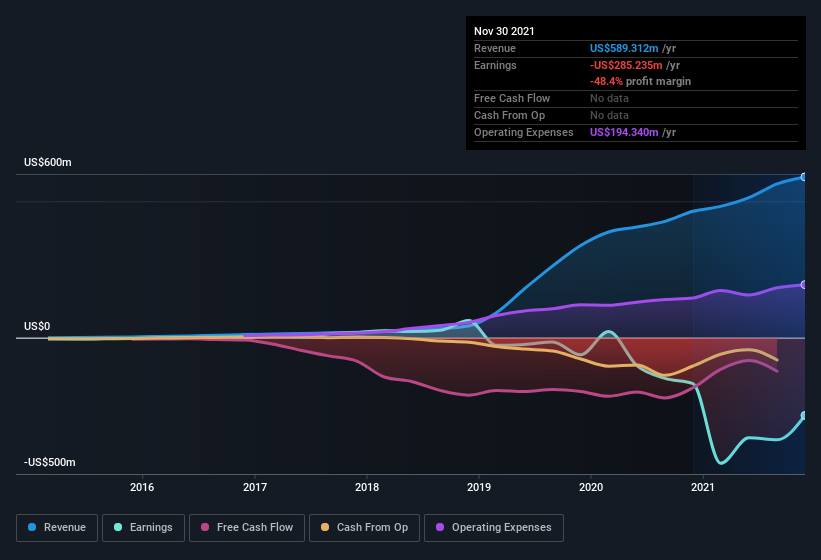

Second-quarter 2022 results:

- EPS: US$0.013 (up from US$0.32 loss in 2Q 2021).

- Revenue: US$155.2m (up 26% from 2Q 2021).

- Net income: US$5.80m (up to US$98.6m from 2Q 2021).

- Profit margin: 3.7% (up from a net loss in 2Q 2021).

Revenue missed analyst estimates by 9.3%, while earnings per share (EPS) exceeded analyst estimates. Over the next year, revenue is forecast to grow 19%, compared to a 16% growth forecast for the industry in the US.

Yet, looking deeper, the critics have highlighted the following:

- Actual EBIDTA was negative without adjustments that removed about US$29M

- Operating loss rose significantly Y/Y

- Sales decreased over 10% Q/Q for cannabis and beverage sales

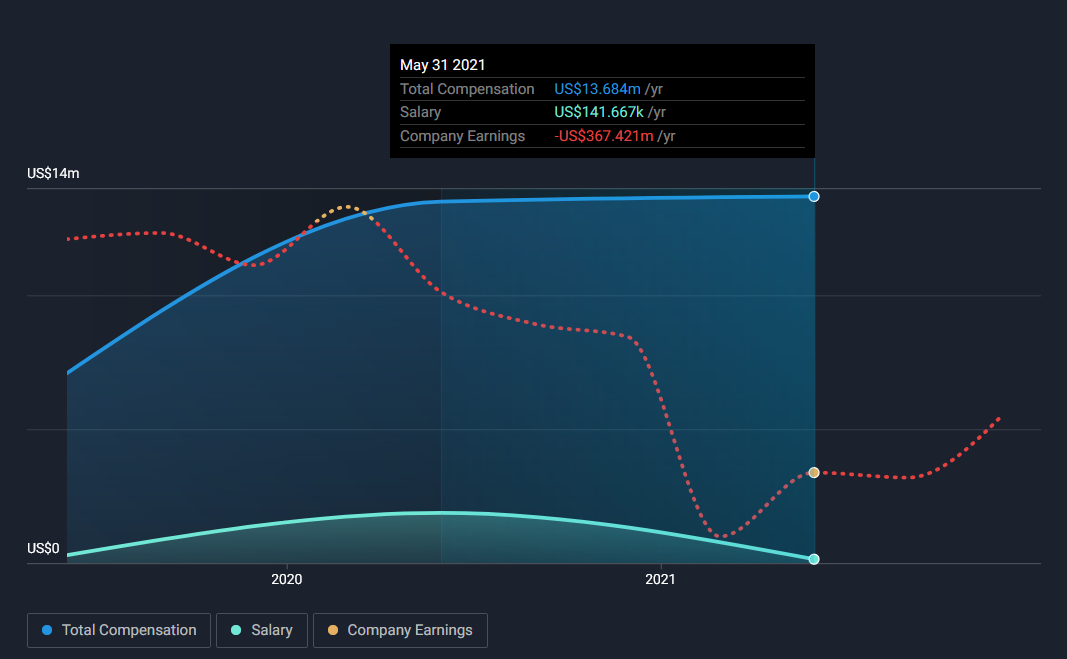

Furthermore, according to our data, CEO's compensation vastly exceeds the average for companies of similar size.

For 2021, the CEO's cash bonuses exceeded US$13m, with total compensation of nearly US$30m. This is around 20% of the quarterly revenues!

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. Tilray expanded the number of shares on issue by 47% over the last year. That means its earnings are split among a greater number of shares.

To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. You can see a chart of Tilray's EPS by clicking here.

A Look At The Impact Of Tilray's Dilution on Its Earnings Per Share (EPS).

Unfortunately, we don't have any visibility into its profits three years back, because we lack the data. And in focusing only on the last twelve months, we don't have a meaningful growth rate because it made a loss a year ago, too. One can observe that the dilution has a fairly profound effect on shareholder returns.

If Tilray's EPS can grow over time, that drastically improves the chances of the share price moving in the same direction. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

That might leave you wondering what analysts forecast in terms of future profitability. Lucky, you can click here to see an interactive graph depicting future profitability based on their estimates.

The Impact Of Unusual Items On Profit

On top of the dilution, we should also consider the US$77m impact of unusual items in the last year, which suppressed profit. While deductions due to unusual items are disappointing in the first instance, there is a silver lining.

When we analyzed most listed companies worldwide, we found that significant unusual items are often not repeated. And, after all, that's exactly what the accounting terminology implies. Tilray took a rather significant hit from unusual items through 2021. All else being equal, this would likely have the effect of making the statutory profit look worse than its underlying earnings power.

Our Take On Tilray's Profit Performance

To sum it all up, Tilray took a hit from unusual items, which pushed its profit down; without that, it would have made more money. Even so, the company has been careful in its approach to the latest earnings presentation, avoiding the painful points.

Unfortunately, the dilution means that shareholders now own a smaller proportion of the company (assuming they maintained the same number of shares). That will weigh on earnings per share, even if it is not reflected in net income.

Based on these factors, it's hard to tell if Tilray's profits are a reasonable reflection of its underlying profitability. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. Every company has risks, and we've spotted 3 warning signs for Tilray you should know about.

In this article, we've looked at a number of factors that can impair the utility of profit numbers as a guide to a business. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity to indicate favorable business economics, while others like to "follow the money" and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity or this list of stocks that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if Tilray Brands might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Stjepan Kalinic

Stjepan is a writer and an analyst covering equity markets. As a former multi-asset analyst, he prefers to look beyond the surface and uncover ideas that might not be on retail investors' radar. You can find his research all over the internet, including Simply Wall St News, Yahoo Finance, Benzinga, Vincent, and Barron's.

About NasdaqGS:TLRY

Tilray Brands

A lifestyle consumer products company, engages in the research, cultivation, processing, and distribution of medical cannabis products in Canada, the United States, Europe, the Middle East, Africa, and internationally.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2552.0% undervalued

130 followersusers have followed this narrative

0 commentsusers have commented on this narrative

25 likesusers have liked this narrative

BL

BlackGoat on IREN ·

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value:US$71.4848.5% undervalued

227 followersusers have followed this narrative

10 commentsusers have commented on this narrative

33 likesusers have liked this narrative

HE

HedgeY on Arm Holdings ·

The Architecture Layer of AI Computing - But Priced Like the Future Already Arrived?

Fair Value:US$43044.3% undervalued

27 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

HI

Hidden_Rock_Capital on Fiserv ·

Temporary "perfect storm" leads to opportunity to buy financial services leader for less than 5x long-term earnings

Fair Value:US$119.9955.0% undervalued

36 followersusers have followed this narrative

1 commentusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

CH

ChuckN on XPLR Infrastructure ·

Investor Thesis: Why XPLR Infrastructure Could Be Deeply Undervalued in an AI Power Cycle

Fair Value:US$209.0294.3% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

andre_santos on Netflix ·

Netflix - A Fundamental Valuation

Fair Value:US$98.7127.4% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on Reddit ·

Reddit's Discount Is Big Enough to Make Me Suspicious. Here's What I Found When I Went Looking for the Reason.

Fair Value:US$423.6866.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28028.3% undervalued

232 followersusers have followed this narrative

9 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9110.7% overvalued

112 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23054.8% overvalued

124 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

GR

greg_xasak on Fiserv ·

As someone who has dealt directly with them as a CTO for a credit union, I have 8 years of horror stories about doing business with them. If there was any other competitor than could deliver 80% of Fiserv services, there would be a mad rush to migrate to them. They should thank their lucky stars they are a near monopoly. this industry is so ripe for a well funded competitor. Their integration of technology is awful, their ability to fix their own implementation screwups is sadly tragic. Sometimes they just silently kill support tickets without resolution and you never find out until you do a follow up inquiry. Why, because sometimes no one you are dealing with knows how to fix it and knows no one to ask for help. They can not meet their own implementation deadlines and sometimes there is no one on a technical team dealing with you that has any banking or credit union experience. The is an industry insider phrase when you meet other Fiserv customers called being "Fiserved". It means telling others of your worst stories of dealing with them. Ask around, all CTO's have some doozies.

2

|0